Pacific Brands Limited (ASX: PBG) improved its fiscal year 2015 guidance, and now estimates its EBIT before significant items to be over $63 million to $65 million. Earlier, the group issued a second half of the fiscal year 2015’s EBIT before significant items to reach over $25.9 million, and entire FY15 to be in the range of $57.4 million and $63.0 million. Pacific guidance update is mainly due to better performance in May and June tradings driven by theBonds and Sheridan retail segments and enhanced margins. The group now expects revenues to grow by 5.3% yoy, while the net debt is forecasted to be $1 million.

First half of fiscal year 2015 highlights

-

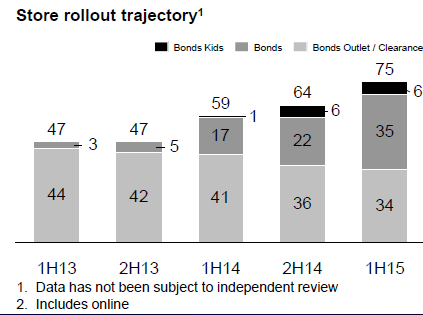

Underwear Segment Performance: The Underwear revenues rose by 4.1% yoy to $252.6 million during the first half of 2015, mainly driven by the Bonds sales, which surged 15% yoy. However, the Non-Bonds brands fell 14.6 yoy due to lower sales from DDS channel and private labels. Therefore, the overall Underwear wholesale sales also got impacted, reducing by 5.8% on a yoy basis. Even the EBIT fell 25.8% yoy to $26.7 million as lower wholesale sales impacted margins. Meanwhile, the retail sales in Underwear surged 50.7% yoy as the group opened 13 stores during the period for Bonds.

Underwear Segment’s store rollout (Source: Company Reports)

-

Sheridan and Tontine & Dunlop Flooring segment results: The Sheridan revenues soared 13.7% yoy to $95.3 million in the first half of 2015, driven by retail channels growth of 22% yoy. The comparable sales in Boutique and Sheridan Factory Outlet witnessed an increase of 25% and 14% respectively in 1H15, as compared to pcp. Accordingly, the EBIT (before significant items) drove to $8.7 million, an increase of 5.4% yoy. As per the Tontine and Dunlop Flooringsegment performance, the revenues slightly increased by 1.2% yoy to $43.8 million. But, the Tontine revenues slightly fell by 0.9% yoy impacted by DDS. However, Dunlop Flooring sales offset this decline by increasing 3.1% yoy. Meanwhile, the segment’s EBIT before significant items improved by 13.8% yoy.

Sheridan and Tontine & Dunlop Flooring revenues by segment(Source: Company Reports)

-

Pacific Brands managed to report an overall yoy revenue growth by 6.0%, but the Gross margins were under pressure, which decreased by 3.6pts to 48.5% as compared to 1H14. This margins decrease was mainly due to foreign exchanges impact on import costs which resulted in increase in prices. But, cost of doing business (CODB) rose by 5.1% yoy or $7.7 million to $158.6 million, driven by retail expansion and optimized store expenses. On the other hand, Pacific reported a net loss after tax of $108.7 million impacted by impairment charges of $138.5 million related to goodwill, brand names and plant and equipment. Meanwhile, Pacific is making efforts to improve its balance sheet and accordingly decreased its net debt to $24.2 million in December 2014 from $249.1 million in June 2014, on the back of better working capital, cash conversion of 135% and divestments. The company did not even declare dividends during the first half.

Outlook

-

Going forward, Pacific Brands intends to focus on its major brands to further grow its retail and online business and achieve operational efficiencies. Accordingly, the group has been making Workwear and Brand Collective divestments, and strengthening balance sheet by offloading non-core brands. The group raised over $226 million by selling its Hard Yakka and King Gee workwear business to Wesfarmers, while Anchorage Capital Partners acquired the group’s Volley, Grosby, Everlast, Slazenger and Dunlop clothing and footwear brands.

-

On the other hand, Pacific increased dependence on the performance of Bonds and Sheridan segment might be tough in the current challenging markets. Moreover, the company raised cash by selling its non-core brands, subsequently losing business to competition. Management also earlier said that the falling foreign exchange rates would hurt its margins, inventory balances and cash conversion from the fourth quarter of 2015 to FY16 and FY17.

-

Pacific Brands stock has been under pressure from several years posting a decline of approx. 53% over the last five years and around 26.3% in the last fifty two weeks. Although the stock jumped over 31.3% from July 1st till date (as of August 14th, due to guidance update) to around $0.49 levels, the shares were not able to hold these levels and have been declining since then. Delivering a negative return on average equity of around 37.9%, we believe there are no solid triggers for the stock to attract investors. Based on the foregoing, we reiterate our “SELL” recommendation to the stock at the current price of $0.425, and update the status after reviewing its full year fiscal 2015 results, which would be releasing on 25th August.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...