Bravura Solutions Limited

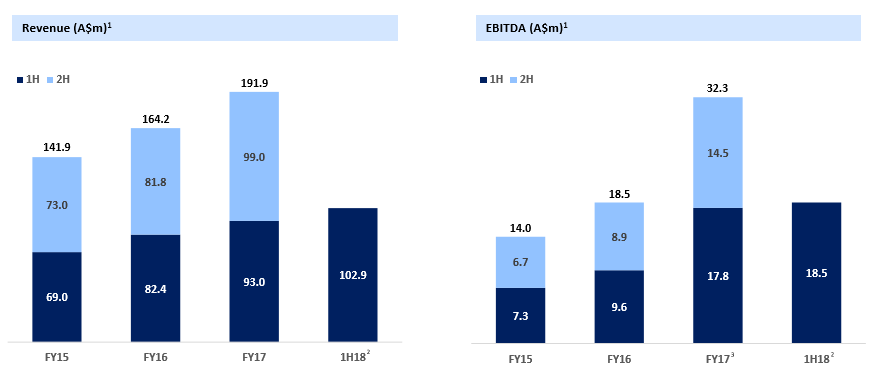

Strong result with rise in working capital consumption: Up 2.4% on February 26, 2018, Bravura Solutions Limited’s (ASX: BVS) half-year results for the period ended 31 December 2017 highlighted revenue growth of 10% to A$102.9m in 1H18 from A$93.5m in 1H17, driven by new clients across Bravura’s operating regions of EMEA and APAC, and better project work from existing clients with long-term contracts being in place. There was a 2% rise in EBITDA while EBITDA margin was 18%, finding support from strong growth in Wealth Management margins, offsetting the loss of a Funds Administration client. Underlying NPAT was up 13% to A$14.2m in 1H18 from A$12.6m in 1H17 while the group reported for lower net interest costs at the back of lower total debt carried on the balance sheet. While the group maintained its dividend policy of paying out between 60 and 80% of underlying earnings (dividend of 4.5 cents per share declared for the half), operating cash flow decreased to A$14.6m in 1H18 from A$16.7m in 1H17 and the group also increased its investment in recruitment and training to support the growth in professional services revenue. On the other hand, return on equity of 24% in 1H18 was reported.

The group has reported that the growth has been boosted by regulatory change, expanding digital distribution channels, and efforts on increased operating efficiency across the financial services industry. Wealth Management revenue growth of 26% has supported the result with EBITDA rise of 40% against Funds Administration EBITDA and investment in Corporate. 55% of group’s total revenue comes from Sonata that witnessed a revenue growth of 35% to A$56.7m with client wins in South Africa (Discovery) and New Zealand (ASB Bank). The 2018 guidance has been revised upwards and is expected to lead to underlying EPS growth in the high-teens while funds Administration are expected to return to growth in 2H FY18. We would wait for any dip in the stock price for an investment opportunity as the stock looks “Expensive” at the current price of $2.11

Revenue and EBITDA in constant currency (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...