Ford Motor Company

Ford Motor Company (NYSE: F) is an automobile company. The Company develops and delivers Ford trucks, sport utility vehicles, commercial vans and cars and Lincoln luxury vehicles, along with connected services. Its Ford Blue segment includes the sale of Ford and Lincoln internal combustion engine (ICE) and hybrid vehicles, service parts, accessories, and digital services for retail customers. Ford Model e segment primarily includes the sale of electric vehicles, service parts, accessories, and digital services.

Recent Business and Financial Updates

Key Positive Metrics

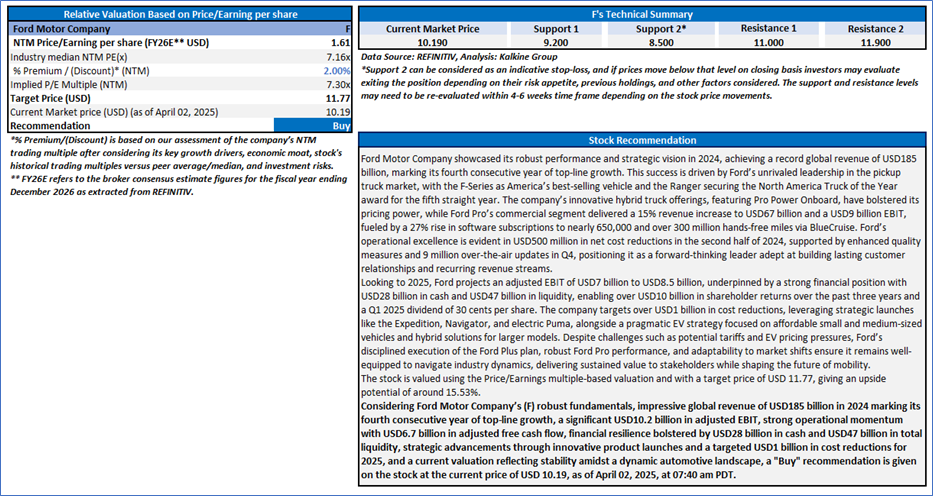

- Record Revenue Growth: Ford achieved a global revenue of USD185 billion in 2024, marking its fourth consecutive year of top-line growth, driven by strong franchises like the F-Series and Ranger.

- Market Leadership in Trucks: The F-Series remains America’s best-selling vehicle, and the Ranger won North America Truck of the Year, reinforcing Ford’s dominance in the pickup truck segment.

- Ford Pro Performance: Ford Pro’s EBIT reached USD9 billion with a 13.5% margin, supported by a 15% revenue increase to USD67 billion and a 27% rise in software subscriptions to nearly 650,000.

- Cost Reduction Success: Ford delivered USD500 million in net cost reductions in the second half of 2024 and targets over USD1 billion in 2025, enhancing operational efficiency.

- Strong Financial Position: Ford ended 2024 with USD28 billion in cash and USD47 billion in liquidity, enabling strategic flexibility and shareholder returns of over USD10 billion in the past three years.

Key Negative Metrics

- EV Segment Losses: Model e anticipates a USD5-USD5.5 billion loss in 2025, reflecting ongoing pricing pressures and significant investments in next-generation EVs and battery facilities.

- Tariff Risks: Potential 25% tariffs from Canada and Mexico could erase billions in industry profits, raise customer prices, and adversely affect U.S. jobs, posing a major risk to Ford’s operations.

- Q1 2025 Breakeven EBIT: Ford expects a breakeven adjusted EBIT in Q1 2025 due to reduced wholesales and unfavorable mix from launch activities, signaling a slow start to the year.

- Competitive Cost Gap: Despite progress, Ford acknowledges a persistent competitive cost gap that will take years to close, indicating ongoing operational challenges.

- Industry Pricing Pressure: A projected 2% decline in industry pricing in 2025, coupled with rising competition from Chinese OEMs, could strain Ford’s margins and revenue growth.

- Leadership Transition and Corporate Performance: Ford Motor Company extends its gratitude to all participants joining this earnings call, marking the debut of Sherry House as the incoming Chief Financial Officer and acknowledging John Lawler’s transition to Vice Chair. Under the leadership of CEO Jim Farley, 2024 proved to be a pivotal year, with Ford achieving a record-breaking global revenue of USD185 billion—the fourth consecutive year of top-line growth. This success is attributed to Ford’s robust fundamentals and its leadership in key segments, notably as the unrivaled leader in the pickup truck market, where the F-Series retained its title as America’s best-selling vehicle and the Ranger solidified its status as a profitable global franchise, earning the North America Truck of the Year award for the fifth consecutive time.

