Sims Metal Management Ltd

.PNG)

SGM Details

Mixed Market Update: Sims Metal Management Ltd (ASX: SGM) stock fell 5.66% on January 20, 2017 at the back of some negative market sentiments post its recent market update. The group now expects 1H FY17 underlying EBIT to be between $75 million and $79 million. 1H FY17 underlying EBIT is said to be a material improvement on previous guidance of underlying EBIT being similar to 2H FY16 of $63 million. However, SGM has stated that volatility in the price of coking coal, instability in Turkey, and winter weather challenges in North America need to be watched owing to their prevalence during 3Q FY17.

Focused on costs to offset the top line pressure: SGM has been focusing on their costs to combat the top line pressure. The group’s controllable costs fell by $137 million, leading to a 17% lower sales volume break-even point of the business. Accordingly, the group improved from their underlying NPAT loss of $18 million in the first half of FY16, to a net profit of $56 million in the second half of FY16. SGM is aiming for a return on capital of 10% or more by FY18. The group had a decent net cash position of $242 million at 30 June 2016 and had bought back over 8 million shares in fiscal year of 2016 as a part of their buy-back program at an average price of $7.59 per share. SGM even paid a final dividend of 12 cents per share during fiscal year of 2016. Meanwhile, the group’s optimization initiatives would continue to be implemented in the coming two years.

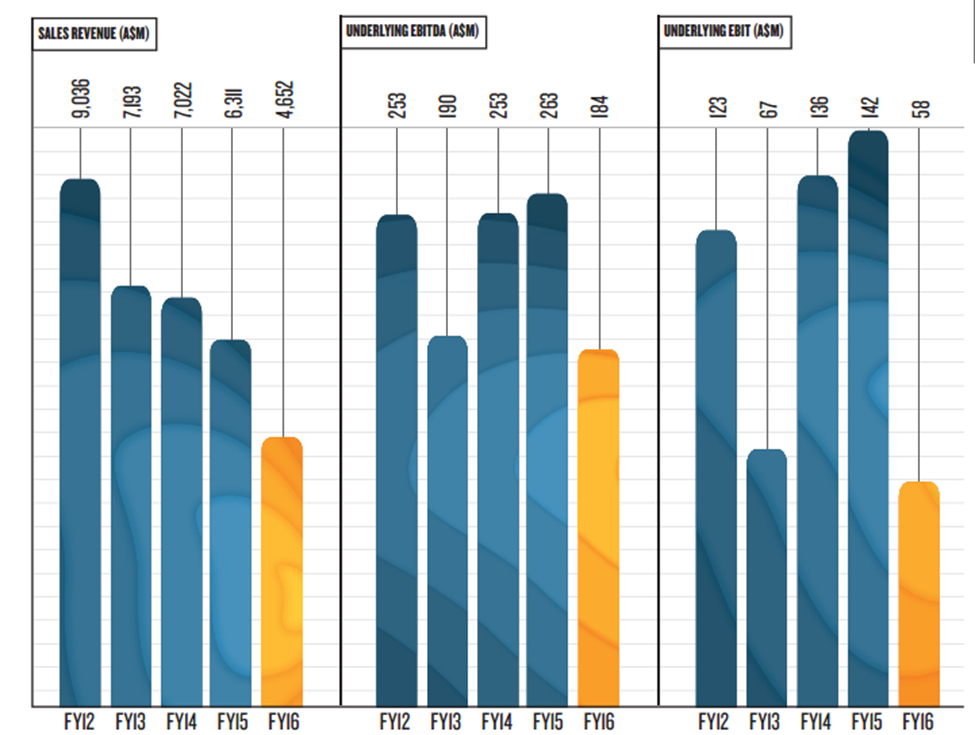

Despite growth efforts overall performance pressure continued: SGM reported an 18% decrease in their sales volumes in FY16 while their underlying NPAT plunged 63% year on year (yoy) to $38 million during the period. Oversupply of low-cost iron ore led to the ferrous scrap decline by over $30 per tonne during October 2015 which is the lowest level as compared to 2003 levels. Fiscal year of 2016 performance was impacted by a 40% ferrous scrap price reduction and a 33% contraction in their sales volumes, similar to the volume decline across their key market.

SGM FY16 performance (Source: Company Reports)

Recommendation: SGM’s stock rallied over 97.85% in the last one year (as of January 19, 2017) and we believe investors can book their profits in the stock now. The group witnessed a major hit late last year and was not able to recover for some time. Slowdown in the domestic steel consumption in China led to excess production into global markets. Despite the recent recovery in the commodity prices, the demand situation might still suffer at the back of macro-economic factors. Further, SGM is currently trading at a relatively higher P/E and has a moderate dividend yield. We recommend a “Sell” for the stock at the current price of $ 12.17, ahead of their interim 2017 results which would be released in February 2017.

.png)

SGM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...