.png)

Stocks’ Details

Southern Cross Electrical Engineering Limited

Decmil Subcontract Update: Southern Cross Electrical Engineering Limited (ASX: SXE) provides large-scale specialized electrical, control and instrumentation installation and testing services for the resources, infrastructure, and heavy industrial sectors. As on 25 June 2020, the market capitalization of the company stood at ~$108.95 million. SXE, with respect to a subcontract with Decmil to design, supply and construct the electrical, communications, instrumentation and controls for the non-processing facilities at Rio Tinto’s Amrun mine project, is pursuing its claims for payment against Decmil under the dispute resolution provisions in the Subcontract.

Record Half-Year Revenue: During 1H20, the company reported record half-year revenue of $230.3 million, up by 27% on pcp, and saw an increase of 21% in EBITDA to $10.9 million. In the same time span, EBIT of the company stood at $8.4 million. The company also reported a strong debt-free balance sheet with total cash of $53.3 million.

.png)

1H20 Financial Highlights (Source: Company Reports)

Key Risks: With the implementation of inter-state and intra-state travel restrictions, the company has delayed some planned capital expenditure and investment activities. The company has also been notified of postponement of some minor projects.

What to Expect: Despite some initial fears of disruption to supply chains, the company did not face any significant issue in procuring materials. The company is preserving cash and has a strong liquidity position. Therefore, it is well-capitalized to navigate through this difficult period.

Stock Recommendation: The company has grown and is well-diversified to capitalize on growth opportunities. A strong business development pipeline and continued progress of the company place it in a position to leverage additional opportunities. On Trailing Twelve Months Basis (TTM), the stock is trading at an EV/EBITDA multiple of 2.5x, lower than the industry median (Industrials) of 6.5x, which indicates share price is undervalued. As per ASX, the stock of SXE gave a return of 23.94% in the past three months and is inclined towards its 52-week low of $0.335, proffering a decent opportunity for accumulation. Considering the attractive trading levels, decent returns in the past three months, financial resilience despite the uncertainty and modest outlook, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.430, down by 2.273% on 25 June 2020.

RXP Services Limited

Strong Cash Conversion: RXP Services Limited (ASX: RXP) is an Information and Communication Technology professional services company that provides digital consulting services. As on 25 June 2020, the market capitalization of the company stood at ~$42.69 million. During 1H20, revenue of the company stood at $65 million, and underlying EBITDA of the company was $6.7 million. In the same time span, the company had a strong cash conversion of 127%. RXP won several significant clients in early 2020 totaling to ~$25 million.

.png)

1H20 Financial and Operational Highlights (Source: Refinitiv, Thomson Reuters)

Key Risks: The increasing spread of the COVID-19 crisis and the associated responses have created an uncertain outlook and can potentially create some operational challenges going forward. The company is also exposed to credit risk, market risk, etc.

What to Expect: RXP continues to operate with a comfortable gearing position. A key benefit of the company’s operations is that all of them can be implemented remotely. RXP’s operations and financial performance have not been materially impacted due to COVID-19.

Stock Recommendation: The company has continued its operations with a conservative approach and is in a solid position with a cash balance of $8.1 million and net debt of $13.9 million as on 31st December 2019. As per ASX, the stock of RXP gave a return of 26.19% in the past three months and is trading close to its 52-weeks’ low level of $0.190. On Trailing Twelve Months Basis (TTM), the stock is trading at an EV/EBITDA multiple of 3.9x, lower than the industry median (Industrials) of 6.5x, and thus, seems to be undervalued. Considering the attractive trading levels, decent returns in the past three months and comfortable gearing position, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.260, down by 1.887% on 25 June 2020.

Ridley Corporation Limited

Solid Operating Performance: Ridley Corporation Limited (ASX: RIC) is engaged in the production of animal nutrition solutions, including stock feed milling and the marketing and provision of rural products and services. As on 25 June 2020, the market capitalization of the company stood at ~$226.96 million. During 1H20, the company reported a solid operating performance with an EBITDA of $30.7 million, marginally up on corresponding prior-year period. RIC is modernising its assets and has secured control over its Thailand operations for expansion.

.png)

1H20 Financial and Operational Highlights (Source: Company Reports)

Growth Strategy: The new structure of the company provides a single point of accountability for both the customer servicing and operation of the supplying facility. The company is commercializing its pipeline of innovation opportunities. RIC has significant opportunities to simplify the business, install automation, leverage its raw material and consumable procurement, and to rationalize the supply chain. The overall outlook for the business is positive, with another strong year expected for the Ruminant business driven by high milk prices.

