Carsales.Com Ltd

.png)

CAR Details

Stable Market Outlook: Carsales.Com Ltd (ASX: CAR) has reported growth of 10% in operating revenue to $344.0 million for FY 16 as compared to FY15. Earnings before interest, tax, depreciation and amortization (EBITDA) grew 10% to $170.3 million during the period as compared to the prior comparative period (pcp). Moreover, CAR’s dealer revenue increased by 10% year on year. The private seller revenue grew by 19% and the display revenue grew 9% year on year. The Finance and related services showed strong growth with gross profit up 29% year on year. Brazilian and South Korean international investments reported a strong local currency revenue growth. Additionally, CAR had acquired 83% of Chileautos in Chile during the second half of FY 16 and had acquired 65% of SoloAutos during the first half of FY 16. In addition, the Domestic core business performance in the first month of FY17 was strong. The company is continuing to build scale and breadth with a number of promising opportunities. CAR is expecting FY17 revenue and EBITDA growth to remain strong due to stable market conditions. Internationally, CAR is expecting that the trial of the lead model into Brazil will be a good growth contributor to local currency revenue and earnings in FY 17, assuming no further deterioration in market conditions.

.png)

Revenue & EBITDA Performance (Source: Company Reports)

Korea is expected to see continued solid local currency revenue and earnings growth. In addition, CAR is expecting that the ongoing integration of core carsales’ IP and technology into Chilean and Mexican businesses will provide solid uplift in revenue and earnings in FY 17. Meanwhile, CAR stock has risen 21.57% in the six months (as of August 10, 2016). CAR has declared a fully franked final dividend of 19.5 cents per share, an increase of 10% on prior corresponding period (pcp) to be paid on October 17, 2016.

CAR Daily Chart (Source: Thomson Reuters)

Suncorp Group Ltd

.png)

SUN Details

Well capitalized but subdued profit reporting: Suncorp Group Ltd (ASX: SUN) has reported NPAT of $1,038 million in FY 16 as compared to $1,133 million in the prior corresponding period. This is due to the lower returns from investment markets and a reduction in reserve releases. The General Insurance underlying ITR is of 10.6% due to the increased cost of settling claims and lower investment returns, and the total GWP increased by 1.8% to over $9 billion. Suncorp Bank net profit after tax grew 11.0% due to continued home lending growth, improved net interest margins and ongoing improvement in credit quality. Suncorp Life net profit after tax grew 13.6% and the underlying profit increased by 9.7% to $124 million. The underlying profit included the positive lapse and claims experience of $21 million. In addition, after accounting the dividend payment, the group is well capitalized with $346 million in CET1 capital held above its operating targets. The General Insurance CET1 ratio is 1.21 times Prescribed Capital Amount and the Bank CET1 ratio is 9.21%. Moreover, SUN has completed the organizational restructuring on 4

th July 2016 which will deliver an ongoing benefit of at least $80 million per annum, at an upfront charge of $55 million. On the other hand, SUN has set the medium term target, and according to which, the cost base is expected to be flat in FY 17 and FY 18. This is taken into account by the ongoing benefits from the optimization program, the operating model restructure and the incremental investment in critical elements of the customer strategy.

.png)

Financial Performance for FY 16 (Source: Company Reports)

SUN is expected to improve the underlying NPAT across the business through driving margins in general insurance back to 12% and reducing the Bank’s cost to income ratio. SUN expects to get a sustainable return on equity of at least 10% which means an underlying ITR of at least 12% and maintaining the dividend payout ratio of 60% to 80% of the cash earnings. Meanwhile, SUN stock has risen 28.32% in the last six months (as of August 10, 2016), while the stock has a decent dividend yield and is trading ex-dividend on August 12, 2016.

