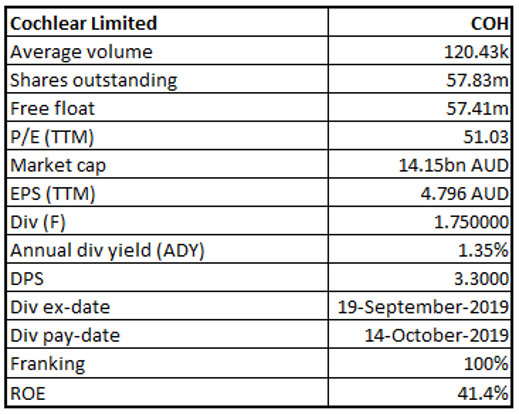

Cochlear Limited

COH Details

Guidance Revised Downward: Cochlear Limited (ASX: COH) is engaged in the manufacturing of Cochlear implant systems. The market capitalisation of the company stood at $14.15 billion as on 11th February 2020. The company recently reduced its guidance for FY20 for underlying net profit to $270-290 million as compared to the previous guidance of $290-300 million. This decrease in guidance is because of the anticipated impact from the novel coronavirus in Greater China. Hospitals are deferring the surgeries to limit the risk of infection from the coronavirus.

The company advised that during the SARS epidemic, it witnessed a material decrease in sales in China. However, the company is confident that delayed surgeries would progress once hospitals resume normal operations. On the financial front, the company reported a rise of 7% in sales revenue in FY19 and the figure stood at $1,446.1 million. During FY19, the company paid fully franked total dividend of 3.3 cents.

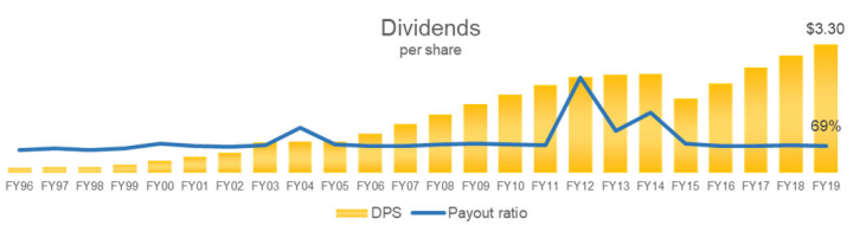

Dividend Growth (Source: Company Reports)

What to Expect: The company continues to anticipate growth in revenue and earnings in the upcoming years, which would be supported by the investments made in product development and market growth initiatives. It continues to target a dividend payout ratio of around 70% of the net profit for FY20. COH anticipates strong growth in cochlear implant units in developed markets, which will be generated by the recent launch of the Nucleus Profile Plus Series cochlear implant as well as continued investment in market awareness and access activities.

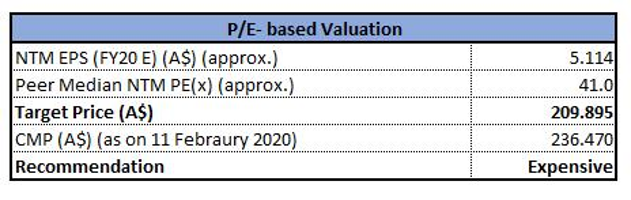

Valuation Methodology:P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company is expecting a fall in capital expenditure of around $100 million in FY21. The company is aiming to maintain its net profit margin. We have valued the stock using P/E based relative valuation method, and for the purpose, we have taken peers such as CSL Ltd (ASX: CSL), Resmed Inc (ASX: RMD) and Sonic Healthcare Ltd (ASX: SHL) and arrived at a target price, which is offering corrections of lower double-digit (in percentage terms). As per ASX, the stock of COH is trading close to its 52-week high of $245.430. Hence, considering the valuations and current trading levels, we give an “Expensive” rating on the stock at the current market price of $236.470 per share, down by 3.387% on 11th February 2020. The fall in stock price was primarily due to a reduction in guidance.

