Cochlear Limited

Strong Growth by Services Business:Cochlear Limited (ASX: COH) is a global leader in implantable hearing solutions. Its offerings include cochlear implants, acoustic implants and bone conduction implants.

Shareholding Updates: The company recently updated that Hyperion Asset Management Limited became a substantial shareholder of the company with the voting power of 5.04%.

FDA Approval: The company recently received FDA approval for the Nucleus® ProfileTM Plus Series cochlear implant and is planning to launch the same in the US immediately. The implant has been designed for routine 1.5 and 3 Tesla magnetic resonance imaging scans without the need to remove the internal magnet. Its commercial availability commenced in Germany with other European countries.

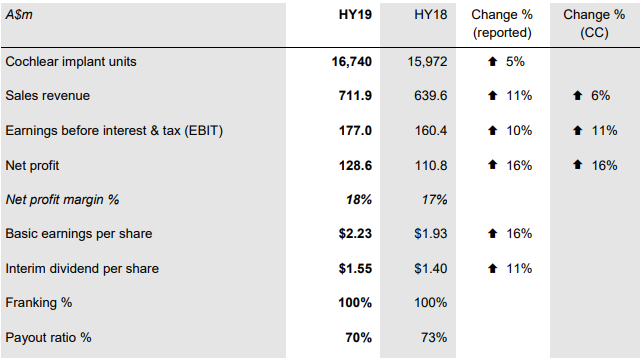

Financial Results: During the six months ended 31 December 2018, the company generated sales revenue amounting to $711.9 million, up 11% on prior corresponding period revenue of $639.6 million. Cochlear implant units for the period stood at 16,740, up 5% on the prior corresponding period. Reported net profit stood at $128.6 million, up 16% on the prior corresponding period net profit of $110.8 million.

Key Metrics (Source: Company Reports)

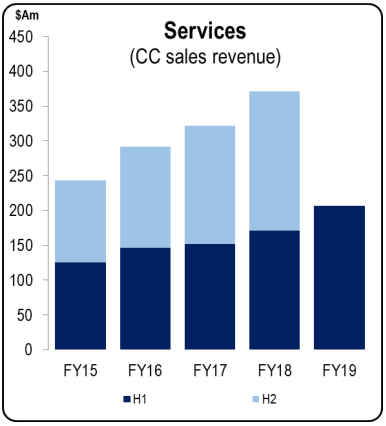

Services Business Highlights: Revenue for the services business reported an increase of 28% on prior corresponding period.On a constant currency basis, revenue increased by 21%. The continuous growth of the services business is supported by the growth of recipient base, which represents almost 30% of the sales revenue. Nucleus®7 Sound Processor, the world’s first Made for iPhone cochlear implant sound processor, has gained a lot of popularity among the recipients. The product was launched in October 2017, with the release of Nucleus Smart App for AndroidTM in June 2018.

Services Sales Revenue (Source: Company Reports)

Implant Business Highlights: Revenue for the implant business reported an increase of 5%, with unit growth of 5%. The company’s developed markets delivered units in line with the units delivered in the prior corresponding period. Prior to that, the implant business had delivered eight halves of strong growth owing to share gains from new products and market growth. Japan witnessed strong demand with respect to the implant business on the back of the expansion of indications and funding for cochlear implants in late 2017. There was a lower rate of growth in the United States due to a loss of share on account of competitor product launch. Increased competitor activity and health budget constraints in a few markets impacted the growth in Western Europe.

Cochlear Implant Sales Revenue (Source: Company Reports)

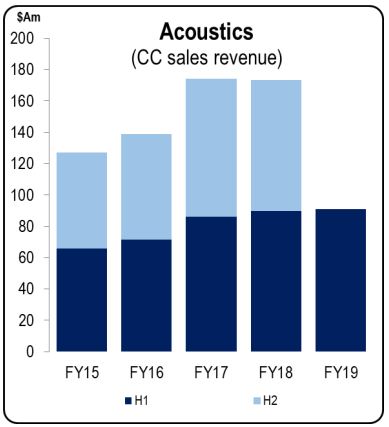

Acoustics Business: Revenue for the acoustic business witnessed an increase of 7%on the prior corresponding period with continued demand for Baha 5 sound processor range. Revenue for the segment increased by 1% on a constant currency basis.

Acoustics Sales Revenue (Source: Company Reports)

Contingent Liability: Under the patent dispute with Alfred E.Mann Foundation for Scientific Research and Advanced Bionics LLC, the US District Court had awarded damages of US$268 million against the company, in November 2018. The exact amount of the damages to be paid has not been ascertained yet, following which the company provided for provision with respect to damages held at 30 June 2018, amounting to $21.3 million and disclosed as a contingent liability. As at 31 December 2018, the provision stood at $19.6 million.

Outlook: The company expects to deliver a net profit in the range of $265 million and $275 million in FY19, depicting growth between 8-12% on FY18. The company aims to make significant investments in product development and market growth initiatives, that will deliver further growth in revenue and earnings. Over the next few years, the company expects its capital expenditure to rise in the range of $80 million - $100 million per annum, due to large long-term investment projects. The company is targeting a dividend payout ratio of around 70% of the net profit.

Stock Recommendation: The stock of the company generated returns of 5.36% and 3.23% over a period of 3 months and 6 months, respectively and 16.28% on YTD basis. The stock is currently priced towards 52 weeks high level of $226.710 and has a price earnings ratio of 44.430x. The company expects FY19 revenue growth to be driven by the Services business. Cochlear implant is expected to report a lower rate of growth for the year. The company targets to maintain the net profit margin by retaining its market leadership through continued investments. As suggested by the outlook, the company’s capital expenditure is expected to rise in the coming years on the back of large long-term investment projects. In addition, there might be inherent uncertainties regarding the damages to be paid by the company related to the patent dispute with AMF and AB. Hence, considering the aforesaid factors along with the price movement on YTD basis, we are of the view that most of the factors are priced in at the current level. Hence, we give an “Expensive” recommendation on the stock at the current market price of $201.520, down 0.91% on 15 August 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...