.PNG)

SUN Daily Chart (Source: Thomson Reuters)

Cochlear Limited

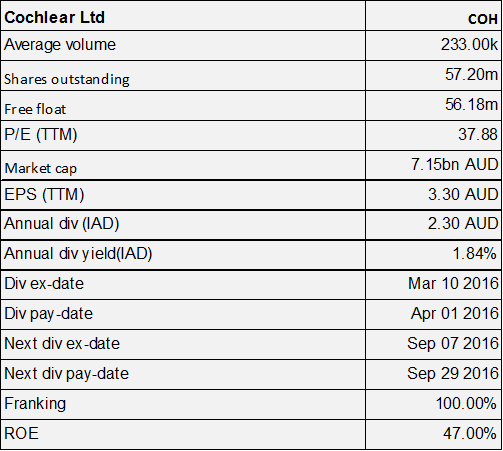

COH Details

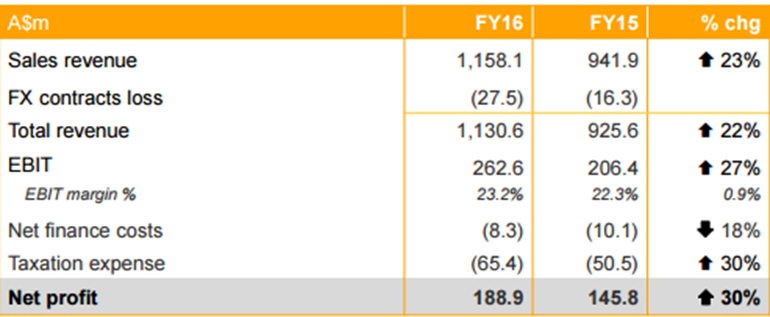

Delivered net profit at top end of guidance range: Cochlear Limited (ASX: COH) has delivered a sales revenue growth of 23% to $1,158.1 million in fiscal year of 2016 on a year on year (yoy) basis. This is the first time the company has reported more than $1billion of the revenue. COH has also reported 30% growth in Net Profit to $188.9 million, which is at the top end of the guidance range and reported an EPS growth of 29% to $3.31 per share in FY 16 as compared to FY 15. COH got benefit from the devaluation of the Australian dollar and invested in market growth initiatives, including direct-to-consumer marketing and expansion of the sales force, as well as increased the investment in R&D. Moreover, COH’s implant business has reported revenue growth of 21% (10% in constant currency) and the unit growth of 12%. COH has also seen growth of the implant units by around 10% in the United States, the United Kingdom, and Germany, while the Emerging markets performed well including China, India and the Middle East. COH’s services business sales’ revenue grew 30% (20% in constant currency) and represents approximately 25% of sales revenue. In addition, COH has expanded the recipient recruitment program and clinical support tools with the roll out of Cochlear Family, MyCochlear.com and CochlearLink and expanded the wireless product offerings.

Financial Performance for FY 16 (Source: Company Reports)

Additionally, in FY 16 COH has come up with first off-the-ear sound processor Cochlear

TM Kanso

TM, and had expanded the bone conduction portfolio with Baha® 5 Power and SuperPower sound processors, introduced the Nucleus Profile Slim Modiolar electrode which is the world’s slimmest electrode and launched the next generation True Wireless Mini Microphone 2+. COH has established an innovation fund to focus on innovative technologies, which will potentially assist COH’s future business activities and already $14 million was invested in FY16. On the other hand, for FY17, the net profit is expected to be in the range of $210-225 million, which is an increase of around 10-20% on FY16. COH is expecting to have continued strong uptake of the Nucleus 6 and Kanso sound processors over the next few years with the current penetration rate for the Nucleus 6 at around 22% of potential recipients. The Chinese Central Government tender units are expected to be at similar levels to FY16 with delivery of units biased to the first half of FY 17. In Europe, COH does not expect any immediate impact on the business from the UK’s decision to withdraw from the European Union. However, the Company remains alert to the potential for uncertainty to curtail economic growth and put pressure on health budgets. COH expects FY17 R&D expenditure to be broadly in line with that for FY16, which represents a lower percentage of sales revenue. Moreover, COH is forecasting a weighted average AUD/USD FX rate of 75 cents for FY17 versus 73 cents in FY16 and expects the balance sheet position and free cash flow generation to remain strong. COH will continue to target a dividend payout ratio of around 70% of net profit as in FY 16. Meanwhile, COH stock has risen 47.52% in the six months (as of August 10, 2016) and is close to its 52-week high price.

.PNG)

COH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...