IDP Education Limited

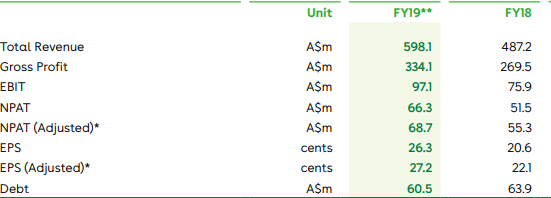

FY19 Financial Performance (as at 30 June 2019): IDP Education Limited (ASX: IEL) is in the business of providing education services and has a market capitalisation of ~A$3.99 billion as on October 10, 2019. With respect to the financial year ended June 30, 2019, interim dividend amounting to 12.0 cents per share (franked at 50%) was paid on March 29, 2019. Additionally, it was stated that the final dividend amounting to 7.5 cents per share (franked at 45%) was declared on August 21, 2019, which was payable on September 26, 2019 to the shareholders, who registered on September 10, 2019. The performance of IDP in FY19 reflects the continuation of robust organic growth that it has been witnessing over the past 7 years. The growth was supported by ongoing global growth in the international education industry and central role of English as a key global language. The company has a global footprint and diversified business model, which benefits from global trends. The company’s total Revenue amounted to A$598.1 million in FY19, which reflects a rise of 22.8% on a YoY basis. Its NPAT stood at A$66.3 million, implying an increase of 28.8% on a YoY basis.

Financial Performance (Source: Company Reports)

Region-wise Financial Summary:

Asia:Asia posted a robust year of growth and it continued to be the primary driver of the company’s profitability with 73% of group EBIT coming from the region. The region includes both India and China, which are the primary engines of growth for international education industry.

Australasia:The performance of the Australasian segment showed signs of improvement during the year. The segment has witnessed a decline in earnings for the last 4 years with the competition in English language testing market reducing the IELTS volumes in ANZ (or Australia and New Zealand).

Rest of World:Rest of World recorded a decent performance for the year and Middle East, Canada, Nigeria and the UK supported the growth in the segment. The Middle East’s underlying performance was because of robust IELTS volume growth and the total test volumes throughout the region were up.

Outlook:The company is introducing a net promoter score system across key touchpoints in order to support its focus towards delivering superior customer service. In 1H of financial year, the company would be rolling out Digital Campus in Chennai. This would be bringing together 400 of the digital marketing, design as well as technical resources, allowing the rapid product development and customer-centric innovation. The company would continue to expand client services so that it can provide data-driven insights and marketing solutions via IDP Connect.

Stock Recommendation: The total revenues of IDP Education Limited has witnessed a CAGR growth of 17.87% in the time span of previous FY 2015- FY 2019 and, thus, it can be said that IEL is possessing respectable capabilities to garner revenues which might support its long-term growth prospects. The company’s net margin stood at 11.1% in FY19, which implies an improvement from FY18 figure of 10.6% and, thus, it can be said that the company’s capabilities to convert its top-line into the bottom-line have improved. IEL’s current ratio stood at 1.31x in FY19, an improvement from FY18 figure of 1.02x. Currently, the stock is trading towards the upper band of the 52-week trading range of $8.45-$19.84 with higher PE multiple of 59.75x. Hence, considering the aforesaid facts and current trading levels, we have a watch view on the stock at the current market price of $15.470 (down 1.402% on 10 October 2019), and suggest investors to wait for better entry levels.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...