- Product Innovation and Market Dominance: Ford’s strategic focus on hybrid trucks has unlocked significant growth opportunities, leveraging unique features like Pro Power Onboard to secure pricing power and a dominant share of revenue in the pickup segment. Beyond trucks, Ford’s Transit family of vans continues to lead globally, reinforcing the company’s stronghold in commercial vehicles. Ford Pro, the commercial division, has seen substantial growth in high-profit series such as Super Duty and Transit Wagon, alongside a 27% increase in software subscriptions to nearly 650,000 and a 100% surge in telematics software adoption. This shift toward recurring revenue streams, including a 57% rise in mobile service units and over 300 million hands-free miles driven via BlueCruise, reflects Ford’s evolving relationship with customers, extending well beyond traditional sales.

- Operational Efficiency and Cost Discipline: Ford is undergoing a cultural transformation aimed at enhancing quality and reducing costs, yielding USD500 million in net cost reductions in the second half of 2024. This progress, driven by upgraded talent, third-party expertise, and best-practice implementation, represents an initial step toward closing the competitive cost gap over the next few years. The company has also adapted to evolving market dynamics, including a normalizing internal combustion engine (ICE) market, intensifying electric vehicle (EV) competition, and the rising influence of Chinese OEMs. For 2025, Ford projects an adjusted EBIT of USD7 billion to USD8.5 billion, with Sherry House providing detailed insights, while remaining cautious about potential policy shifts, such as tariffs, which could significantly impact the industry if prolonged.

- Global Market Trends and Strategic Response: The automotive industry faces a transformative landscape, with tariffs potentially wiping out billions in profits and increasing customer prices, alongside growing digital vehicle importance and Chinese OEM expansion. Ford, however, asserts control over its destiny through compelling product launches like the Expedition, Navigator, and electric Puma, paired with Ford Pro’s service enhancements. The company targets a multi-billion-dollar cost reduction opportunity by accelerating defect resolution, improving supplier quality, reducing complexity, and expanding over-the-air (OTA) updates—executing 9 million in Q4 2024 alone. Ford’s EV strategy focuses on affordable, high-volume small and medium-sized trucks and utilities, while prioritizing hybrids and extended-range electric vehicles (EREVs) for larger models to meet customer demands for range and affordability.

- Financial Outlook and Shareholder Commitment: Sherry House highlighted Ford’s 2024 performance, with a 5% revenue increase to USD185 billion, USD10.2 billion in adjusted EBIT, and USD6.7 billion in adjusted free cash flow, supported by a strong balance sheet boasting USD28 billion in cash and USD47 billion in liquidity. Ford remains committed to capital discipline, returning 40-50% of free cash flow to shareholders, evidenced by over USD10 billion distributed in the past three years and a Q1 2025 dividend of 30 cents per share. Segment performance showed Ford Pro’s EBIT at USD9 billion, Ford Blue at USD5.3 billion, and Model e achieving USD1.4 billion in cost reductions despite EV pricing pressures, setting the stage for a disciplined 2025 focused on quality and cost efficiency.

- Future Vision and Operational Resilience: Ford’s 2025 outlook anticipates challenges like lower industry pricing and tariff uncertainties, offset by USD1 billion in net cost reductions, primarily from warranty and material savings. The company expects a breakeven Q1 EBIT due to launch-related impacts, with stronger performance in the second half as cost benefits materialize. Ford Pro is projected to deliver USD7.5-USD8 billion in EBIT, while Model e anticipates a USD5-USD5.5 billion loss amid increased investment in next-generation EVs and battery facilities. Ford Blue targets USD3.5-USD4 billion in EBIT, with Ford Credit contributing USD2 billion in earnings before taxes. This disciplined execution of the Ford Plus plan underscores Ford’s transformation into a capital-efficient, high-margin enterprise, poised to navigate industry shifts while delivering value to stakeholders.

Company Valuation (Price/Earnings Per Share based relative valuation)

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is April 02, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

AU

AU

Please wait processing your request...

Please wait processing your request...