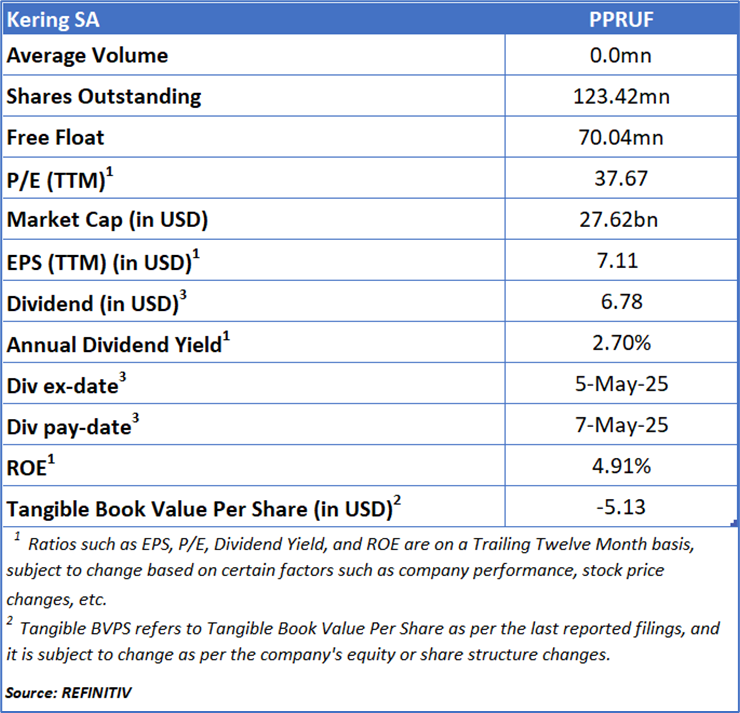

Kering SA

Kering SA (OTC: PPRUF) is a French company focused on the fashion sector, with core activities centered on producing and marketing premium luxury brand products.

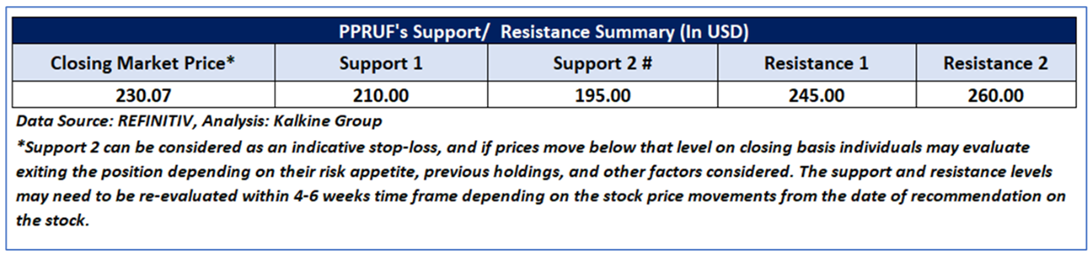

As per our previous Kalkine’s Global Tariff Report published on ‘PPRUF’ on July 08, 2025, Kalkine provided an ‘Buy’ stance on the stock at USD 230.07 based on fundamental analysis and the stock price has now moved up by ~ 19.01% since then and has breached resistance level 2.

Noted below are the details of support and resistance levels provided in our previous report:

