Leigh Creek Energy Limited

LCK’s Maiden PRMS Certification Based On JORC Report: Leigh Creek Energy Limited (ASX: LCK) is engaged in the development of its Leigh Creek Energy project (LCEP) in South Australia. The LCEP will produce synthetic natural gas and/or ammonium nitrate products (fertiliser and industrial explosives) from the remnant coal resources at Leigh Creek, utilising In Situ Gasification technologies, and will provide long term stability and economic development opportunities to the communities of the Upper Spencer Gulf, northern Flinders Ranges and South Australia.

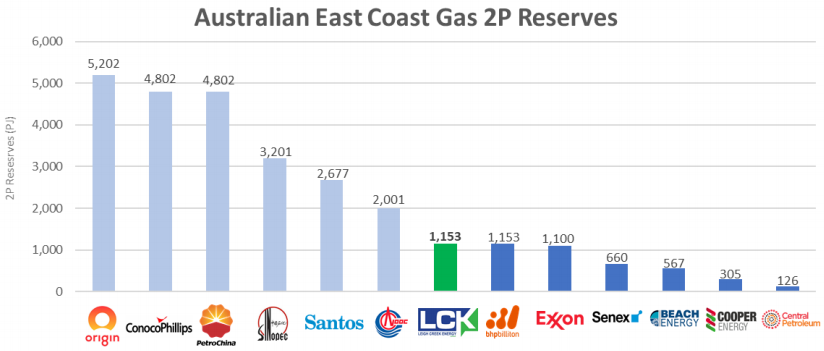

The company recently provided in-depth review of the Leigh Creek Energy project regarding its Society of Petroleum Engineers - Petroleum Resources Management System (PRMS) certification of 1,153 PJ 2P Reserve. The current PRMS 2P gas reserve only accounts for 31% of the available JORC compliant coal resource. There is a potential for additional gas reserve upgrades are anticipated. As per LCK’s LCEP JORC report, total 301.2 mt of coal was the subject of LCK’s JORC Report, of which 62% related to Indicated Resources, and 38% for Inferred Resources, in the Telford Basin.

March 2019 Quarterly Report: LCK reported total cash balance at $6.6 Mn on March 31, 2019. During the March 2019 quarter, the CBA Research and Development working capital debt facility was extended to $4.0 Mn. The total debt drawn under this facility was $3.6 Mn, leaving $0.4 Mn available to be drawn upon as needed. In the March quarter, the Company undertook capital raising activities by offering 25,000,000 Convertible Notes with a face value of AUD$3.0 million with a fixed conversion price of $0:12/note, to existing Top 20 LCK shareholder, Crown Ascent Development Limited.

Gas 2P Reserves with Various Players (Source: Company Reports)

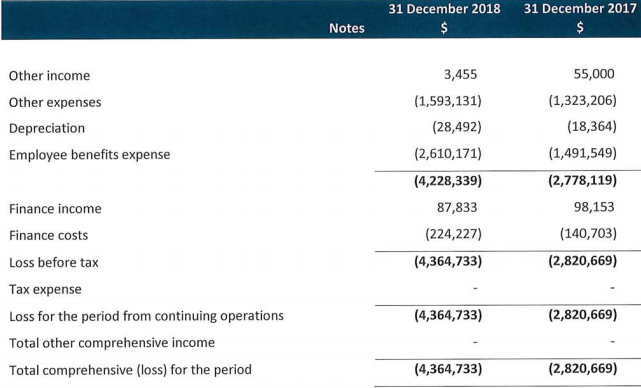

H1FY19 Financial Report: Total consolidated operating loss for the period was reported at $4,364,733, majorly due to the employee benefits expenses which were $2,610,171. Its basic and diluted loss per share was reported at $0.01.

H1FY19 P&L Statement (Source: Company Reports)

What to Expect: The independent confirmation and certification of the 2P energy reserve will allow LCK to advance with its negotiations with potential joint-venture partners on investment structures and the full-funding solutions for a commercial facility at the Leigh Creek Energy Project. The Company has signed a Heads of Agreement with South African based African Carbon Energy Pty Ltd for the negotiation of one or several of the Lease Agreement, Sale and Purchase Agreement and the Service Agreement, which is expected to help LCK to recover the majority of its engineering and plant costs of the Pre-Commercial Demonstration facility and to also have an early path to revenue.

Stock Recommendation: Leigh Creek’s share generated positive YTD return of 137.50% and is trading slightly towards the 52-week high price of $0.430. From the analysis standpoint, its current ratio for H1FY19 stands at 1.43x, which is better than the industry median of 1.25x, implying a better liquidity position to address its short-term obligations than its peer group. Its debt-equity ratio for H1FY19 stands at 0.14x, lower than the industry median of 0.32x, which indicates the company is less leveraged and utilises its own resources for funding needs. Hence, considering the aforesaid facts and current trading level, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.275 per share (down 3.509% on May 31, 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...