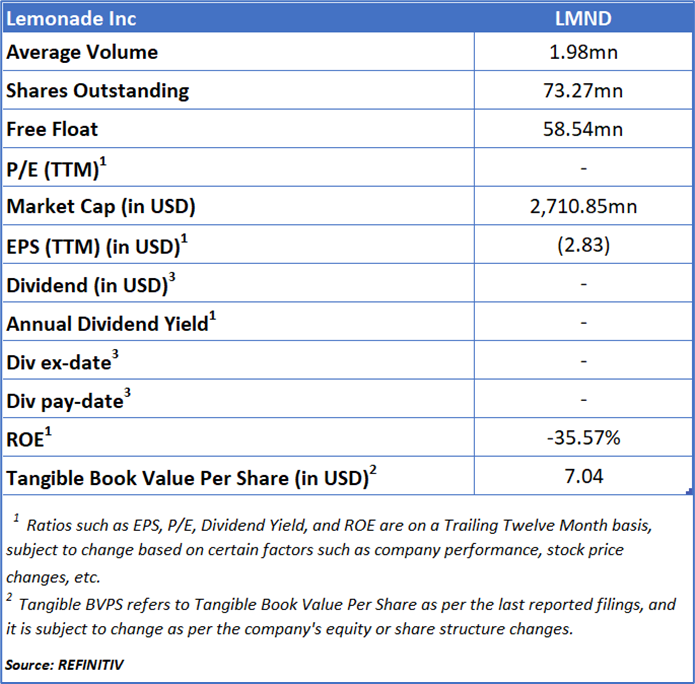

Lemonade Inc (NYSE: LMND)

Lemonade Inc (NYSE: LMND) provides insurance products across multiple categories, including renters, homeowners, auto, pet, and life insurance. The company operates in both the United States and Europe, including the United Kingdom, utilizing diverse distribution channels to reach its customers.

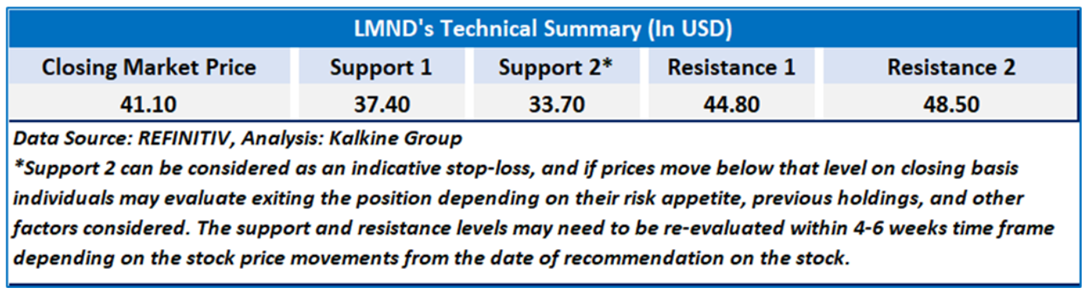

As per our previous Kalkine’s Diversified Opportunities Report published on ‘LMND’ on 26th June, 2025, Kalkine provided an ‘Buy’ stance on the stock at USD 41.10 based on fundamental analysis and the stock price has now moved by ~ 16.76% since then and is hovering around resistance 2.

Noted below are the details of support and resistance levels provided in our previous report:

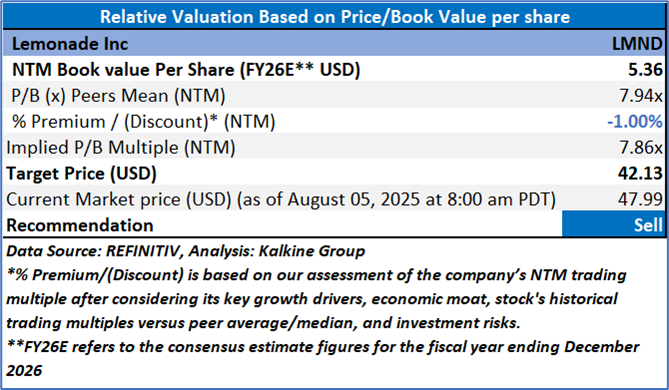

Rationale – Sell at USD 47.99

- Persistent Losses and Expanding Net Deficit: Lemonade Inc. remains in the red despite impressive revenue growth. In Q1 2025, the firm reported a net loss of USD 62.4 million, a sharp increase from the USD 47.3 million loss in Q1 2024. This worsening loss reflects mounting profitability pressures, fueled by higher marketing expenses and exceptional events like the California Wildfires. The year-over-year increase in per-share loss further underscores the ongoing difficulty in converting revenue growth into bottom-line gains.

- Rising Operating Costs Fueled by Expansion Efforts: Total operating expenses rose by 29% YoY, reaching USD 127.2 million, driven largely by intensified investment in growth and a one-time USD 6.9 million charge related to the California FAIR Plan. Spending on growth initiatives alone doubled to USD 38.1 million compared to the prior year. Although these investments are aimed at expanding offerings like Lemonade Car and entering new markets, the increased outlays are putting significant pressure on cash reserves and earnings. Without short-term financial returns, such a spending trajectory may not be sustainable.

- Ongoing Cash Flow Challenges and Extended Path to Profitability: Adjusted free cash flow remained deeply negative at USD 31 million for Q1 2025, compared to negative USD 18.9 million a year earlier. Management noted that the impact of wildfire-related events distorted results and that free cash flow might have been positive otherwise. Nonetheless, the recurring negative cash flow trend raises red flags about operational efficiency and long-term financial health. The company now expects to achieve positive Adjusted EBITDA only by late 2026, keeping investor optimism cautious.

- Weakening Retention and Margin Compression: Customer retention, tracked by annual dollar retention (ADR), fell to 84% from 88% YoY, mainly due to policy lapses under updated underwriting criteria. In addition, gross and adjusted gross profit margins declined to 26% and 30%, respectively, down from 29% and 31% in Q1 2024. These metrics highlight challenges in customer retention and operational cost management, especially amid rising claims and stiff competition in the digital insurance space.

- Increased Loss Ratios in Core Insurance Lines: Although the trailing twelve-month (TTM) gross loss ratio remained at 73%, Q1 saw a jump to 78%, mainly due to wildfire-related claims in California—exceeding the company’s targeted loss ratio range. Net loss ratio also climbed to 82% from 78% YoY. Notably, Lemonade Car continued to suffer from high loss ratios, largely due to the shorter duration of newer policies. While longer-tenured policies are showing improvement, the performance of newer business segments continues to drag on underwriting results, creating uncertainty around future profitability.

Valuation (Using P/B Multiple)

Share Price Chart

Conclusion

Lemonade Inc. continues to face mounting financial and operational challenges despite its top-line growth. The company’s net losses have widened significantly, fueled by surging operating expenses and strategic but costly growth initiatives. Persistent negative cash flow, declining customer retention, and shrinking profit margins further highlight inefficiencies. Elevated loss ratios—particularly in its car insurance segment—combined with a delayed profitability outlook through 2026, underscore concerns about the company’s sustainability and its ability to deliver long-term shareholder value.

Based on the notional gains, valuation downside and price action stance, a "Sell" recommendation on Lemonade Inc (NYSE: LMND) has been given at the current market price of USD 47.99 as on 05 August 2025 at 8:00 am PDT.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 05 August 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

AU

AU

Please wait processing your request...

Please wait processing your request...