NIB Holdings Limited

-

The company is the fifth largest private health insurer in Australia with an 8% market share and provides cover for more than 1 million people living in Australia and New Zealand. In addition to health insurance, the company also sells life and travel insurance, although these are not underwriting businesses. People in general are spending more and more money on health care and the relative funding contributions from governments cannot be indefinitely sustained. The inevitable consequence will be the private sector will have to play an increasing role despite the challenges that this will bring. There is also an accelerating emphasis on international cross-border healthcare and insurance coverage.

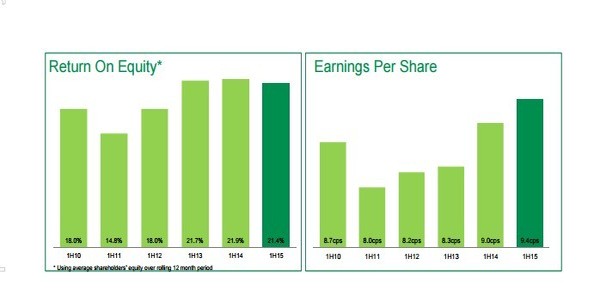

Return on Equity (Source - company Reports)

-

The main features of the company's business strategy is to grow its health insurance business for Australian residents in an organic manner at around 10% annual premium growth and 4.5% policy holder growth. This will be achieved through ongoing emphasis on the below 40s market (Virgin Green), growing the over 55 market share (Virgin Silver) and other tactical niches. Other strategies will include market share and earnings from international workers and students, developing the new business in New Zealand and ensuring that the design, payment and management of benefits meets the needs of policyholders.

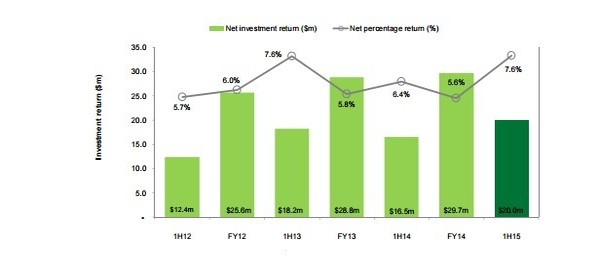

Net investment return (Source - Company Reports)

Net investment return (Source - Company Reports)

-

The results for first half 2015 showed a 9% growth in group premium revenues to $ 802.3 million and a 1.7% growth in group operating profit to $ 42.1 million. Australian residents health insurance operating profit rose by 10.3% to $ 37.5 million and the net margin was 5.3% compared to 5.2% in the previous year. International workers and students showed strong growth in the top line and the businesses accounted for 18.2% of operating profits while the Saudi International student business was secured. New Zealand is now growing after years of decline and with with policyholder growth of 3.3% compared to a decline of 0.3% in the previous year. The operating profit continues to be negatively impacted by ongoing upfront investment business growth and capabilities as well as the liability under the Premium Paypack product portfolio. The operating profit includes the expenditure incurred on developing options and other initiatives for new business. The investment return outperformed the internal benchmarks by 7.6% annualised largely due to the gains on the sale of investments in Pacific Smiles Group. NPAT grew 3.8% to $ 41.1 million, EPS by 4.4% to 9.4 cents per share and return on equity was steady at 21.4%. The interim dividend rose by 4.8% to 5.5 cents per share fully franked.

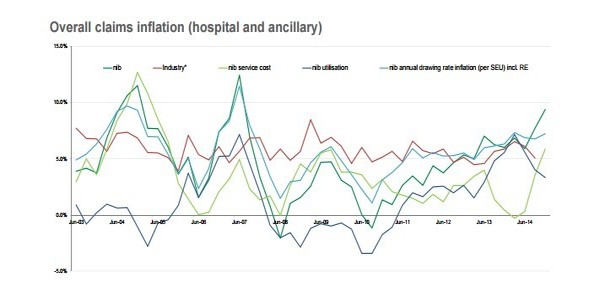

Claims Inflation (Source - Company Reports)

Claims Inflation (Source - Company Reports)

-

The Australian residents net policyholder growth was down because of increased competition and the rise of aggregators, the impact of regulatory changes (income testing and indexing of rebates from the Australian government), the after effect of high premium increases in 2014 and the closure of Top Extras 85% during the period. The unfavourable trends were partly offset by increased sales to over 55' s to account for 27.5% of total sales and reflects the performance of the distribution network. The lower use of retail brokers was a tactical decision because of the cost of acquisition. Premium revenue was up 8.8% with average premium income at $ 2436 compared to $ 2301 in the previous year. The underwriting margin was 5.3% compared to 5.2% and claims expenses were up 12.1% because of a 17% increase in hospital benefits and the 7.1% increase in ancillary benefits. Risk equalisation was down by 6.1% because of the success in the over 55 market and lower SEU growth. The price increase on 1 April 2015 is expected to absorb the ongoing inflation in forecast claims. MERC remains stable despite a 26% increase of $ 3.3 million in marketing investments divided between $ 1.2 million in DERC and $ 2.1 million in direct marketing.

-

Net operating cash flow was down by $ 9.7 million because of the timing of payments to suppliers, policyholders and employees. The company on average pays out claims of around $ 5 million every day. The net investing cash outflow was due to the reallocation of assets from cash to fixed income investments. The net cash outflow of $ 65.4 million is mainly because of the final dividend payment of $ 64.7 million which included a special dividend of $ 39.5 million. Gearing ratio as an 31 December 2014 defined as debt to debt plus equity was 17.1%. The continuing exploration of investment opportunities including mergers and acquisitions was the reason for the gearing ratio being below target. The targets are a long-term ratio of 30% and short to medium target of 25% with 5% being reserved for strategic opportunities. If the company takes advantage of a significant opportunity, the target may fall to below 30% for a short period of time.

-

The company is looking for steady growth in market and earnings for the core Australian residents health insurance business. It is also looking for growth in other existing businesses. Investment in innovation and business diversification as well as capital management will be conducted in a disciplined fashion. Annual system policyholder growth is expected to be around 2% to 3% with this company targeting growth in the range of 4% to 5%. Factors to be considered will be intense competition and churn but lifetime value remains ahead of cost of sales and retention. Underlying claims inflation will be in the region of 6% to 7% but premium pricing will be designed to cover inflation and to achieve net margin of around 5% to 5.5% in FY 2016. In addition, efforts will be made to control service cost inflation and mitigate avoidable surgery and treatment.

-

The guidance for FY 2015 is a consolidated operating profit in the range of $ 75 million to $ 82 million with the results likely to be at the lower end. The forecast for investment income will be in line with the relevant internal benchmarks and the ordinary dividend payout ratio will be 60% to 70% of the full year NPAT.

We believe that at the current price levels, the stock is overvalued and looks expensive .

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...