Energy One Limited

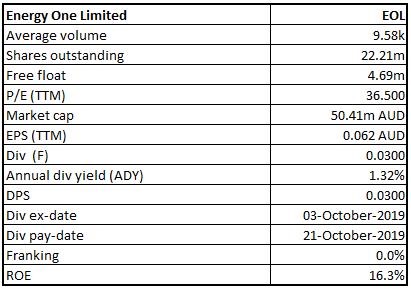

EOL Details

Increase in Borrowings on Account of Strategic Acquisition:Energy One Limited (ASX: EOL) is engaged in providing consulting services, software applications and supportive services to the Energy Sector. Recently, the company informed that one of its Directors named Andrew Bonwick, acquired 27,027 share rights.

FY19 Operational Highlights for the Period ended 30 June 2019: EOL announced its annual results, wherein the company reported revenue of $16.065 million, up 62% on y-o-y basis, aided by the positive contribution from Contigo. Underlying EBITDA, before one-off acquisition costs, came in at $3.851 million as compared to $2.5 million in the previous financial year. NPAT for FY19 came in at $1.309 million as compared to $1.040 million in FY18. During the year, the company secured a $7.28 million debt facility for the acquisition of Contigo. The company reported higher employee benefits expense at $8.233 million as compared to $4.964 million in the previous financial year. The company reported a decline in EBITDA margin on account of the inclusion of acquisition cost. Contigo has contributed $4.8 million to the top-line and $0.96 million to Group EBITDA. The acquisition being earnings accretive, contributed to a lift to 1.1% per share in FY19. The company reported higher direct project costs at $0.79 million as compared to $0.257 million in the previous financial year. The company reported cash from operating activities at $3.44 million, cash used for investing activities at $8.805 million and cash flow from financing activities at $6.854 million during FY19.

.png)

FY19 Income Statement Highlights (Source: Company Reports)

Guidance: The company expects that EBITDA margin is likely to improve with the product release for 5min settlements and the operational improvements being implemented in the UK. The acquisition of Contigo is likely to enhance the workforce of EOL and will help the company in the provision of high-quality ETRM solutions to a specialized and deep European market.

Stock Recommendation: The stock is quoting at $2.270 with a market capitalisation of ~$50.41 million. The stock has generated stellar returns of 41.88% and 118.27% in the last six months and one year, respectively. The stock is available at a price to book value multiple of 5.6x on trailing twelve months (TTM) basis as compared to industry median (Software & IT Services) of 3.6x. With a strong presence across the UK market, EOL will focus on European exposure with higher marketing efforts and product enhancement. The company will further focus on driving organic growth and also looks forward to strategic growth through prudent acquisitions and other strategic relationships related to highly complementary businesses. Considering the price movements and overvalued position in comparison to the industry, we are of the view that most of the positives are factored in at the current juncture. Thus, looking at the increasing debt levels, valuations, higher staff expenses and other factors, we suggest investors to book profit at the current level and recommend a ‘Sell’ rating on the stock at the current market price of $2.27 as on 20 December 2019.

EOL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...