.jpg)

Stocks’ Details

BHP Group Limited

Completion of Minerva Gas Plant Acquisition: BHP Group Limited (ASX: BHP) is engaged in minerals and hydrocarbon exploration, production and processing. As on 14 January 2020, the market capitalization of the company stood at $116.45 billion. The company has recently announced that Terry Bowen has been appointed to the Board of Transurban Group with effect from 1 February 2020 and as a Chair of BHP’s Risk and Audit Committee from 1 May 2020. Cooper Energy has recently acquired Minerva Gas Plant from the Minerva Joint Venture participants where BHP Petroleum has 90% interest and Cooper Energy has interest of 10%.

In the recently held AGM, the top management stated that the company delivered strong financial performance with EBITDA of US$23 billion at a margin of 53%. For the quarter ended 30 September 2019, copper production of the group decreased by 3% due to planned maintenance across several operations and natural field decline in Petroleum.

.png)

Operational performance (Source: Company Reports)

What to Expect from BHP: The company remains positive for its long-term outlook and is confident that the portfolio is well positioned to capture the opportunities from population growth and better living standards. The company along with solid set of development options across a range of commodities with attractive fundamentals is expected to deliver returns in the upcoming year.

Valuation Methodology: EV/EBITDA Based Approach

.png)

EV/EBITDA based Approach (Source: Thomson Reuters), *1 USD=1.45 AUD

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of gave a return of 1.49% on the YTD basis and a return of 8.21% in the past 3 months. During FY19, net margin of the company stood at 21.5%, higher than the industry median of 10.9%. This indicates that the company is managing its costs well and is able to convert its revenue into profits. In the same span, ROE of the company was 16.8% as compared to the industry median of 12%. Considering the returns, high net margin and ROE and positive long-term outlook, we have valued the stock using EV/EBITDA based valuation approach and have arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $40.050, up by 1.315% on January 14, 2020.

Resolute Mining Limited

Response to Media Speculation of Gold Mine Sale: Resolute Mining Limited (ASX: RSG) is engaged in gold mining and development of resource projects and prospecting and exploration for minerals. The company in response to media speculation of gold mine sale stated that it is reviewing the Ravenswood Gold Mine and is evaluating the future capital demands of the project. The company also stated that it has entered negotiations with EMR Capital Management Limited on transaction for total proceeds of up to A$300 million comprising A$100 million of initial upfront value and up to A$200 million in additonal deferred consideration.

Despite the Syama roaster being offline, gold production of the company increased by 2,092oz to 105,293oz in December 2019. For the same period, Mako produced 42,997oz of gold. For the quarter ended 30 September 2019, the company made gold sales of 127,265oz at an average gold price of US$1,362/oz.

.png)

September 2019 Quarter Production and Costs (Source: Company Reports)

What to Expect: The company has recently provided an improved production and cost guidance for the 12 months to 31 December 2020. The company expects gold production of around 500,000oz at an All-In Sustaining Cost forecast of US$980/oz. It also expects non-sustaining capital expenditure for operating assets to be approximately US$15 million with investment of US$25 million on exploration and other development capital expenditure.

Valuation Methodology: EV/EBITDA based Approach

.png)

EV/EBITDA based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of RSG is inclined towards its 52-weeks’ low level of $0.965 and is offering a decent opportunity for accumulation. For the 1H19 net margin of the company stood at 12%, higher than the industry median of 10.6%. This indicates that the company is managing its costs well and is able to convert its revenue into profits. Considering the trading levels, higher net margin and improved guidance, we valued the stock using EV/EBITDA based multiple approach and have arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $1.170, up by 4% on January 14, 2020, owing to its response for gold mine sale.

Stanmore Coal Limited

Strong Quarter of Coal Mining: Stanmore Coal Limited (ASX: SMR) is engaged in the exploration, development, production and sale of metallurgical and thermal coal. As on 14 January 2020, the market capitalization of the company stood at $274.06 million. The company has recently released its December quarter report wherein it reported quarterly sales of 497kt, down by 31% on the September quarter. This was mainly due to co-shipper coal availability delays resulting in vessels for loading at DBCT slipping into January. For the same time span, net cash position declined to $57.9 million from $90.7 million. The company reported a strong quarter of coal mining with 864kt ROM mined.

.png)

Production and Sales (Source: Company Reports)

Growth Opportunities: The company has revised its EBITDA guidance and expects it to be in between $50 million to $52 million. It also gave the FOB costs (excluding royalty) guidance and anticipates it to be around A$107/tonne product coal sold. The company is expected to release its interim report in late February.

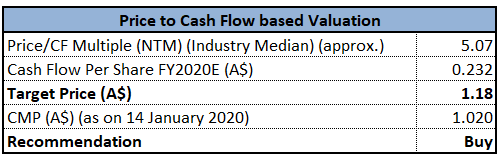

Valuation Methodology: Price/Cash Flow Based Approach

Price/Cash Flow Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of SMR gave a return of 1.9% in the past one month and is trading close to its 52-weeks’ low level of $0.905. In the span of 3 years from FY16 to FY19, the company witnessed a CAGR of over 200% in revenue. During FY19, net margin of the company stood at 22.7%, higher than the industry media of 15.3%. In the same time span, ROE of the company was 79.6% as compared to the industry median of 13.2%. Considering the trading levels, CAGR in revenue and high ROE, we valued the stock using Price/Cash Flow based relative approach and arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $1.020, down by 4.673% on January 14, 2020, owing to recent release of its quarterly results.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...