Australia and New Zealand Banking Group Ltd

.png)

ANZ Dividend Details

Outstanding dividend yield: Australia and New Zealand Banking Group Ltd (ASX: ANZ) delivered a Cash profit increase of 5% year on year (yoy) to $1.85 billion in the first quarter of 2016 as compared to the average of the third and fourth quarters of the fiscal year of 2015. The group’s core Australian and New Zealand business generated a decent performance driven by the lower interest and exchange rates coupled with improving Retail and Small Business segments. Retail business growth was boosted by the group’s market share gains at home lending in major markets. The group’s Asian business was slow while its China’s business was affected by manufacturing and trade-exposed sectors. But Institutional Markets income surged 6% yoy to $553 million while Institutional NIM was also enhanced during the period as the group’s efforts on asset mix and deposit pricing paid off. Some positive news comes from the new CEO who has updated about management restructure in order to improve productivity of the bank.

.png)

ANZ Portfolio (Source: Company Reports)

On the other hand, ANZ stock continued to be under pressure and fell over 11.24% (as of March 03, 2016), during this year to date impacted by the ongoing global markets turmoil. But, we believe that long term investors need to leverage this correction to enter the stock as it is trading at attractive valuations. ANZ has a low P/E and has an outstanding dividend yield. We reiterate our “BUY” recommendation on the stock at the current price of $24.80

ANZ Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.png)

NAB Dividend Details

Delivered core business performance: National Australia Bank Ltd. (ASX: NAB) stock continued to fall even during this year and generated a year to date decline of 12.95% (as of March 03, 2016), while fell over 30.63% in the last fifty two weeks impacted by ongoing global turmoil in the markets. But NAB was able to generate a top line growth of 2% first quarter of 2016, while reported a 4% growth without the legal settlement gain, driven by the better lending volumes net interest margin (NIM), and decent Wealth segment performance. NIM improvement shows that the group’s home loan repricing has paid off but was partly offset by the rising funding costs and competition. The bank was able to generate a decent top line growth despite the challenging conditions, driven by its solid core Australian business coupled with group’s efforts on customer experience and priority segments investments.

NAB’s charge for Bad and Doubtful Debts also plunged by 52% yoy to $84 million during the quarter driven by the enhanced asset quality and reported an Unaudited cash earnings for continuing operations (excluding CYBG impact) rise of around 3% to $1.7 billion during the December 2015 quarter, against the quarterly average of the September 2015 half year result and over 8% as compared to prior corresponding period. Meanwhile, the recent stock correction also opened an attractive opportunity to invest in NAB which is trading at lower P/E and has an outstanding dividend yield. Accordingly, we give a “BUY” on NAB at the current price of $26.37

.PNG)

NAB Daily Chart (Source: Thomson Reuters)

Commonwealth Bank of Australia

.png)

CBA Dividend Details

Improved bottom line performance: Commonwealth Bank of Australia (ASX: CBA) reported a cash NPAT growth by 4% yoy to $4,804 million for the half year ended on December 2015 while its statutory NPAT rose by 2% yoy to $4,618 million. CBA enhanced its Customer deposits by 9% to $500 billion, which is 64% of the funding. Operating income improved by 6% yoy to $12,362 million during the period while the bank is also boosting its capital position with Basel III Common Equity Tier 1 (CET1) (APRA) at 10.2% and CET1 (Internationally Comparable) APRA at 14.3%. But the bank’s risk weighted assets rose 11% yoy to $393 billion during the first half of 2016.

.png)

Commonwealth Bank of Australia CET1 performance (Source: Company Reports)

Despite delivering a decent half year performance, the bank’s requirements to comply with the APRA regulations coupled with the ability to maintain its performance in the coming periods given the current volatile conditions might continue to hurt the stock in the coming months.

The stock already corrected by 12.6% during this year to date (as of March 03, 2016). Hence, we issue an “Expensive” recommendation to CBA at the current price of $74.91

.PNG)

CBA Daily Chart (Source: Thomson Reuters)

Westpac Banking Corp

.png)

WBC Dividend Details

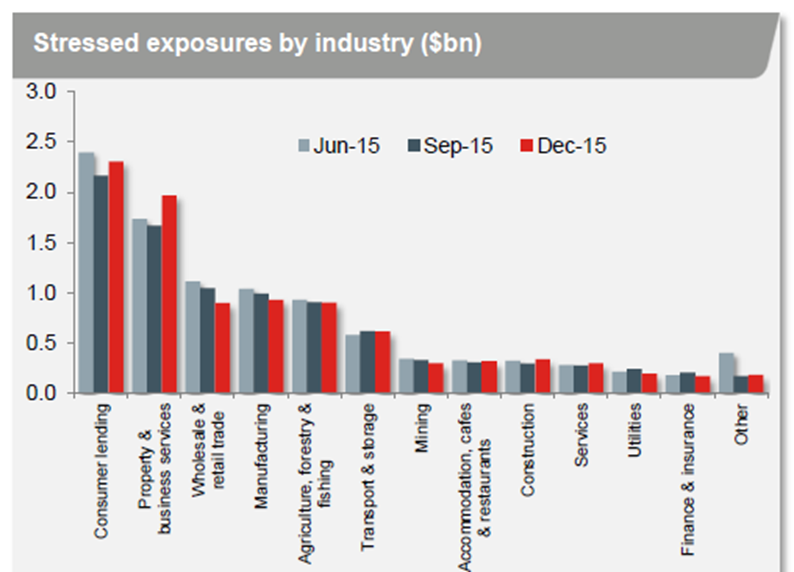

Boosting Capital position: Westpac Banking Corp (ASX: WBC) improved its stable funding ratio to 84.0% as of December 2015 driven by rise in customer deposits and capital. The bank even raised over $14 billion of term wholesale funding during this year and intends to enhance its liquidity coverage ratio (LCR) to 129% with $30 billion in excess liquidity by this year end. However, WBC’s total stressed assets in dollar terms have increased while the rising stress in consumer lending led to a 2 basis points rise in group mortgage.

WBC’s stressed exposure (Source: Company Reports)

The bank’s property and business services stress also increased due to a facility downgrade.

Moreover, the ongoing commodity prices decline also impacted the stress in the bank’s construction and services sectors. With the recent turmoil in the markets, we believe that the pressure for the bank’s stock might continue, which fell by over 7.21% in this year to date (as at March 02, 2016). Accordingly, we give an “Expensive” recommendation to the bank at the current price of $31.23

WBC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...