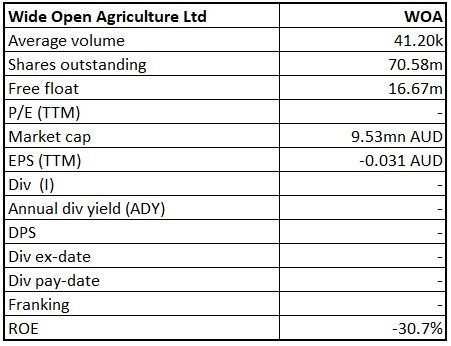

Wide Open Agriculture Ltd

WOA Details

Final Market Testing for Western Australian Oat Milk: Wide Open Agriculture Ltd (ASX: WOA) is engaged in the development of the farmland portfolio and food brand. The company has recently opened its online sales portal for direct sales of grass-fed, regenerative beef and lamb to the consumer. As on 2 April 2020, the market capitalization of the company stood at $9.53 million. The company has announced that it has completed an industrial trial of 5,000L to produce regenerative oat milk. The company projects that consumer intolerance to dairy, environmental concerns and potential health benefits of plant-based products will drive the worth of the oat milk to ~US$1.6 billion in 2024. WOA is currently conducting the final test and is focusing on the taste, color and texture of the product.

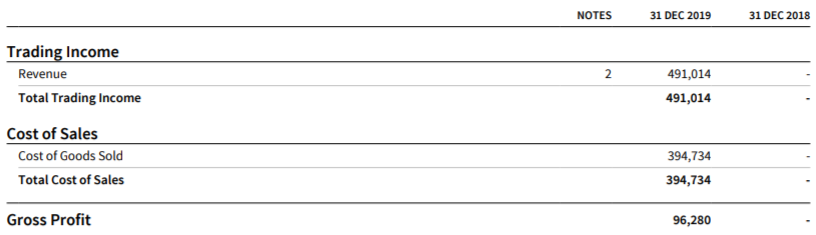

Growth of 46% in Quarterly Revenue: WOA delivered quarter on quarter revenue growth, with Q2 revenue increasing by 46% to $290k. These results are the highest in the company’s history, bringing the total sales for H120 to $490k and reported a gross profit of $96.2k. In the same time span, it reported a growth of 64% in restaurant customers sales with over 50 regular customers from premium restaurants and food service outlets. The company has also launched its flagship regenerative food brand, Dirty Clean Food in more than ten retail locations and is focusing on building long-term relationships with retailers.

1H20 Financial Highlights (Source: Company Reports)

Future Expectations and Growth Opportunities: Over the second quarter, Wide Open Agriculture Ltd has established multiple sales channels that present an ideal pathway to enter new markets in Australia and South-East Asia. The company has also stated that the outbreak of COVID-19 has not significantly impacted the business operations, and WOA is experiencing continued sales push. It stated that monthly online sales orders have witnessed an increase from 51 in February to 388 in March 2020 and hence expects Q3 FY2020 revenue to exceed Q2 FY2020.

Food service orders from restaurants and cafes have witnessed a fall, but the decline is likely to be compensated by the growth in the retail and online sales channels. This positions the company for sustained sales. The company is aiming at improving its operational efficiencies, diversifying product lines and growing distribution channels. WOA is also looking at initiatives that will enable increased sales and marketing activity in WA and other states, domestically.

Stock Recommendation: As per ASX, the stock of WOA gave a negative return of 25% in the past one year but a positive return of 12.5% in the last one month. The stock is inclined towards its 52-weeks’ high level of $0.190. During 1H20, Debt/Equity ratio of the company stood at 0.39x, higher than the industry median of 0.19x. In the same time span, EBITDA and net margin of the company witnessed a substantial improvement over the corresponding period in last year. On TTM basis, the stock is trading at a price to book value multiple of 2.5x, lower than the industry median (Consumer Non-Cyclicals) 1.3x. Considering the volatility in stock price, lower trading volumes and current trading levels, higher price to book value multiple, decent growth in revenue despite softer market conditions and modest outlook, we have a watch stance on the stock at the current market price of $0.135, on 2 April 2020.

WOA Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...