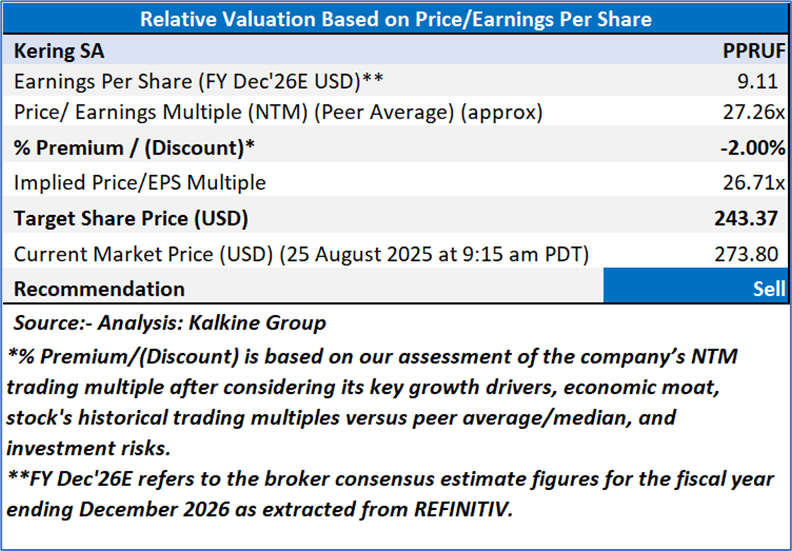

Rationale – Sell at USD 273.80

- Steep Decline in Revenue and Profitability: Kering reported a 16% drop in revenue to Euro 7.6 billion, with operating income plunging 39% and net income attributable to the Group falling 46% compared to the prior year. The recurring operating margin fell by 4.7 percentage points to just 12.8%, underscoring significant negative operating leverage. Weak store traffic, declining tourist flows, and subdued consumer demand in key markets such as Asia-Pacific and Japan were primary drivers of this downturn, reflecting broader luxury market headwinds.

- Severe Underperformance at Gucci: Gucci, the Group’s flagship brand and its largest revenue contributor, saw sales tumble 26% and recurring operating income collapse by 52%, reducing its margin from 24.7% to just 16%. Footfall fell sharply across all regions, and e-commerce sales suffered disproportionately, particularly in the American market, where customers with weaker disposable income curtailed luxury purchases. Wholesale sales at Gucci dropped by 42%, reflecting the brand’s continued rationalization of its distribution network. This deterioration placed considerable pressure on Group results given Gucci’s outsized contribution to revenues and earnings.

- Regional and Channel Weakness: Sales declines were broad-based across geographies: Asia-Pacific was down 21%, Japan down 20%, and both North America and Western Europe declined by 12–13% on a comparable basis. The downturn was linked to low tourist inflows, weak local demand, and adverse currency impacts. Across distribution channels, directly operated retail stores and e-commerce dropped 16%, while wholesale revenue for luxury houses contracted by 25%, reflecting reduced orders from US distributors and restructuring of wholesale networks. The digital business, once a growth lever, also faltered due to its exposure to more price-sensitive consumer segments.

- Pressure on Other Houses and Brand Challenges: Beyond Gucci, the “Other Houses” segment underperformed significantly, with revenue down 15% and operating income swinging to a loss of Euro 29 million from a profit of Euro 44 million a year earlier. Alexander McQueen’s restructuring weighed heavily, while Balenciaga faced ongoing weakness in Europe and Japan despite pockets of resilience in North America. The group’s reliance on a few strong brands highlighted its lack of balanced growth drivers, with several smaller houses failing to offset Gucci’s downturn.

- Rising Costs, Store Closures, and Strategic Uncertainty: Although Kering reduced operating expenses by 11% through cost discipline, profitability was still pressured by high marketing and retail investments necessary to support long-term brand desirability. The Group closed 41 net stores in H1 2025 (including Gucci and Saint Laurent units) and signaled up to 80 closures by year-end, pointing to ongoing structural adjustments in its retail footprint. Additionally, the departure of Gucci’s creative director and the transition to new leadership created short-term uncertainty around creative direction and brand momentum, further compounding operational risks during a weak demand cycle.

Valuation (Using Price/Earnings Multiple)

Share Price Chart

Conclusion

Kering’s first-half 2025 results reflect a deeply challenging period, marked by a sharp contraction in revenue (-16%) and profitability (-39% in operating income), driven largely by the steep underperformance of Gucci, whose sales and margins collapsed amid weak consumer demand and distribution rationalization. The downturn was broad-based, with Asia-Pacific, Japan, and Western markets all posting double-digit declines, while both retail and wholesale channels suffered from falling footfall, reduced orders, and slowing e-commerce activity. Other Houses also weighed on results, swinging into losses, and ongoing store closures and brand restructuring highlighted the Group’s vulnerability and strategic uncertainty. Overall, these trends point to a negative outlook, with weakened brand momentum and heavy dependence on a few flagship labels exacerbating the Group’s exposure to global luxury market softness.

Based on the notional gains, valuation downside and price action stance, a "Sell" recommendation on Kering SA (OTC: PPRUF) has been given at the current market price of USD 273.80 as on 25 August 2025 at 9:15 am PDT.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 25 August 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

AU

AU

Please wait processing your request...

Please wait processing your request...