Stocks’ Details

Bubs Australia Limited

Substantial Growth in Revenue: Bubs Australia Limited (ASX: BUB) is engaged in the manufacturing of infant milk formula. The market capitalisation of the company stood at ~$579.91 Mn as on 7th July 2020. Recently, the company announced that it has reached a new supply agreement with Coles Supermarkets Australia. Under the agreement, Bubs Organic® Grass-Fed Infant Formula would be distributed to 482 Coles supermarkets. The company notified that the incremental distribution of Bubs Organic® Grass-Fed Infant Formula is in addition to the continued sale of Bubs® Goat Milk Infant Formula, which is ranged in 561 stores and Bubs Organic® Toddler Snacks ranged in up to 804 stores. During Q3 FY20, the company achieved record revenue amounting to $19.7 million, reflecting a rise of 67% over pcp. The company reported positive quarterly operating cashflow of $2.3 million. The quarter reflected the strength of Bubs Australia’s business model and agility of its team to continue to meet the needs of Bubs Family in a challenging operating environment.

.png)

Cash flows (Source: Company Reports)

Effectively Meeting the Rise in Demand: The company continues to be fully focused on ensuring that its integrated supply chain is responsive to the increased demand being observed in all channels. On the back of its operating flexibility from its vertical supply chain and strong balance sheet position, the company is agile and able to quickly respond to a fast-moving situation.

Key Risks: Bubs Australia Limited’s business is mainly exposed to customer credit risk, which arises largely from the inability of payment by customers. In addition, the Group carries out transactions in Australia, New Zealand, China and Europe and is exposed to currency risk arising from movements in currencies.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 3.03x in 1H FY20 as compared to the industry median of 1.73x. This indicates that the company is in a decent position to address its short-term obligations against the peer group. Debt to equity multiple of the company stood at 0.04x in 1H FY20 against the industry median of 0.22x. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method. For the purpose, we have taken peers such as A2 Milk Company Ltd (ASX: A2M), Freedom Foods Group Ltd (ASX: FNP) and Baby Bunting Group Ltd (ASX: BBN) and arrived at a target price of high single-digit upside (in percentage terms). Thus, considering the new supply agreement with Coles Supermarkets Australia, decent performance in Q3 FY20, decent liquidity position and deleveraged balance sheet, we maintain a “Hold” recommendation on the stock at the current market price of $1.050 per share, up by 1.449% on 7th July 2020.

Coca-Cola Amatil Limited

Resilient Balance Sheet Position: Coca-Cola Amatil Limited (ASX: CCL) is involved in the manufacturing, distribution and marketing of beverages. The market capitalisation of the company stood at ~$6.48 Bn as on 7th July 2020. In a recent trading update, the company stated that the month of April 2020 was challenging with the full brunt of the COVID-19 restrictions felt in all of its markets throughout the peak Easter and Ramadan trading periods. As a result, the company experienced a drop of around 33% in gross volume. Moreover, trading in the first three weeks of May 2020 has also witnessed a decline of around 26% in volume on the pcp; this reflects an improvement on the April run rate of -33%. The below picture gives an overview of the financial performance for FY19:

.png)

Key Metrics (Source: Company Reports)

Strong Operational and Financial Position: The company believes that its strong balance sheet, ample liquidity, robust cashflows as well as solid credit ratings place it in a decent financial and operational position to trade through the uncertain period and emerge as a stronger and better business.

Key Risks: The company is mainly exposed to beverage industry risk, which arises from the fundamental shifts in the beverage and macroeconomic landscape. These include changing consumer trends, increasing margin pressure as manufacturer margins are squeezed by major retailers, a fragmented and price competitive trading environment, digital disruption to supply chain, etc. Moreover, termination of agreements with key brand partners like The Coca-Cola Company or unfavourable renewal terms can adversely impact the company’s profitability.

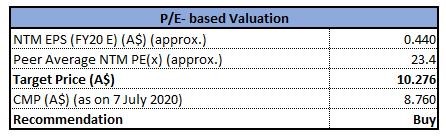

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: Over the span of five years (2015-2019), the company reported a CAGR of 3% in free cash flow. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with low double-digit upside (in percentage terms).For the purpose, we have taken peers such as Treasury Wine Estates Ltd (ASX: TWE), Wesfarmers Ltd (ASX: WES), Coles Group Ltd (ASX: COL), etc. Thus, considering the strong balance sheet, ample liquidity, robust cashflows, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $8.760 per share, down by 2.123% on 7th July 2020.

Keytone Dairy Corporation Limited

Repetitive Orders from Nouriz: Keytone Dairy Corporation Limited (ASX: KTD) is a manufacturer, packer and exporter of dairy and nutritional products. The market capitalisation of the company stood at $69.28 Mn as on 7th July 2020. Recently, the company has received the largest follow-on order of $1,391,000, from Nouriz (Shanghai) Fine Food Co Ltd for their Whole Milk and Skim Milk Powders. These orders will be manufactured in the company’s New Zealand facilities through August 2020. The company has also completed its Share Purchase Plan offer and raised funds worth $359,052. During FY20, the company reported total sales of $22.53 million against $2.51 million in FY19. Moreover,FY20 has recorded another phase of rapid expansion, significant growth as well as investment in a diversified platform across Australia and New Zealand for which the business is currently well capitalised and positioned.

.png)

Group Quarterly Revenue Growth (Source: Company Reports)

Focus on Increasing Shareholders Wealth: The company is focused on sustained growth in shareholder wealth, consisting of growth in share price, and delivering a constant or increasing return on assets.

Key Risks: Any transaction denominated in foreign currency exposes the business to foreign currency risk through foreign exchange rate fluctuations. Any default by a counterparty to fulfill its contractual obligations gives rise to credit risk. Inability to maintain sufficient liquid assets exposes the business to liquidity risk and may cause disruptions in operations.

Stock Recommendation: During FY20, cash receipts from customers stood at $24.68 million as compared to $2.86 million in FY19. The company closed the financial year 2020 with a cash balance of $4.4 million. The stock of KTD has corrected by 25.00% and 29.87% in the last three months and six months, respectively. The stock of KTD is inclined towards its 52-week low of $0.195. The stock is trading at a price to book value multiple of 1.0x as compared to the industry median (Food & Tobacco) of 1.3x on TTM basis. Thus, considering the follow-on order from Nouriz, decent performance in FY20 and rise in cash receipts, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.260 per share, down by 3.704% on 7th July 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...