Pacific Smiles Group Limited

.png)

PSQ Details

FY20 Outlook: Pacific Smiles Group Limited (ASX: PSQ) provides services and facilities to dental practitioners who practice at dental centres operated by Pacific Smiles. As on 30 June 2020, the market capitalisation of the company stood at ~$245.62 million. The company had earlier stated itsre-opening of the bulk of its 93 dental centres. The re-openings were in response to the expanding range of dental procedures allowed by the Australian Health Protection Principal Committee (AHPPC), following the ease during the Covid-19 related restrictions. In lieu of this, PSQ provided an outlook for FY20. It expects patient fees for the period to be ~$185.8m, down 0.7% year over year, with same centre patient fee decline of ~4.5%. Further PSQ expects underlying EBITDA to be between $22.3m to $22.8m whereas net debt is expected to be around ~$8.5 million. The company is set to report its FY20 results on 20th August 2020.

Interim Results: During 1H20, the company reported increased patient fees by 14.5% to $105.4 million and growth of 9.4% in the same centres. In the same time span, Underlying EBITDA of the company went up by 15% to $12.9 million and NPAT saw a rise of 11.2% to $5.0 million.

.png)

1H20 Financial and Operational Highlights (Source: Company Reports)

Future Expectation: The company is taking necessary measures to open news centres in the coming years, which will eventually contribute to long-term growth and profit margins of the company. Further, the company expects to achieve a long-term target to open around 250 centres having more than 5% of total market share. The company’s long-term strategies involve network growth via existing centres, extending the range of services and opening hours along with high functional leadership.

Key Risks: The company is exposed to various risks such as interest rate risk, credit risk, and liquidity risk.Further, pricing pressure in the competitive Australian market remains a headwind. Additionally, a debt-laden balance sheet adds to its woes.

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

.png)

Price to Cash Flow Multiple Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of PSQ gave a return of 8.11% in the last one month and is inclined towards its 52-weeks’ high level of $2.05. During 1H20, gross margin of the company was 83.4%, higher than the industry median of 57%. In the same time span, net margin of the company was 6% as compared to the industry median of 3%. Considering the returns, trading levels, decent financial position midst pandemic, we have valued the stock using price to cash flow multiple based illustrative relative valuation approach and have arrived at a target upside of higher single-digit (in percentage terms). We have taken the peer group - Opthea Ltd (ASX: OPT), AFT Pharmaceuticals Ltd (ASX: AFP) and Capitol Health Ltd (ASX: CAJ). Hence, we recommend a ‘Hold’ rating on the stock at the current market price of $1.57, down by 1.875% on 30 June 2020.

.png)

PSQ Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Collins Foods Limited

.png)

CKF Details

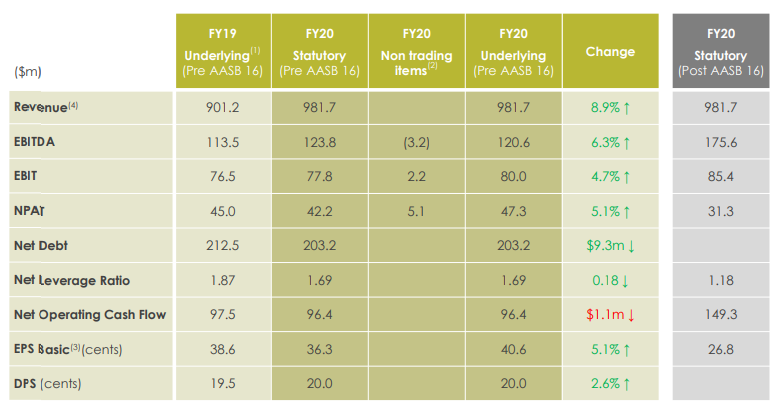

Revenues up 8.9% Year Over Year in FY20: Collins Foods Limited (ASX: CKF) is mainly involved in the operation, management, and administration of restaurants in Australia, Europe, and Asia. The market capitalisation of the company stood at ~$974.62 million as on 30 June 2020. In a recent update, the company stated that Vinva Investment Management, has ceased to become a substantial holder of the company, effective from 26 June 2020.

FY20 Key Highlights: On the financial front, the company experienced a growth of 8.9% in revenue, which amounted to $981.7 million in FY20. It experienced a decline in net debt to $203.2 million in FY20 as compared to $212.5 million reported at the end of FY19. Underlying EBITDA for the period went up 6.3% to $120.6 million. The decent financial performance of the company resulted in the EPS to increase to 40.6 cps from 38.6 cps in pcp. The company declared a 100% franked final dividend of 10.5 cents per ordinary share, demonstrating the healthy operating cash flows of the business and its growth outlook.

Key Highlights (Source: Company Reports)

Business Model Remains Strong Amid COVID-19:The company recently provided an update relating to the COVID-19 led global impact on its business. The company has taken necessary measures to ensure the well-being of its employees and customers as well as implementing cost control measures and ensuring continuity of the business. The KFC Australia business has shown improvements in sales amid COVID-19 led crisis. In FY20, same store sales (SSS) in Australia were up 3.5% year over year. The company opened 9 new restaurants, with home delivery available in 137 restaurants through Deliveroo and Menulog. The company had a positive come back in the Taco Bell business in FY20. The company opines that it is well-positioned to stay afloat through this difficult time. The company’s overall business model remained resilient through COVID-19 challenges.

Key Risks: In Europe, the company’s business was impacted by COVID-19 led crisis. Same Store Sales (SSS) in Europe declined 5.8% year over year in FY20. Further, the company is exposed to various kinds of risks such as failure to meet the requirement of food products safety, supply chain disruption, changing consumer behaviours, stiff competition, and inability to adapt to changing environments.

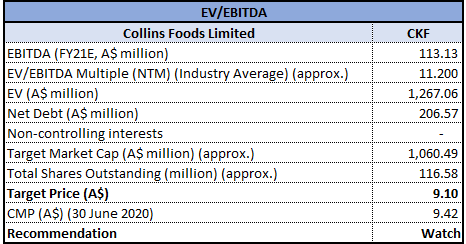

Valuation Methodology:EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company corrected 7.52% in the past six months and is currently trading close to its 52-week high of $10.8. The stock has a P/E ratio of 25.91x and an annual dividend yield of 1.91%. The company is focused on further strengthening all operational systems as well as executing on initiatives, which continue to improve the customer experience while maintaining operational excellence. We have valued the stock using an EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a correction of single-digit (in percentage terms). Therefore, considering the above factors and current trading levels, we have a watch stance on the stock at the current market price of $9.42, up by 12.679% on 30 June 2020 on the back of recent FY20 results.

.png)

CKF Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...