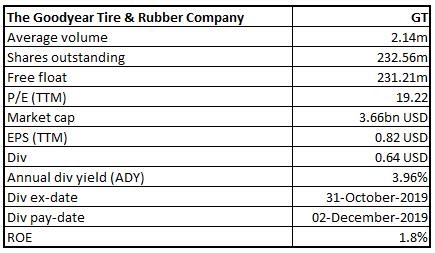

The Goodyear Tire & Rubber Company

GT Details

Strong Volume Growth in China in Q3 2019: The Goodyear Tire & Rubber Company (NYSE: GT) is the world’s leading developer, manufacturer, marketer and distributor of tires. The company is one of the world’s largest operators of commercial truck service and tire retreading centers.

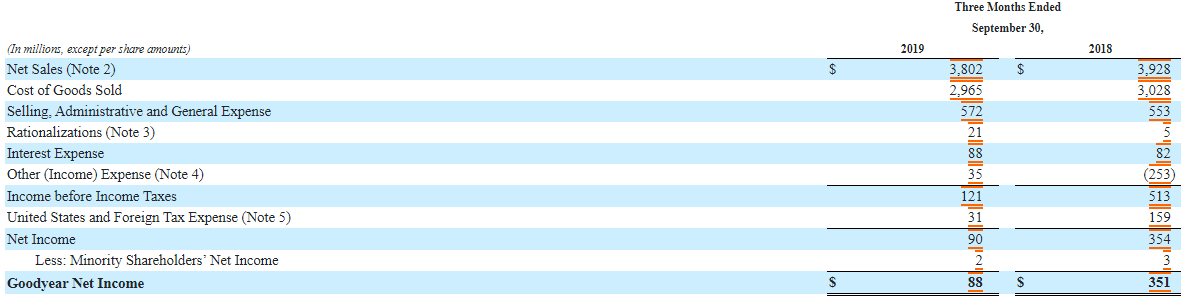

Q3FY19 Financial Highlights for the period ended 30 September 2019:GT announced its FY19 third-quarter financial report, wherein the company posted net sales of $3,802 million, down 3% from Q3FY18. The company reported a net income of $90 million as compared to $354 million in Q2FY18. During FY19, the company reported total unit sales at 40.3 million, down 1% on y-o-y basis. Operating income during Q3FY19 came in at $175 million, down 9.8% from $194 million in Q3FY18. Operating income was down on account of favorable indirect tax settlement of $21 million in Brazil during 2018, higher selling, administrative and general expense (SAG) of $20 million, primarily related to higher incentive compensation; and higher product liability costs, lower income.

Q3FY19 Financial Highlights (Source: Company Reports)

The Americas segmentreported net sales at $2,049 million, down 2.8% on pcp. Total unit sales stood at 17.9 million, up 0.9% y-o-y basis. A decrease in net sales was due to lower sales in other tire-related businesses.

The Europe, Middle East & Africasegment reported total unit sales of 14.5 million as compared to 15.2 million in the previous corresponding period. Net sales from the segment decreased 6.6% on y-o-y basis at $1,205 million. The company reported a lower operating margin of 5.5% as compared to 8.6% in Q3FY18. The segment witnessed a lower volume on account of decline in overall consumer shipments due to tepid market scenario and distribution challenges. On the other hand, the business reported strong commercial replacement during the quarter.

Asia Pacific segment reported a 5.4% and 3.2% year-on-year increase in total unit sales and net sales at 7.9 million and $548 million, respectively. The quarter was marked by strong growth in both replacement and original equipment, especially in China.

Outlook:As per the guidance for FY19, GT is expecting a capital expenditure of ~$800 million to ~$825 million. The business is expecting a working capital of less than $100 million. Depreciation and amortization costs are estimated to be around $775 million. GT expects interest expense at around ~$350 million for the current financial year and predicts income tax expense to be ~25% of global pre-tax operating income.

Stock Recommendation:The stock of GT closed at $15.76 on 20 November 2019 and has a market capitalization of ~$3.66 billion. The stock has generated returns of ~35.395% and ~5.5593% in the last three months and six-months, respectively. The company has an enterprise value to sales multiple of 0.7x on trailing twelve months basis as compared to the industry median of 1.2x. EV/EBITDA multiple of the company stands at 5.9x on TTM basis as compared to the industry median of 7.8x. GT is focused on developing products and services that anticipate and respond to the growing needs of the consumers. It aims at improving the manufacturing efficiency and creating an advantaged supply chain focused on reducing total delivered costs. Considering the performance in the third quarter, decent FY19 outlook, recent price movements, and current valuations, we recommend a ‘Buy’ rating on the stock at the current market price of $15.76, down 2.54% on 20 November 2019.

GT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...