COH Daily Technical Chart (Source: Thomson Reuters)

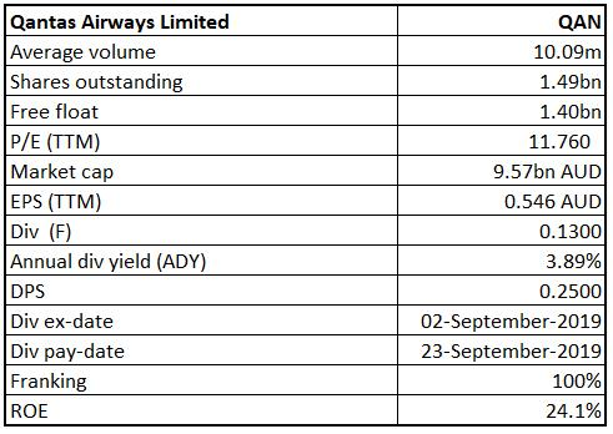

Qantas Airways Limited

QAN Details

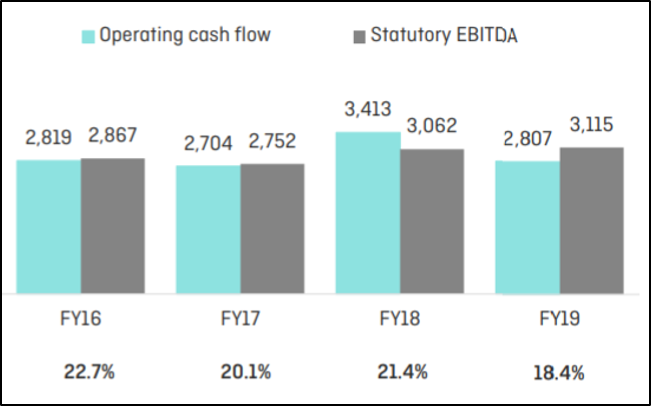

Record Total Group Revenue: Qantas Airways Limited (ASX: QAN) is engaged in international and domestic air transportation services. As on 11 February 2020, the market capitalization of the company stood at ~$9.57 billion. For the quarter ended 30 September 2019, the company reported a record total group revenue of $4.56 billion, up by 1.8%. During FY19, statutory EBITDA witnessed a slight increase and stood at $3,115 million from $3,062 million. Despite higher oil price, the company made a profit of $1.3 billion. The decent financial performance enabled to Board to declare a fully franked dividend of 13 cents per share.

Statutory EBITDA and Operating Cash Flow (Source: Company Reports)

Future Expectations and Growth Opportunities: The company is uniquely positioned through its Customer loyalty and insights, Home market strength and other key competitive advantages. It has hedged its fuel for FY20 to benefit from any fall in oil prices. The company expects its full-year fuel cost to be around $3.98 billion. QAN also expects the group capacity to grow between 0.5% to 1% in the first half of FY20 and is on track to deliver at least $400 million in transformation benefits in FY20.

QAN is well-positioned to deliver higher domestic operating margins owing to its stable market structure and its focus on cost reduction. The company is on track for growth, innovation and resilience and expects to drive $500-600 million of EBIT in FY22. The company has provided its long-term outlook and is targeting EBIT margin of ~18% in FY24 from its Qantas Domestic segment. It is also targeting zero net carbon emissions by 2050 and is expecting to reduce the use of plastic by the end of 2020. On the face of coronavirus outbreak, various flights disruption and knock-on effect on tourism industry, QAN is likely to see an impact on the business.

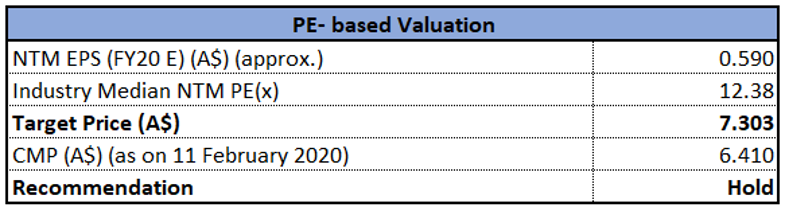

Valuation Methodology: P/E Based Valuation

Price to Earnings Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of QAN gave a return of 11.65% in the past 6 months. During FY19, gross margin of the company was 53.2%, higher than the industry median of 39.7%. In the same time span, Return on Equity was 24.1% as compared to the industry median of 5.2%. Considering the returns, trading levels, higher ROE and modest outlook, we have valued the stock using P/E based relative valuation method and arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $6.410, down by 0.156% on 11 February 2020.

.jpg)

QAN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...