Metcash Limited

.png)

MTS Details

Cost Cutting Initiatives to Aid MTS in Long-term: Metcash Limited (ASX: MTS) is a wholesaler to independent retailers in the food, grocery, liquor, hardware & automotive industries. The market capitalisation of the company stood at $2.91Bn as on 23 March 2020. In a recent update, the company stated that National Australia Bank Limited and its associated entities have become a substantial holder of the company, with a voting power of 5.208%. In another update, the company announced that Brad Soller has showed his intention to step down from the post of Group Chief Financial Officer in the company. Mr Soller has agreed to continue with his roles and responsibilities in the company till the selection of a successor, which is expected to be done by FY21 end.

H1FY20 Financial Highlights for Period ended 31 October 2019: During the period, the company’s total revenue (statutory) increased 1.6% year over year and stood at $6,289.8 million. The rise in revenue was on the back of higher sales growth in the Food and Liquor pillars, offsetting the decline in Hardware sales. Underlying EBIT stood at $149.7 million, representing a decline of 5.3%, primarily due to reduced contribution in the Food pillar from the resolution of onerous lease obligations. Underlying profit after tax came decreased from $100.3 million in 1HFY19 to $95.7 million. The company paid an interim dividend of 6 cents per share during the period. Food, liquor and Hardware contributed 61%, 25% and 14% of sales revenue, respectively. Operating cash inflow for the period stood at $88.8 million, with cash realisation ratio of 52.4%.

.png)

1HFY20 Financial Highlights (Source: Company Reports)

What to Expect: Metcash expects construction activity to be supported by population growth as well as undersupply of housing. Under the Food segment, the company further anticipates cost cutting initiatives to help offset the cost inflation impact over the remainder of FY20. In the liquor segment, the company expects the market in the remainder of FY20 to get affected by the ‘premiumisation’ trend.

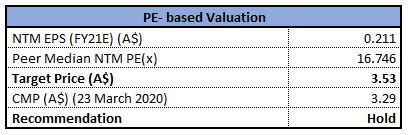

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company is currently trading at its 52-week high level of $3.29. In 1HFY20, current ratio and quick ratio of the company stood at 1.11x and 0.69x as compared to the industry median of 0.66x and 0.23x, respectively. This reflects that the company is in a decent position to address its short-term obligations against the broader industry. We have valued the stock using the P/E based relative valuation method and arrived at a target price with an upside of single-digit (in percentage terms). For the purpose, we have taken peers such as Graincorp Ltd (ASX: GNC), Coca-Cola Amatil Ltd (ASX: CCL), Treasury Wine Estates Ltd (ASX: TWE), to name few. Considering the decent liquidity position and current trading levels, we give a “Hold” recommendation on the stock at the current market price of $3.29 per share, up 2.812% on 23 March 2020.

MTS Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...