James Hardie Industries Plc

33% growth in the group adjusted net operating profit in 3Q FY 18: James Hardie Industries Plc (ASX: JHX) stock rose 6.7% on February 2nd, 2018 after the company reported 33% growth in the group adjusted net operating profit to US$69.9 million in the third quarter of FY 18. The growth is due to the higher prices for its products and modest volume growth. The group net sales grew 9% to US$495.1 million in the third quarter of FY 18. Moreover, JHX expects its North America Fiber Cement segment’s FY18 EBIT margin to be in the range of 20% to 25%. The full year adjusted net operating profit has been forecasted to be between US$260 million and US$275 million. Additionally, JHX expects to close the Fermacell acquisition in the fourth quarter of FY 18. Meanwhile, JHX stock has risen 13.47% in three months as on February 01, 2018 and is trading at a high level. The company is reducing the manufacturing inefficiencies and production costs and is experiencing higher input costs. Despite the result, the stock looks “Expensive” at the current price of $23.65

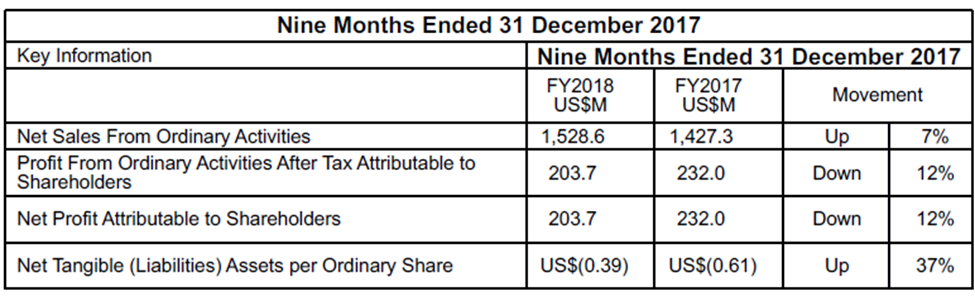

Performance for Nine Months ended 31st December 2017 (Source: Company Reports)

Wesfarmers Ltd

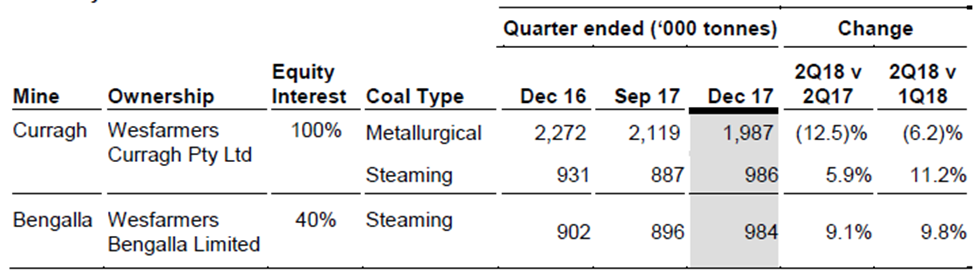

December Quarter Production, Development and Exploration: Wesfarmers Ltd (ASX: WES) has stated that for December quarter, the overburden removal was 14.6% below the previous quarter in Curragh, due to the mining sequence and high overburden removal volumes posted in the previous quarter. The coal production for the December quarter was 2,973,000 tonnes, which is in line with the previous quarter. Metallurgical coal production fell 6.2% to 1,987,000 tonnes below the previous quarter and the Steaming coal production increased 11.2% to 986,000 tonnes higher than the previous quarter. Moreover, for December quarter in Bengalla, WES’s share of coal production increased 9.8% above the previous quarter to 984,000 tonnes as the mine progressed through a more productive area of the mining sequence. In the December quarter, there were no significant development and exploration activities at both the mines.

On the other hand, Coles seems to be losing the fizz and the market expects that a shift in the strategy might be required for it to regain the lost ground. The supermarket is losing its share to Woolworths in terms of factors including in-store execution and strategy. Coles might be needed to focus on quality and customer requirements. In the last one month, WES has not made any significant stock price movement given the challenges. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $44.15

Quarterly Production (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...