Analysis

Transpacific Industries Group Ltd (ASX: TPI) said that Vik Bansal would be the new CEO of the firm, substituting Bob Boucher who has served for only eighteen months. With the stock trading near its multi-year lows, it is quite challenging for Vik Bansal to take the stock ahead. However, we believe that TPI’s stock has the capabilities of driving higher given its market leadership.

Market Leader in Waste management

-

Transpacific is the market leader in Waste management wherein 66% is represented by Cleanaway and 34% by Industrials business. Even though Australia’s waste management industry is highly fragmented, Transpacific has higher market penetration against its competitors. On an overall perspective, Transpacific has the capability of controlling prices as it has large landfill assets.

Sales intiatives in future (Source - Company Reports)

Sales intiatives in future (Source - Company Reports)

-

TPI has been taking several initiatives to maintain its dominant position, and also achieve cost optimization to improve its financial performance. The group has addressed operational issues relating to pricing and control as well as focused on improving its management during fiscal year of 2014. In the current fiscal year, the group has been investing to improve its capabilities, infrastructure and operational process. Consequently, management expects that these efforts would drive its core C&I business as well as pricing. Moreover, the target industry of Transpacific is expected to grow at a compound annual rate of 4.41% to 2020-2021 years, which is much higher as compared to the GDP growth of Australia for the same period.

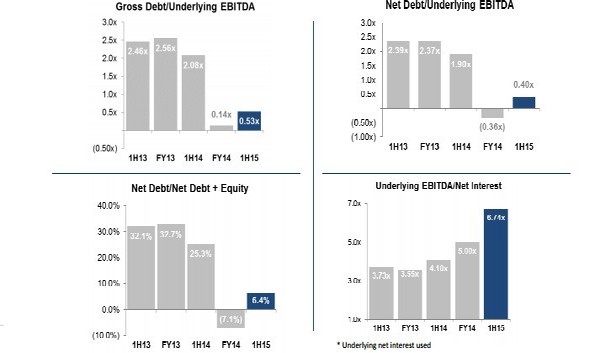

Net Debt + Gross Debt Position (Source - Company Reports)

-

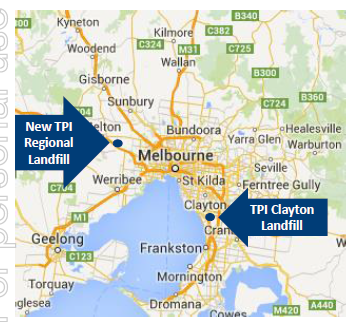

Transpacific had also made a strategic acquisition of Melbourne Regional Landfill in Ravenhall, west Melbourne, to hone its (TPI) Cleanway business. The group took over landfill operations from its earlier operator Boral during February. The Melbourne Regional Landfill have long term assets wherein the airspace is available for around fifty years with permitting or seven to ten years. The group will be diverting most of its Melbourne’s post collection volumes to regional landfill. Accordingly, TPI expects to enhance its Melbourne’s internalization to over 65% by fiscal year 2017, from over the present rate of 25%.

Melbourne Regional Landfill (Source - Company Reports)

Financial Performance Highlights

-

TPI posted disappointing first half of 2015 results, with statutory loss after tax attributable to ordinary equity holders falling to $41.7 million during the period, as compared to $158.6 million profit in 1H14. This huge decrease was mainly due to the underlying costs associated to the impairment of assets ($77.5 million), fleet grounding costs ($16.5 million) which were offset by modest gains from disposal of New Zealand businesses ($9.0 million) and net proceeds from disposal of investments ($1.9 million).

TPI Daily Chart (Source - Thomson Reuters)

TPI Daily Chart (Source - Thomson Reuters)

-

The Cleanway segment’s revenues, decreased 2.4% yoy to $456.3 million in 1H15, but increased by 2.7%, as compared to the previous half. However, the group’s pilot sales project for commercial and industrial segment was successful, and therefore TPI is launching the new sales program across major markets for the next half. The collection system prices have also improved driven by the better prices as compared to last fiscal year. On the other hand, TPI’s Industrials segment revenues plunged 7.2% yoy to $229.1 million, affected by challenging market conditions and falling oil prices. Therefore, Transpacific undertook business restructuring in this segment due to poor trading conditions which were partly affected by the studying a fee based structure for oil collection, consolidating processing facilities and re-scaling the business. Meanwhile, the group’s EBITDA reached $121.8 million, which is a decrease of 12.7% (excluding discontinued operations) as compared to earlier year’s corresponding period.

TPI Dividends (Source - Company Reports)

TPI Dividends (Source - Company Reports)

-

On the other hand TPI has been maintaining a strong balance sheet, wherein the ratio of cash flow from operating activities to underlying EBITDA improved to 95.4% as compared to pcp of 78.1%. The group expects to incur Remediation costs of over $26 million for the entire FY15 on landfills, while the capital expenditure will be over $170 million in FY15.

Outlook

-

Transpacificstock has been under pressure from quite some time now and delivered a decrease of around 26% over the last six months. The shares have fallen over 9.5% in last four weeks alone partly impacted by investors negative sentiment as the group’s CEO resigned after serving just 18 months. However, investors should note that TPI is heavily investing on infrastructure and is upping sales initiativesto deliver solid potential growth. As a result, TPI forecasts to incur a one-off costs of over $14 million in the second half, including the earnings from the Melbourne Regional landfill business acquisition. The company is also executing policies to improve its fleet maintenance and road safety further.

-

Moreover, if Vik Bansal continue to focus on cost optimizations, service efficiency, growing landfill capacity, and divesting non-core assets, the shares of TPI would grow higher from these levels. Therefore, we believe that investors need to leverage the current lower levels and enter into the stock. Accordingly, we recommend a “BUY” on TPI at current price of $0.685.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...