-

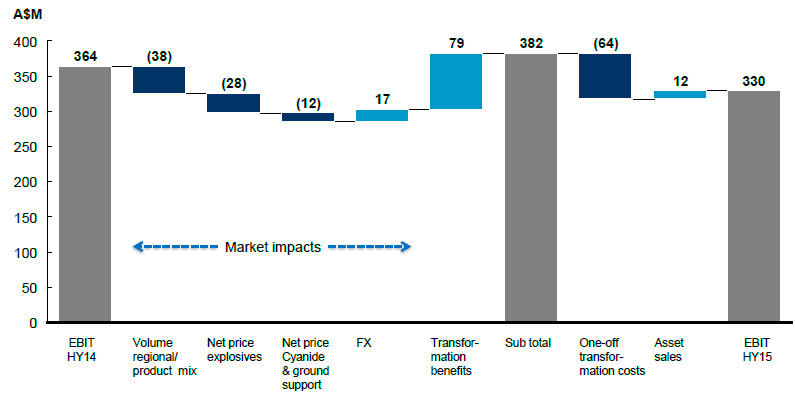

Poor first half of 2015 results: Orica Ltd (ASX: ORI) disappointed investors by reporting a very poor first half of FY2015 performance (ended on March 2015). The firm’s overall revenues fell to $3.28 billion during the first half of 2015, as compared to $3.44 billion in the September half of 2014 and $3.36 billion in the first half of 2014. Pressure from Australia/pacific regions as well as decrease in chemicals business (with the sale completing on February 2015) led to the revenue decline. ORI EBITDA fell by 5% on a yoy basis to $472 million, while the EBIT declined 9% yoy to $330 million. Orica reported a net profit after tax decline of 3% yoy to $211 million in 1H15. The Net operating and investing cash flow fell to $109.5 million in 1H15, against $124.4 million in 1H14. Meanwhile, Orica maintained its interim dividend at 40 cents per share during the period. Orica reported that it would perform $400 million worth of share buyback which would be ongoing for the second half of the fiscal year as well.

EBIT performance during the period (Source: Company Reports)

-

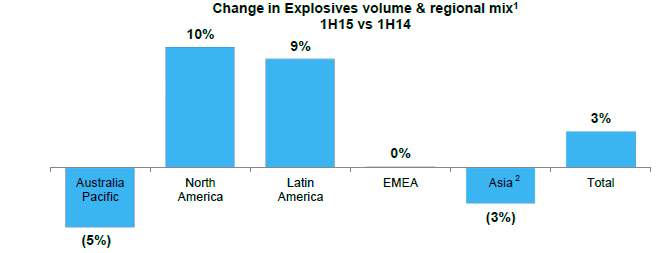

AN volumes continue to be under pressure: Orica’s overall Aluminum nitrate volumes (AN-which included other emulsion products) slightly increased by 3% on a year over year basis, impacted by the tough market conditions. Australian explosives volumes fell 5% yoy on the back of customer site closures as well as mine planning changes occurred in Eastern Australia. Moreover cost cutting measures by Orica’s clients at iron ore sites in the Pilbara added to the volumes pressure. On the other hand, AN volume growth rose for North America by 10% yoy, adding some support to the overall volumes, as the region witnessed more sales from existing clients. Improved indirect sales as well as contract wins also added to the North America’s volume growth. Latin America volumes surged 9% yoy during the period, driven by advanced blasting products and services revenue from projects in Brazil and Peru which improved 17% yoy. Meanwhile, the group’s advanced blasting products and services revenues increased 9% yoy driven by the contract wins in Brazil, Peru, Norway and CIS flowing during the period. With regards to the Europe, Middle East and Africa, earnings from operations marginally improved by 2% yoy driven by revenues generated from the advanced blasting products as well as services, despite pressure from explosives volumes and ground support volumes. But, Asia’s AN product volumes reduced 3% against pcp, impacted by inferior strip ratios and reduced demand from coal clients. However, ORL’s cyanide volumes improved by 28% yoy boosted by better demand, contract wins and customer destocking.

Performance of explosive volumes and regional mix for the first half of FY15 (Source: Company Reports)

-

Reducing exposure to the volatile markets: Orica has been making efforts to decrease its potential price exposure by winning new contracts from Australia/Pacific as well as global markets. Accordingly, its forward book of volumes is better this year as compared to the last year. Orica is implementing a partial production at its Yarwun operation as ammonium nitrate market is already oversupplied. Orica is also reviewing options to optimize its Bontang ammonium nitrate manufacturing facility in Indonesia for the medium and longer term. Meanwhile, the group has implemented a company-wide transformation program to improve its overall efficiency. As a result, the group finished a supply contract renegotiations with over 60% of its strategic supplier base. ORL decreased 550 operational support roles as a part of its manufacturing optimization efforts.

Orica Daily Chart (Source - ASX)

Orica Daily Chart (Source - ASX)

-

Weak Guidance: Orica estimates that its global explosives volumes would continue to be under pressure and forecasts to be around 3.75 million tonnes. Australian volumes for the rest of the fiscal half might be in line with the first half. Meanwhile, orica had reset its explosives prices which would show full impact to flow through the second half of fiscal 2015. Sodium cyanide volumes might surge by 10% for this fiscal year against earlier fiscal year. On the other hand, ground support markets are estimated to be under pressure, while the operating costs are expected to decrease due to costs incurred from ORL’s transformation program. Accordingly, the net pretax benefits are estimated to be in the range of $140 to $170 million while the implementation costs would be over $100 to $120 million in 2015.

-

Ongoing stock pressure: Orica Ltd(ASX:ORI) shares fell over 20.8% in last four weeks, as it expects a non-cash impairment charge in the range of $1.35 billion to $1.65 billion (after tax) during its 2015 full year financial results, due to challenging mining sector. Moreover, the group’s first half of 2015 results were not pleasing, and the management estimates the pressure to continue for the rest of the fiscal year as well. The groups AN volumes continue to face pressure as ammonium nitrate market is already oversupplied. In addition, cost cutting measures by its mining clients due to falling commodity prices would add more pressure on the stock. Accordingly, we recommend a “SELL” on the stock at the current price of $15.30

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...