Steadfast Group Limited

.png)

SDF Details

Underlying Earnings Driven by Organic and Acquisition Growth: Steadfast Group Limited (ASX: SDF) is primarily engaged in the provision of services to Steadfast Network brokers, distribution of insurance policies, and related services.- The company recently updated that Challenger Limited became a substantial shareholder of the group with the voting power of 5.02%.

Closure of IBNA Takeover Offer: The company recently updated that it has received the acceptances from IBNA shareholders for its takeover offer for IBNA Limited and has obtained an interest in 100% of IBNA shares.

Share Purchase Plan: In a recent announcement, the company notified that it has raised a total of approximately $19 million via a Share Purchase Plan, with new ordinary shares to be issued at a price of $3.38 each.

Dividend: On 20 September 2019, the company paid a dividend amounting to AUD 0.0530 per ordinary share issued.

FY19 Financial Highlights: During the year ended 30 June 2019, the company reported underlying revenue amounting to $688.3 million, up 21.4% on prior corresponding year. Underlying EBITA for the year amounted to $193.3 million, representing an increase of 17.8% on pcp. Underlying NPAT stood at $89.2 million, up 19.0% on prior corresponding year. During the year, the company reported underlying EPS of 11.27 cents per share, increasing 16.0% on the previous year.

Gross written premium for the Steadfast Network was reported at $6.1 billion, representing an increase of 16% on prior corresponding period. The growth in GWP was driven by moderate price increases by insurers, new brokerages joining the network and expansion in volumes. GWP for Steadfast Underwriting Agencies stood at $1.17 billion, up 28% on FY18 on the back of an increase in price by insurers and growth in market share.

.png)

FY19 Financial Results (Source: Company Reports)

Potential Acquisition of PSF Rebate: The company is seeking expression of interest from Steadfast Network Brokerages to renounce their rights to professional service fee (PSF)rebates in return for Steadfast shares or cash.

FY20 Guidance: In FY20, the company expects underlying EBITA in the range of $215 million - $225 million. Underlying NPAT for the year is expected to be in the range of $100 million - $110 million. In addition, growth in underlying diluted EPS is expected to be in the range of 5% - 10%.

Stock Recommendation: The stock of the company generated returns of 13.12% over a period of 6 months and is currently trading towards its 52 weeks high level of $3.890. In FY19, the company reported a decent growth across all key metrics including revenue, EBITA and NPAT on the back of increase in premium price and volumes along with the addition of new brokerages in the Network. The period was also marked by a strong balance sheet with net assets amounting to $1.1 billion. However, the company also notified that the IBNA transaction and potential PSF Rebate Acquisition will adversely impact the statutory NPAT in FY20. In the light of aforesaid factors and current trading levels, we advise investors to book the profit at the current juncture and recommend a "Sell" rating on the stock at the current market price of $3.550, down 1.934% on 30 September 2019.

SDF Daily Technical Chart (Source: Thomson Reuters)

Charter Hall Retail REIT

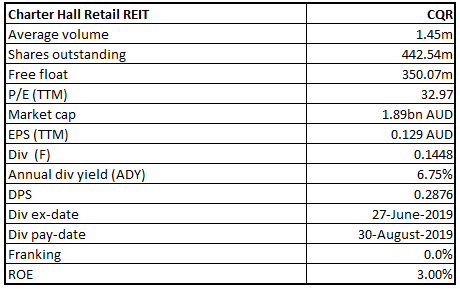

CQR Details

Operating Earnings & Distribution Growth in-line with Guidance:Charter Hall Retail REIT (ASX: CQR) is primarily engaged in property investment.

Sale of Interest in RP6: Charter Hall Retail REIT recently acquired Charter Hall Group’s 20% stake in Pacific Square, Maroubra and Bass Hill Plaza. The Group will maintain its exposure to the assets through its co-investment in CQR. The assets are currently owned by the Charter Hall Retail Partnership No. 6 Trust (RP6) and is valued at $281 million. The remaining stake in the trust is owned by Mercer, a global consultancy firm. The acquisition was funded by the proceeds from recently announced divestments.

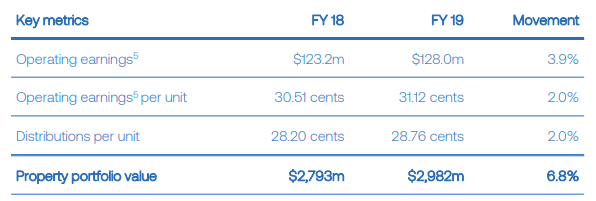

Highlights of FY19 Results: During the year ended 30 June 2019, the company reported operating earnings amounting to $128 million, up 3.9% on prior corresponding period. Statutory profit for the year stood at $53.1 million. Distribution for the year amounted to 28.76 cents per unit, representing an increase of 2% on prior corresponding period. At the end of the period, the company reported balance sheet gearing of 32.9% with undrawn debt capacity of $143 million.

FY19 Key Highlights (Source: Company Reports)

FY20 Guidance: Operating earnings in FY20 are expected to report growth in the range of 1.5% - 2.0%. Distribution payout ratio range for the year is expected to be at 90% - 95%.

Stock Recommendation:The stock of the company generated negative returns of 0.47% and 4.27% over a period of 1 month and 3 months, respectively. In FY19, value of the company’s portfolio increased by $189 million due to development and transaction activity, maintaining portfolio occupancy at 98.1%. During the year, the company continued to manage its capital and debt position to ensure a wise capital structure. It has refinanced the existing debt facilities and has no debt maturing until FY22. In FY19, the company also acquired three high-quality assets with Rockdale Plaza, NSW, Gateway Plaza, Vic and Campbellfield Plaza, Vic. In addition, the recently acquired assets in Sydney represent a significant addition to the portfolio with strong income growth prospects for the fund. Based on the above factors, we give a “Buy” recommendation on the stock at the current market price of $4.250, down 0.235% on 30 September 2019.

CQR Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...