McMillan Shakespeare Limited

-

The company which is based in Melbourne provides remuneration, asset management, and finance services to public and private organizations in Australia. It operates in two segments, Group Remuneration Services and Asset Management. The Group Remuneration Services segment provides salary packaging services, including salary packaging benefit administration and processing; remuneration policy design; fringe benefits tax and motor vehicle lease management services to employers from state and federal governments, hospitals, charities as well as private sector organizations. The Asset Management segment offers financing and ancillary management services relating to motor vehicles, commercial vehicles, and equipment. It provides car and home insurance products.

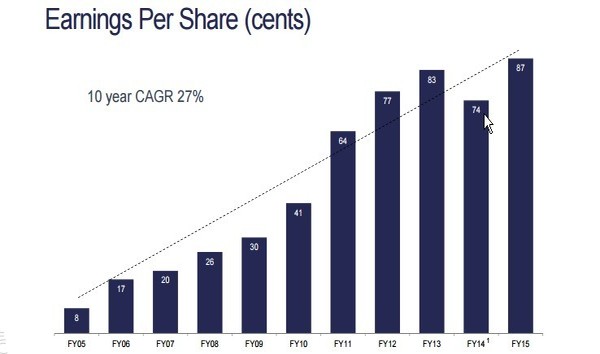

Earnings Per Share (Source - Company Reports)

Results for FY 2015

Earnings Per Share (Source - Company Reports)

Results for FY 2015

-

The company reported record financial results for the year with EBITDA up by 20%, NPAT by 23% and EPS by 18%. The company has entered a new stage in its evolution with step changes in scale, competitiveness and opportunity and has created a leading presence for itself in the market for independent consumer car finance. It has maintained its financial strength through strong cash flow generation and growth has been supported by a strengthened management team.

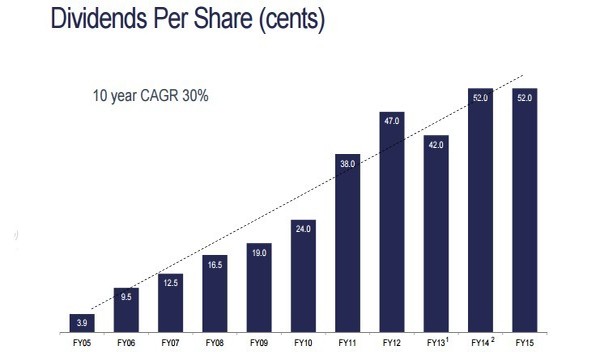

Dividends Per Share (Source - Company Reports)

Operational highlights

-

Among the operational highlights for the year, there is significant growth and profitability within the Group Remuneration Services business where operating revenues increased by 12%, EBITDA by 25% and NPAT margins continue to stay strong. The approach to growth in Asset Management has been selective and there is a stable Australian asset book with conservative gearing levels while the UK business is showing momentum and has commenced the sale of "Lifestyle leases". A new complementary segment called Retail Financial Services has been created and the acquisitions completed of Presidian on 27 February 2015 and of UFS after the year-end on 31 July 2015. This ensures scale across the value chain for new and used vehicles and synergies and new growth opportunities have been identified and the integration is well advanced and on track. Additional contracts were secured from existing clients and there is a good pipeline of new business extending into FY 2016. Improved funding arrangements were concluded with financial providers and productivity benefits from IT investment continue to be generated. The Guaranteed Future Value product has been well received by the market and all the leading indications are favourable.

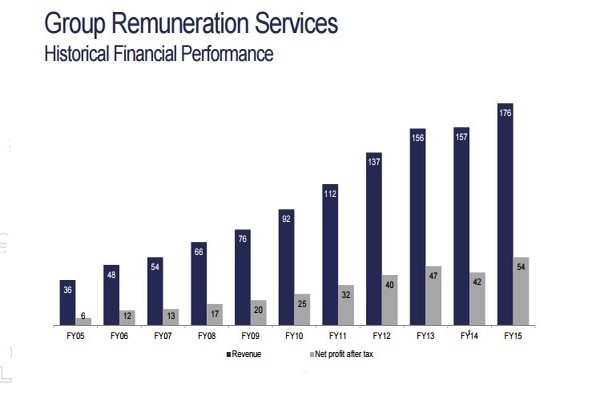

Group Remuneration Services (Source - Company Reports)

Financial highlights

-

Consolidated NPAT was $ 67.5 million a growth of 23% over the previous year and the underlying NPAT was $ 70.2 million which was up 26% over the previous year. Group Remuneration Services NPAT was $ 54.3 million up 29% over the previous year, Asset Management NPAT was $ 11.3 million down 17% from the previous year and Retail Financial Services NPAT was $ 3 million representing four months of trading in Presidian following the acquisition. The final dividend fully franked was $ . 27 cents per share making a total of 52 cents per share fully franked and the total payout ratio is 63%. The diluted EPS of 86.8 cents per share is up 19% over the previous year while the basic EPS of 87 cents per share is up 18% over the previous year. EPS is based on the underlying NPAT of 90.6 cents per share which is up 21% over the previous year. The annualised return on equity is 25% and the return on capital employed is 24%. There is a strong operating cash flow of $ 79 million pre capital expenditure, tax and increases in the fleet.

MMS Dividends (Source - Thomson Reuters)

Group business segments

-

Group Remuneration Services offers administrative services in respect of salary packaging, facilitates the settlement of motor vehicle novated leases but does not provide financing and ancillary services associated with motor-vehicle novated leases such as insurance and aftermarket products. Customers are typically hospitals, health and charity workers and public and private sector lease products are also offered. It has over 800 customers who have around 1 million employees. Revenues were around $ 176 million, EBITDA was $ 79.69 million and underlying NPAT was $ 55.52 with an underlying margin of 31.5%.The NPAT for FY 2015 of $ 54.3 million was $ 12.3 million or 29% higher than the previous year. The business is characterised by strong sales and distribution capabilities and a number of significant new business wins and there is a good pipeline of new business opportunities. Free operating cash in excess of NPAT was generated and the core operating contribution of $ 69.6 million represents an increase of 25% over the previous year

MMS Daily Chart (Source - Thomson Reuters)

-

Asset Management offers financing and ancillary management services associated with motor vehicles, commercial vehicles and equipment. It is located in Australia, New Zealand and the United Kingdom. The customer base is predominantly corporate and there are over 300 customers as well as selected brokers. Revenues were $ 188.06 million, EBITDA was $ 19.92 million and underlying NPAT was $ 11.28 million with a margin of 6%.The business showed a decline in NPAT compared to the previous year and the decline was primarily due to asset impairment charges of $ 3.2 million and credit losses of $ 0.4 million. Assets under Finance declined marginally to $ 311 million and the market remains highly competitive with pressure on margins and fees. The inertia of fleets remains the same as the previous year and interest-rate risk is managed through hedging facilities. There is a pipeline of new business opportunities.

-

Retail Financial Services offers retail brokerage services and aggregation of finance origination and extended warranty cover but does not provide financing. It services a retail customer base as well as a dealer, broker and retail network. There are more than 2500 active dealers and 450 insurance brokers. Revenues were $ 23.1 million, EBITDA was $ 5.5 million and underlying NPAT was $ 4.5 million with a margin of 19.8%.

-

The company continues to deliver strong results and continues its impressive growth and, in fact, the CAGR has been 29% annually since it listed on the ASX in 2004. It trades at a reasonable P/E ratio and its track record and future prospects suggests that this would be a good investment. We recommend that you buy the stock at the current price of $12.85.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...