Qantas Airways Ltd (ASX: QAN) has been a key stock in the industrial sector with ability to position itself for growth and sustainable returns. It has been on track for returning over $2.6 billion to shareholders since October 2015. Lately, the group’s Chairman Leigh Clifford indicated to step down from the national carrier in October 2018 and this will break his 11 years’ association with the group. Meanwhile, Richard Goyder will assume the role. The group also intends to depict key insights on operations during its AGM on 26 October.

The group has witnessed key transformative periods with profitability settling in alongside investors’ returns. It has been also targeting ongoing transformation gross benefits of $400 million per annum. The whole landscape of operations has made Qantas an iconic Australian company among key performing airline groups. The group seems to have dodged the view that airlines will lead to loss of money only and can’t be a long-term investment play. The key thing to look at is the funding of new aircrafts to stay up to beat and more competitive. However, cost becomes a key aspect to look at. In case of Qantas, the cash flows look in a decent shape given the oil price scenario over the last few years, while the recent changes in prices need to be considered along with cash tax payments that have been slated for FY19 and onwards. However, the benefits in terms of domestic revenue may help the stock. Then, replacing old planes with new ones can be an important move from future perspective. The group lately ordered 6 additional 787-9 Dreamliners for delivery by the end of 2020.

If one looks at the third quarter FY18 trading update, the total revenue has been up 7.5% to $4.25 billion with healthy unit revenue performance in both the domestic and international markets. Despite the rising fuel cost seen lately, the group’s full year underlying profit before tax has been flagged to be in the range of $1.55 billion to 1.60 billion. The group had recently cancelled buy-back of shares while as at May 2018, the programme was 50% complete.

The group’s Return on Invested Capital has been above >20% (12 months to 31 Dec 2017) while its segments have yielded ROIC over 10%. Qantas Loyalty programme is also targeting 7-10% CAGR in earnings through FY22. QAN stock moved up 33% this year to date given the developments. We believe that the stock has a long-term potential and maintain a “Buy” at the current price of $ 6.720.

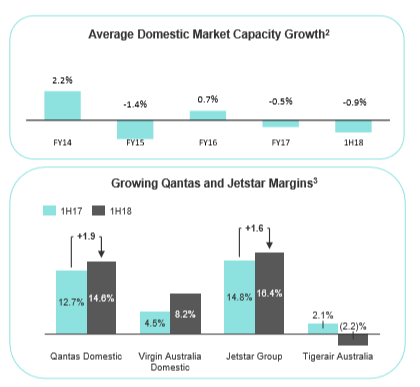

Domestic Market Statistics (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...