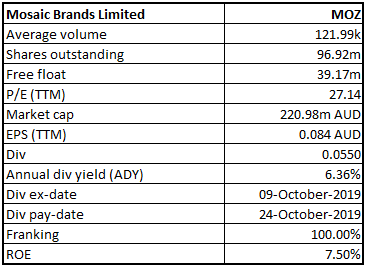

Mosaic Brands Limited

MOZ Details

Substantial Increase in Revenue: Mosaic Brands Limited (ASX: MOZ), formerly known as Noni B Limited is engaged in the retailing of women’s apparel and accessories. As on 23 December 2019, market capitalisation of the company stood at $220.98 million. On 23 December 2019, the company, under Section 708A(5)(e) of the Corporations Act 2001, announced that shares issued on 16 December 2019, will rank equally with all other shares on issue.

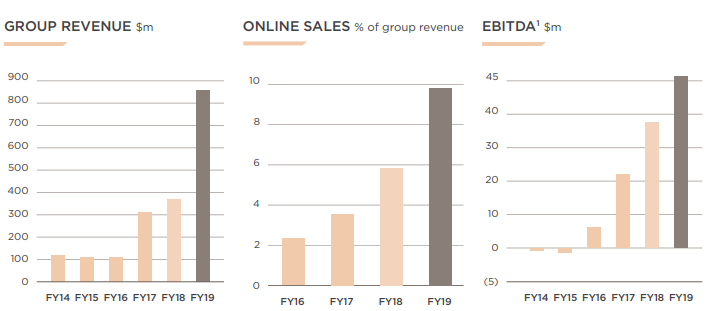

In the recently held AGM, the Management stated that the company acquired five brands from Specialty Fashion Group, which led to the increase in revenue by 136.8% to $881.9 million in FY19 from $372.4 million in the previous year.The company reported earnings per share of 8.4 cents for the period as compared to 21.3 cents in the year-ago period, impacted by the higher depreciation cost and restructuring costs. Total depreciation for FY19 amounted to $21.4 million as compared to $10.06 million reported in the year-ago period. Underlying EBITDA for the period came in at $45.5 million, an increase of 22% on a year over year basis. Net profit after tax stood at $8.2 million as compared to $17.3 million reported in the year-ago period. The balance sheet is also in good shape with a positive operating cash flow of $23.5 million in FY19. As a result of the strong financial position and the increase in underlying profitability, the company paid fully franked dividend of 14.5 cents per share for the year, up 11.5% over the previous year. The company existed the year with cash and cash equivalents of $36.61 million as compared to $58.69 million at the end of FY18.

Scott Evans, Director of the company, has recently acquired 43,555 Shares in Mosaic Brands Limited for a consideration of $2.89 per share. The company has changed its name from Noni B Limited to Mosaic Brands Limited.

Growth Opportunities:The company expects underlying EBITDA of $75 million in FY20. The company plans to open up to 100 new stores in FY 2020. The Group is optimistic about the potential to be unlocked by greater assessment of the Group’s data, store expansion and online strategies. MOZ looks forward to further growth in revenue and earnings in FY2021 and beyond.

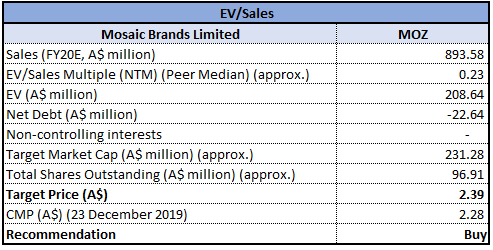

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week low of $2.260. Over the period of FY15 to FY19, the company witnessed a CAGR of 63.76% in gross profit. During the year, gross margin stood at 56.6%, higher than the industry median of 24.2%. The company aims to standardise operating platform in order to enhance shopping experience and increase time to market for new site improvements. The company aims to increase product inventory on all the sites, thereby delivering a multi-channel experience to the customer. The company intends to continue its team investments to meet the growing demand of customers and achieve long-term growth. In FY19, database pertaining to e-mail address increased to 4.4 million, whereas phone number increased to 3.4 million. Considering the aforesaid facts, we have valued the stock using one relative valuation approach, i.e., EV to Sales multiple and arrived at a target of mid-single-digit upside (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.280 on December 23, 2019.

MOZ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...