Myer Holdings + Cromwell Property Group - 2 stocks to sell

Sep 15, 2015 | Team Kalkine

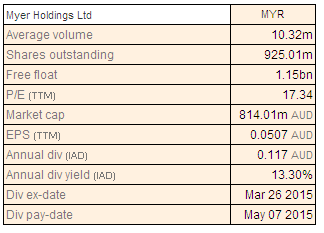

Myer Holdings Ltd (MYR)

Result Summary

The Company has announced its results for the full year FY 2015 as well as the launch of a fully underwritten 2 for 5 accelerated pro rata non-renounceable entitlement offer to raise approximately $ 221 million at an offer price of $ 0.94 per share. The proceeds of the offer will be used to reduce debt and provide the balance sheet strength and flexibility to implement the new Myers Strategy. The company believes that this new strategy will create a business model that is sustainable which will maintain and improve its competitive position and return the business to sustainable profit growth in the future.

Myer Dividends (Source - Company Reports)

Among the highlights of the FY 2015 results are sales growth of 1.7% (1.1% on a comparable store sales basis) to $ 3.19 billion, a decline in operating gross margins by 53.4 basis points to 40.4%, an increase of 3.3% in cost of doing business to $ 1.06 billion, a decline of 11.6% in EBITDA to $ 223.2 million, basic earnings per share of 13.2 cents per share compared to 16.8 cents per share and statutory basic EPS of 5.1 cents per share. No dividend has been declared by the board. CEO and managing director Richard Umbers said that these results support an agenda of comprehensive change. The decisions taken for the New Myers Strategy will lead to changes in both operations and the store network and result in increased productivity and more efficient footprint.

Way forward

FY 2016 will be the transition year for the Company in which significant investments are being made for future growth and the benefits of these investments are expected to be felt late in 2016 and the years after. Following this, the Company expects to return to a position of sustainable profit. As a result and inclusive of the impact of the entitlement offer, NPAT for FY 2016 will be in the range of $ 64 million-$ 72 million excluding the implementation costs of the New Myers Strategy. Significant items are expected to be in the range of $ 35 million-$ 45 million and capital expenditure is expected to be in the range of $ 100 million-$ 120 million.

MYR Daily Chart (Source - Thomson Reuters)

We notice that the struggling department store operator is looking for a way out of its decline and is therefore asking shareholders to fund the strategy involving a refreshed range of new products and a better user experience for shoppers. The Company is appealing to investors by pressing the shares at a discount to the prevailing price. The bright spot is that the entitlement offer is fully underwritten and forms part of the firm financing for the $ 600 million that the Company says it needs over the next five years. However, the offer coincides with the decline in performance from the Company for FY 2015. The strategy is high-risk and may appeal to ones having a high appetite for risk.

Accordingly, we put a SELL recommendation for this stock at the current price of 0.855.

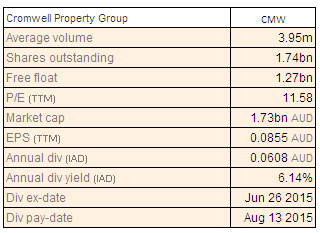

Cromwell Property Group (CMW)

Portfolio snapshot and growth

The global property investment manager has reported profits of $ 144.9 million for FY 2015 compared to $ 146.7 million in the previous year. The operating earnings per security were 8.35 cents per share and the distribution per security was up 3% at 7.86 cents per share. CEO Paul Weightman described the performance as robust and reflected the focus on active management of the core property portfolio and growing the fund management business. He pointed out that the current sales activity partially represents some of the pricing at the peak of the cycle for prime office property, particularly in, Sydney and Melbourne. Consistent with the view of the Company that it invests only where it can deliver superior risk-weighted returns through the entire cycle, the Company was a net seller of assets with 321 Exhibition Street in Melbourne settling for $ 206.9 million and 43 Bridge Street in Hurstville being agreed for a sale price of $ 37 million. Both transactions will be settled after the end of the financial year. After the end of FY 2015, Bligh House in Sydney has been sold for $ 68 million and Terrace Office Park is under an unconditional contract for sale for $ 31 million. Portfolio valuations increased by 1.1% though some increases were partly offset by decreases in properties with vacancies or short-term lease profiles.

FY15 Results (Source: Company Reports)

As of 30 June 2015, the property portfolio had Weighted Average Lease Expiry of 5.7 years and a vacancy rate of 5.4% by gross income compared to the national CBD average of 12.2%. Government and government funded and owned entities accounted for 45% of gross income. The Company expects market conditions to remain soft for the next 12 to 18 months but some growth is expected in FY 2016 because of biannual reviews to be conducted in a number of the larger assets.

Cromwell Dividends (Source - Thomson Reuters)

Acquisition and Earnings Scenario

Earnings from wholesale fund management increased to $ 2.6 million because of increased activity from the Australian wholesale fund, Cromwell Partners Trust and a contribution for part of the year from Valad Europe. The acquisition of Valad Europe advances the stated objective of generating 20% of group earnings from fund management because it is a respected and established fund management business. It has 27 funds covering more than 400 properties and 3700 tenants over 4.2 million square meters. Earnings from retail fund management declined from $ 3.5 million in the previous year to $ 1.4 million because of the lower transaction fees generated because of caution in acquiring new assets for investors at this stage of the property cycle.

The Company's strategic objective to consistently grow distributions by 3% every year continues to remain as it is. Earnings for FY 2016 are not expected to be less than 9 cents per share compared to 8.35 for the previous year and distribution should not be less than 8.10 compared to 7.86. This works out to an earnings per security of 8.65% and distribution per security of 7.79%, respectively. However, we believe that it will be at least 12 or 18 months before there is any upside in the stock given the drag from domestic expiries and high capex.

CMW Daily Chart (Source - Thomson Reuters)

Accordingly, we put a SELL recommendation for this stock at the current price of 0.975.

Disclaimer The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

.PNG)

Please wait processing your request...

Please wait processing your request...