Bionano Genomics Inc.

Bionano Genomics Inc. (NASDAQ: BNGO) is a life sciences instrumentation company in the genome analysis space. The group develops and distributes Saphyr system, a platform used for ultra-sensitive and ultra-specific structural variation detection. The above system enables researchers and clinicians to enhance the detection of new diagnostics and therapeutic targets and to simplify the study of changes in chromosomes.

Key Updates:

- Proposed Public Offering of Common Stock: Recently, the company announced that it is planning to sell its common shares through an underwritten public offering. The management is likely to grant the underwriters a 30-day option to purchase up to an additional 15% of the total common stock offered.

- Business Expansion: The company has expanded its presence across Europe with the adoption of Saphyr across three largest pediatric hospitals in Spain, Italy and France. Moreover, the company expanded its Global business with the adoption of Saphyr for Next-Generation Cytogenomics in Eastern Europe, Australia and Canada. We believe, with the above expansion, the group would enhance its product presence across several new geographies which would further lead to improved business prospects.

Q3FY20 Financial Highlights:

- BNGO announced its quarterly results, wherein the company posted total revenue of USD 2.196 million, as compared to USD 3.313 million in the previous corresponding period (pcp). The decline was primarily attributable by a change in the mix of revenue between instrument sales and its reagent rental program.

- Total cost of revenue stood lower at USD 1.46 million, significantly lower than USD 2.375 million in Q3FY19. However, the group reported a slightly higher research and development costs (USD 2.30 million versus USD 2.17 million in pcp) and a significantly higher selling, general and administrative expense (USD 8.659 million versus USD 4.44 million in pcp). The increase in selling, general and administrative expense was due to higher legal and accounting fees required to support business operations and its international presence.

- Loss from operations extended to USD 10.228 million, as compared to USD 5.685 million in pcp.

- The company reported a net loss of USD 10.792 million, as compared to a loss of USD 6.398 million in Q3FY19.

- The company reported cash and cash equivalent of USD 18.867 million, while total assets were recorded at USD 41.396 million.

Q3FY20 Income Statement Highlights (Source: Company Reports)

Risks: The company’s overall operations have been hindered by weak revenue mix during Q3FY20, and continuation of the above trend would likely to dampen the overall performance.

Stock Recommendation:

The company received German accreditation of Laboratory Developed Test for genetic disease testing, which is a key positive. Moreover, the group has improved its Saphyr System through fast and simple DNA isolation protocol to process solid tumor samples. We believe, despite the above developments, the company’s upcoming business prospects would highly depend upon the acceptability of the company’s products for individual clinical trials and related medical purposes. Moreover, the company has increased its long-term debt component by USD 1.8 million in Q3FY20. The stock of BNGO soared 922% and 1,482% in the last six months and nine months, respectively. On the valuation front, the stock is trading at an EV to Sales of 42.7x on NTM basis, significantly higher than the industry average (Healthcare Equipment & Supplies) of 11.0x. Hence, considering the above facts, current price movement, we recommend an ‘Expensive’ rating on the stock at the closing price of USD 5.00 on January 07, 2021.

BNGO Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Aqua Metals, Inc.

Aqua Metals, Inc. (NASDAQ: AQMS) is engaged in recycling lead through process that the Company developed and named AquaRefining. The Company's AquaRefining approach focuses on recycling lead-acid batteries (LABs) and the production of lead using bio-degradable aqueous solvent and an ambient temperature electro-chemical process to produce lead.

Key highlights

- Debt-free balance sheet:Recently, the Company announced that they had retired its USD 9.0 million debt obligation with Veritex Bank, making them debt-free. Further, the Company has received an additional progress payment of USD 0.8 million from its insurance provider. The retirement of the loan is positive Aqua Metals as it improves the Company’s cash burn rate by eliminating USD 0.9 million annually in debt service payments, including USD 0.6 million in interest expense.

- Positive demand prospects for lead:LAB market is driving the growing demand for the lead as annual LAB sales are expected to nearly double to USD 84+ billion by 2025. Today the LAB production constitutes the largest lead as it represents over 95% of all batteries produced due to improved recyclability, safety and performance compared to Li-ion and NiMH.

Source: Company

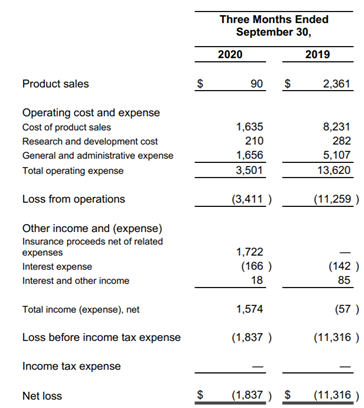

Financial overview of Q3 2020

Source: Company

- In Q3 2020, the company reported revenue of USD 90,000 compared to USD 2.3 million in the previous corresponding period. Since the lead recycling facility was not in production during the third quarter of 2020 due to the fire and the acceleration of licensing strategy. Revenue was realized from the sale of inventory consisting of lead compounds generated during pre-fire operations.

- The company posted a loss from operations at USD 3.4 million in Q3 2020, compared to a loss of USD 11.26 million in Q3 2019.

- Net loss in Q3 2020 stood at USD 1.8 million, compared to USD 11.3 million in the previous corresponding period. This performance was mainly due to the fire accident due to which the lead recycling facility was not in production.

Risks associated with investment

The Company is under various market risks in the ordinary course of operations that could impact its earnings and cash flows. Some important risk factors are global economic conditions that could negatively affect their prospects for growth and operating results. Any further fire accident could also bring their operations standstill,

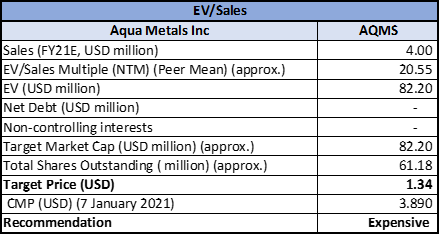

Valuation Methodology (Illustrative): EV to Sales

Stock recommendation

The company recently announced that they are now debt-free, after paying USD9.0 million debt obligation to Veritex Bank. This would help them save USD0.6 million in interest expense. Also, the LAB market demand outlook looks rosy as the LAB sales are expected to nearly double to USD84+ billion by 2025. But the fire accident has turned out to be a nightmare for the company because they recognized minimal revenue during Q3 2020. During the quarter, the revenue earned from the sale of inventory consisting of lead compounds that were generated during pre-fire operations. We have valued the stock using EV to Sales based relative valuation and arrived at a target downside of double digit (in % terms). Therefore, based on the above rationale and valuation, we recommend an "Expensive" rating at the closing price of USD 3.89 on January 7, 2021. We have considered Johnson Controls International PLC, Pyrogenesis Canada Inc, China Recycling Energy Corp, etc. as the comparison's peer group.

Source: Refinitiv (Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...