Key Risks: The company might face significant operational risks. Cyclical fluctuations impacting the demand for animal nutrition products may adversely impact the diversified portfolio. Performance of RIC may also be impacted by the influence of the domestic grain harvest.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company expects the poultry volume to improve in the coming years as the industry reverts to its traditional bird lifecycle. As per ASX, the stock of RIC is trading close to its 52-weeks’ low level of $0.655, proffering a decent opportunity for accumulation. We have valued the stock using the price to earnings multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). Considering the attractive trading levels, long-term outlook and decent growth strategy of the company, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.665, down by 6.993% on 25 June 2020.

Healius Limited

Simplified Portfolio with Leading Market Position: Healius Limited (ASX: HLS) is a service company for medical, para-medical, and related services, and a day surgery operator. As on 25 June 2020, the market capitalization of the company stood at ~$1.97 billion. During 1H20, the company reported a strong growth trajectory in Day Hospitals after a ramp-up of new sites. Over the span of 3 years from 1H17 to 1H20, the company witnessed a CAGR of 11% in pathology EBIT and a CAGR of 14% in imaging EBIT. The company is looking to entrench several short-term COVID initiatives and further reset cost base.

.png)

Growth in EBIT (Source: Company Reports)

Key Risks: The company has experienced varying rates of volume decline in its businesses due to significant deferral of non-COVID19 testing and elective services. While most of the company’s revenue comes from Medicare Benefits Schedule (MBS) reimbursements, HLS does charge out-of-pockets on some services. Consequently, consumers may delay or not use services due to affordability concerns, impacting volumes and revenue.

What to Expect: The company is focusing on leading diagnostics business and day hospitals. The company is aiming for the higher value and higher growth businesses with improved shareholder returns. The company has a strong balance sheet and is well-positioned to execute on value-generating initiatives. HLS expects to remain within its banking covenants in the 2020 financial year and is targeting to maintain its bank gearing ratio below 3.0x.

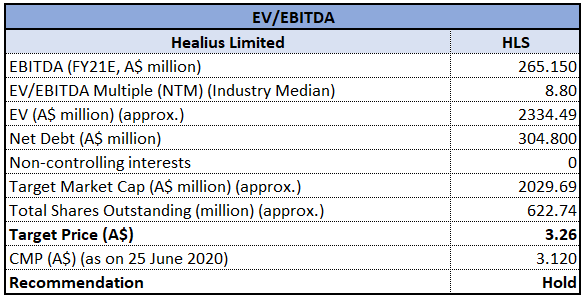

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In Medical Centres of the company, patient visits remain strong, and telehealth currently totals around 40% of all presentations. The rapid adoption of telehealth services by HLS is assisting with good GP recruitment and retention rates. As per ASX, the stock of HLS gave a return of 40.89% in the past three months and a return of 34.89% in the last one month. The stock of HLS is trading close to its 52-weeks’ high level of $3.315 but holds the potential for growth. We have valued the stock using the EV/EBITDA multiple based Illustrative relative valuation method and have arrived at a target price of single-digit upside (in percentage terms). Considering the current trading levels, attractive returns in the past three months, positive outlook and CAGR in EBIT, we recommend a ‘Hold’ rating on the stock at the current market price of $3.120, down by 1.577% on 25 June 2020.

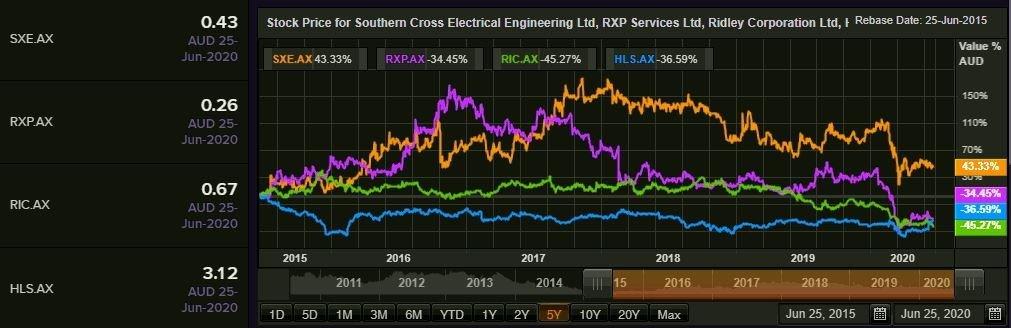

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...