Boral Limited

.png)

BLD Details

Investigation on Financial Irregularities: Boral Limited (ASX: BLD) is engaged in the manufacturing and supply of building and construction materials. The market capitalisation of the company stood at A$5.77 Bn as on 6th December 2019. The company recently advised that it has identified certain financial irregularities in its North American Windows business, which involves misreporting including in relation to inventory levels as well as raw material and labour costs at its Windows plants. It was also mentioned in the release that with oversight by the Board and senior management, a privileged and confidential investigation is being conducted by lawyers retained by the company, who have also engaged forensic accountants to assist the investigation. The following picture provides an overview of key financial metrics for FY19:

Financial Metrics (Source: Company Reports)

Anticipation of Rise in Fly Ash Volumes:With respect to Boral North America, the company is half-way through a four-year growth plan, which is seeing BLD to progressively deliver the benefits of the Headwaters acquisition. In addition, the acquisition synergies are being delivered, in-line with plan, and already delivered US$71Mn of benefits. The company is confident that the remaining US$44 million of additional synergies would be delivered in FY2020 and FY2021, to achieve its total targeted synergies of US$115 million.

The company’s legacy fly ash business has been impacted by the closure of numerous utilities. Resultantly, fly ash volume increases from the synergies as well as growth initiatives have been offset by the lower volumes associated with utility closures. It anticipates to witness a modest increase in fly ash volume in FY2020 and more significant volume growth in the coming years.

Valuation Methodology: Price to Earnings Multiple Approach

P/E Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation:FY20 earnings guidance are unchanged, with property earnings to be in the range of $55-$65 million.We have valued the stock using P/E valuation multiple approach and arrived at the target price, offering an upside of lower single digit (in percentage terms). Therefore, we recommend a “Hold” rating on the stock at the current market price of A$4.610 per share, down 6.301% on 6th December 2019, taking cues from the release related to the investigation in North America Business.

BLD Daily Technical Chart (Source: Thomson Reuters)

Fletcher Building Limited

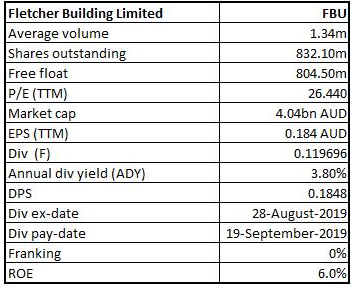

FBU Details

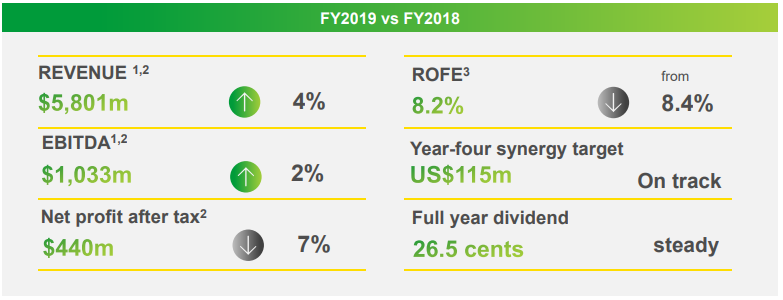

Chairman’s Address to Shareholders:Fletcher Building Limited (ASX: FBU) is into building products, distribution, laminates & panels, concrete, construction and steel and has a market capitalisation of A$4.04 Bn as on 6th December 2019. Recently, the CEO of the company addressed the shareholders at 2019 Annual General Meeting and stated that revenue for the financial year 2019 amounted to $9.3 billion and net earnings stood at $164 million. The bottom-line was impacted by $234 million of significant items, which comprised of two main components – (1) $140 million of write-offs associated with the sale of its international businesses (Formica and RTG), and (2) Around $78 million of costs associated with the intervention and reset of the Australian businesses.

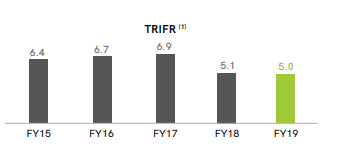

During FY19, the priority of the group was to materially strengthen the balance sheet and to provide a robust platform for the execution of the go-forward strategy.FBU’s net debt witnessed a decline from $1.3 billion at June 2018 to $325 million at June 2019, primarily due to highly successful Formica divestment. The following picture provides an idea of total recordable injury frequency rate (TRIFR) for the financial year 2019:

TRIFR (Source: Company Reports)

Supportive Medium-Term Outlook:For FY20, the company anticipates EBIT before significant items in the ambit of $515 million to $565 million. In New Zealand, FBU anticipates residential consents to ease slightly off current peaks, non-residential construction to remain at similar levels, as well as infrastructure spend to ease in major roading with a move to road safety, water, and rail. When it comes to Australia, the company forecasts the contraction in residential to continue, and the non-residential as well as East Coast infrastructure market to be broadly flat.

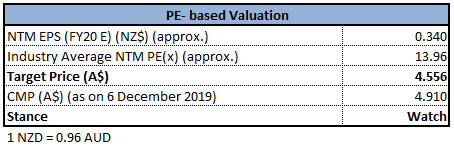

Valuation Methodology: Price to Earnings Multiple Approach

P/E Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation: The company would continue to maintain a prudent approach to balance sheet management. The Board of the company has paid a total dividend amounting to 23 cents per share for the financial year 2019. This total dividend includes a final dividend of 15 cps and an interim dividend of 8 cents per share. The dividend policy of the company remains unchanged to the pay 50-75% of net profit before significant items. At the current market price of $4.910, the stock is available at a PE multiple of 14.4x on NTM basis as compared to the industry median 13.96x. The stock is trading towards its 52-week high of A$5.270. Also, the company would release its 1HFY20 results on 18th February 2019, a key event to gauze the performance of the business. Considering the valuation, current trading levels and other aforesaid facts, we have a wait and watch stance on the stock at the current market price of A$4.910 per share, up 1.029% on 6th December 2019.

FBU Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...