Breville Group Ltd

BRG Details

· First Half 2017 Financial Performance: Breville Group Ltd (ASX: BRG) in the first half of FY 17 has reported 2.4% growth in the revenue to $339.2m, which is a growth of 5.6% on constant currency basis. The trend of EBIT growth rate acceleration continued, growing by 6.7% to $49.1m compared to 5.7% in the prior comparative period (pcp). The group EBIT margin improved to 14.5% in the first half of FY 17 from 13.9% in the pcp due to a greater proportion of higher margin Global Product segment revenue. The Global Product segment has reported strong performance with the double digit constant currency revenue growth of 12.9%. Moreover, the company has increased the dividend by 6.9% to 15.5 cents per share, in which 60% is franked. BRG has continued to make progress through its strategic transformation and the company’s key metrics are on track. Additionally, BRG has posted strong cash flow generation due to the improved operating performance and also due to a significant reduction in the working capital of the company.

.png)

1H 17 Group Financial Performance (source: Company Reports)

· BRG has changed its reporting segments in 1H 17: BRG has changed its reporting segments in the first half of FY 17 to reflect the two business models operating within the BRG Group, namely the “Global Product” business and the “Distribution” business and to show the way the company is being managed. The Global Product segment consists of the sale of Breville designed and developed products that are sold globally, either directly or through the third parties, and may be branded Breville, Sage or carry a third party brand. The ‘Distribution’ segment consists of products designed and developed by a third party. These products may be distributed after a license or distribution agreement, or they are sourced directly from manufacturers. These products may be branded Breville, Kambrook, or they may be distributed under a third party brand. The Distribution segment operates only in the ANZ region.

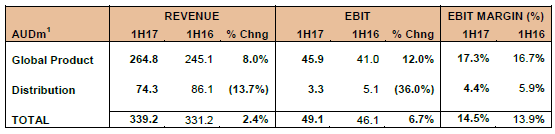

· Segment Performance in 1H 2017: In the first half of FY 17, the Global Product grew by 8.0% to $264.8m compared to the corresponding period last year. On constant currency basis, the revenue of this segment for the half year grew by 12.9%. Global Product segment EBIT for the half year has grown by 12.0% to $45.9m, and the EBIT margin improved to 17.3% from 16.7% in the pcp. The improvement in the margin is due to a more favourable product mix which, together with cost efficiencies, had more than offset the adverse impact of the stronger transactional USD and the incremental increase in marketing and R&D expenditure. On a geographic basis, North American revenues, in constant currency, have continued to post a double digit growth compared to the pcp. ANZ revenues grew 20.1% higher than the pcp on an AUD reported basis and has contributed the highest growth rate of all regions. The growth has come mainly due to the releases of new product in the beverage category. The Rest of World revenues has posted 3.7% growth in AUD to $42.2m and on constant currency basis, the revenues were 14.8% higher than pcp. Both the Hong Kong distribution and the UK business have reported double digit growth in constant currency. There is a 17.2% growth in the revenue of the UK business in constant currency. On the other hand, the Distribution segment is facing challenges, particularly in the entry to mid-market segment, and the revenues of this segment declined by 13.7% to $74.3m in the half year of FY 17. There is a decline in the revenue due to the products sold through the mass channel, as the discount retailers continuing to favour their private label brands in the entry to mid-price points. In channels outside of the mass channel, the Distribution segment revenue fell slightly down over the pcp. Therefore, the Distribution Segment EBIT in the half year has posted $1.8m reduction to $3.3m. The EBIT margin of this segment has decreased to 4.4% from 5.9% in the pcp. The margin reduction was mainly due to the impact of a stronger transactional USD. However, the reduction in gross margin was offset marginally by the lower marketing expenses and cost efficiency savings.

1H 17 Segment Performance (source: Company Reports)

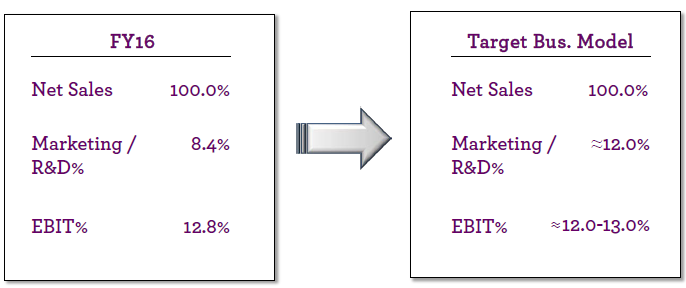

· Group strategic transformation: BRG has continued to progress through its strategic transformation in the key areas. The growth acceleration framework includes more product, larger market, scalable and acceleration platform and growth oriented business model. Moreover, the company has shortened the product development cycles and brought forward the new product releases, followed by their global launch in the transformation program. The product team has successfully shortened the development cycle for two products, and they are applying the process learning to other projects in the innovation pipeline. Further, to expand the market into which the company sell, in the last six months BRG has commenced shipping Nespresso products in North America (under the expanded license agreement) and executed a series of global marketing programs across the markets for the Christmas trading period. The company has also executed the first Sage brand transition in Europe with the distribution partner in the Baltics. BRG are also piloting the consolidation warehouse process with this partner, that resulted in a range expansion of approximately 40%. Additionally, BRG’s global systems rollout is on track. The company’s new global Customer Relationship Management (CRM) system rollout is in process, with North America live and other regions to follow in the coming months.BRG’s new eCommerce platform is expected to be launched by the end of the FY 17. In addition, BRG is still transitioning inventory turns and is on track to spend approximately 9.5% of revenue on marketing and R&D for the FY 17, up from the 8.4% spent in the FY16.

Migrating to a Growth-Oriented Business Model (source: Company Reports)

· Outlook for FY 17: BRG currently expects the EBIT growth rate in the second half of the FY17 to be generally consistent with the first half of the FY 17.

· Stock Performance: Meanwhile BRG stock has risen more than 10% (source:ASX) in last six months as on August 14th, 2017 and rose 4.7% on August 15, 2017. BRG is migrating to a growth-oriented business model. We give a “Hold” recommendation on the stock at the current price of $10.32

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...