Newell Brands Inc

Newell Brands Inc (NASDAQ: NWL) is a worldwide consumer products company that operates through three main business segments: Home and Commercial Solutions, Learning and Development, and Outdoor and Recreation.

Key Financial Updates:

- Steady Performance Amid Macroeconomic Headwinds: Newell Brands reported its second quarter 2025 results, demonstrating operational resilience despite a challenging economic landscape. President and CEO Chris Peterson highlighted that the company achieved key financial targets including net sales, core sales, normalized operating margin, and normalized earnings per share—all within prior guidance. He noted the team’s adaptability and reaffirmed confidence in the company’s long-term strategy, which is aimed at enhancing core sales growth, improving margins, and sustaining healthy cash flow.

- Margin Expansion and Capital Market Confidence: Chief Financial Officer Mark Erceg emphasized continued improvement in profitability metrics. Gross margin expanded by 100 basis points year-over-year, reaching 35.4%, marking the eighth consecutive quarter of such gains. The company also enhanced its financial position by successfully refinancing USD 1.25 billion in debt through an offering that was four times oversubscribed. This level of interest, according to Erceg, reflects strong investor confidence in the company’s transformation strategy, which has supported top-line stabilization, balance sheet strengthening, and overall structural improvements.

- Mixed Financial Results and Segment-Level Challenges: During the quarter, Newell Brands recorded net sales of USD 1.9 billion, representing a year-over-year decline of 4.8%, driven by a 4.4% drop in core sales and the impact of unfavorable foreign exchange and business exits. Nevertheless, operating margin improved to 8.8% from 8.0%, supported by restructuring-related cost savings. Net income held steady at USD 46 million, and diluted earnings per share remained unchanged at USD 0.11. However, normalized net income declined to USD 101 million from USD 148 million in the prior year, while normalized diluted EPS fell to USD 0.24 from USD 0.35.

- Segment Performance Highlights: Among the company’s three business segments, the Home & Commercial Solutions division saw sales decline 7.3% year-over-year to USD 892 million, with a 6.0% drop in core sales. Despite modest growth in the Home Fragrance business, declines in the Commercial and Kitchen segments weighed on performance. Operating income fell sharply to USD 24 million from USD 48 million. In contrast, the Learning & Development segment remained relatively stable, with sales of USD 809 million and a marginal 0.5% core sales decline. Outdoor & Recreation revenues dropped to USD 234 million, but the segment turned a profit of USD 8 million, reversing a prior-year operating loss.

- Cash Flow and Balance Sheet Position: Newell reported an operating cash outflow of USD 271 million for the year-to-date period, compared with an inflow of USD 64 million during the same period last year. The decline was largely due to increased working capital usage, tariff-related costs, and comparison with the prior year’s lower bonus payouts. The company ended Q2 with USD 5.1 billion in debt and USD 219 million in cash and equivalents, compared to USD 5.0 billion and USD 382 million, respectively, a year ago. The recent debt refinancing helped address the 2026 maturities and improved financial flexibility.

- Revised 2025 Outlook Reflects Tariff Impact: Newell Brands updated its full-year 2025 guidance to reflect new tariff estimates, expecting an incremental cash tariff cost of approximately USD 155 million over 2024. The projected gross profit impact is about USD 105 million, equating to an after-tax EPS reduction of USD 0.21. For Q3 2025, net and core sales are projected to decline between 2% and 4%, while normalized EPS is forecasted at USD 0.16 to USD 0.19. For the full year, net and core sales are expected to decline by 2% to 3%, with normalized EPS forecasted between USD 0.66 and USD 0.70. The company also adjusted its full-year operating cash flow projection to USD 400–USD 450 million, factoring in elevated inventory-related tariff costs.

Technical Observation (on the daily chart):

Newell Brands Inc. (NWL) experienced a sharp 15% decline, breaking below both its 21-day and 50-day moving averages, signaling a bearish shift in trend. The RSI is near oversold territory at 32.8, reflecting weak momentum, while a spike in volume confirms strong selling pressure. An uptrend is expected with surging volume, indicating investors’ interest.

Newell Brands delivered a stable second quarter performance despite macroeconomic challenges, achieving key financial targets within guidance. The company continued its streak of gross margin expansion for the eighth consecutive quarter, supported by strong productivity and pricing actions. Operational improvements, disciplined cost management, and successful debt refinancing reflect strategic execution and investor confidence. While core sales declined, margin gains and financial flexibility position Newell well to navigate headwinds and pursue long-term growth.

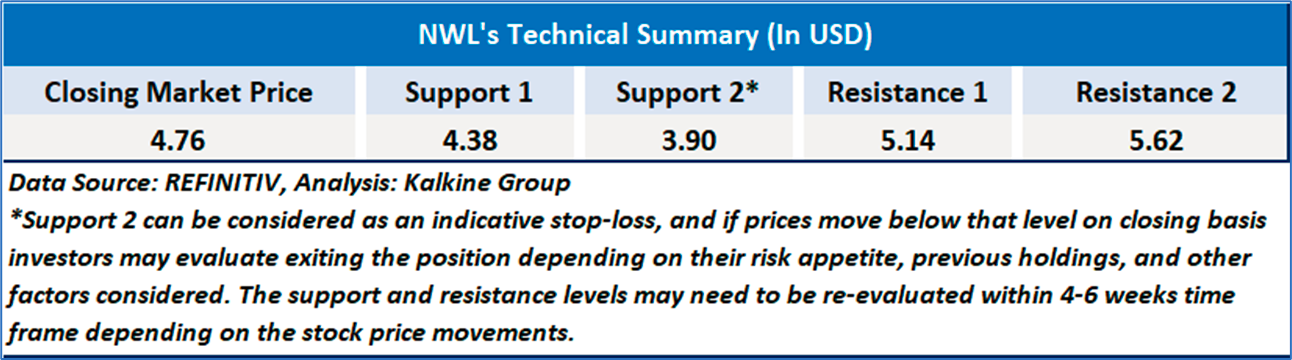

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Buy’ rating has been given to Newell Brands Inc (NASDAQ: NWL) at the closing market price of USD 4.76 as of August 01,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is August 01,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

AU

AU

Please wait processing your request...

Please wait processing your request...