Eclipx Group Limited

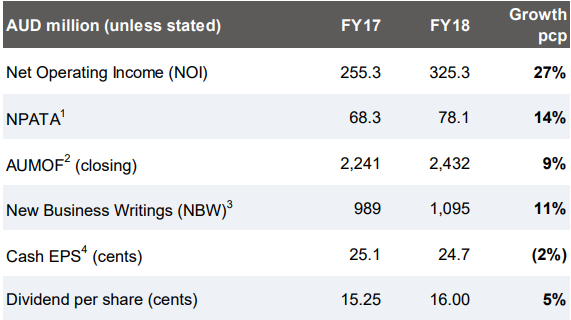

Financial Performance in FY18: Eclipx Group Limited (ASX: ECX), is a leading provider of fleet, equipment leasing and management, vehicle rentals and online auction services in Australia and New Zealand. Net Operating Income (or NOI) at $325.3 million witnessed a growth of 27% on account of strong growth in Fleet and commercial. Coming to the segment performance, Cash NPATA for the Australia Commercial segment for FY18 stood at $42.6 million as compared to $40.2 million in FY17 with 6% growth in new business writings. The Australia Consumer segment witnessed Cash NPATA of $16.5 million in FY18 as compared to $15.9 million in FY17. The Grays, acquired on 11 August 2017, recorded Cash NPATA of $10.4 million in FY18.

The New Zealand Commercial segment saw Cash NPATA at $8.6 million, lower than $11.0 million in FY17. Lower cash NPATA for this segment is largely attributed to $3.3 million related to the launch of Eclipx Commercial Finance in New Zealand. New business writings witnessed a growth of 13% as a result of the expansion in New Zealand and the retention of key fleet customers on sole supply agreements. To provide co-branded operating lease products to new vehicle sales outlets, New Zealand has continued to grow its strategic relationships. Eclipx maintains the committed funding facilities to cater for forecast business growth and as at 30 September 2018, it had undrawn debt facilities of $286.8 million.

Financial Highlights (Source: Company Reports)

NPTA Performance and Expectations: Management expects NPATA (Net Profit After Tax and Before Amortisation) for FY19, broadly in-line with reported NPATA for FY18 representing single digit growth in FY19 NPATA.

Estimates for a net profit before tax for FY19 are likely to witness increased growth compared to pro forma pre-tax numbers of FY18 due to the lower average corporate tax rate of 25% in FY18 as compared to the 29% estimated corporate tax rate for FY19. The NPATA results for the company have been slightly tilted towards the 2nd half in the past five years. NPATA for 1H FY19 is currently expected to be ~ 40% of the full FY19 NPATA on the back of softer Consumer and continued softness in Insolvency/Industrial auction market conditions prevailed in the 1Q FY 2019.

ECX has initiated for further cost reduction program, in response to the softer 1H FY19 performance as expected.The lower expense base being established in 2H FY 2019 would flow through to the lower annualised operating expenses beyond September 2019.

Stock Recommendation: At the current market price of $1.045, the stock is available at price to earnings multiple of 5.150x with market capitalization at ~$326.03 million and an annual dividend yield of 15.69%. Looking at the historical price performance, the stock has given a negative return of 68.42% in last 1-year whereas stock gained 36.91% in the last 1-month.

Considering the above factors along with decent fundamentals, and looking at recent run-up saw in the stock, we give a “Hold” recommendation on the stock at the current market price of $1.045 per share (up 2.451% 2 May 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...