Kalkine has a fully transformed New Avatar.

Propel Funeral Partners

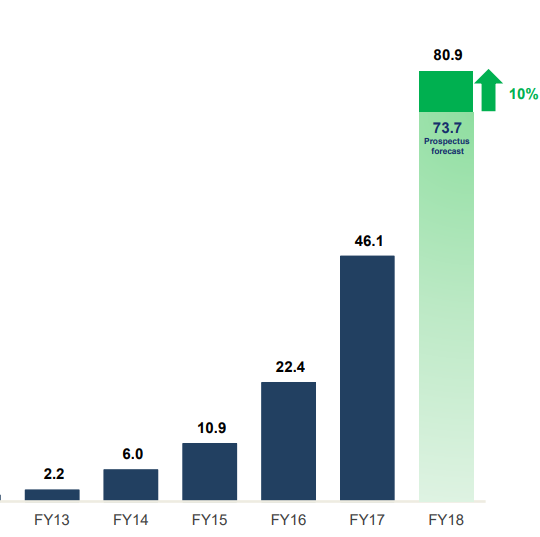

Mortality trends to boost the stock: Propel Funeral Partners Ltd (ASX: PFP) has posted 76% rise in the FY18 revenue at $80.9 Mn compared to $46.1 Mn in FY17. Funeral volumes were up 67% which helped the company achieve positive numbers. Operating EBITDA for the company came in at $21.5 Mn, an increase of 75% from FY17 number of $12.3 Mn

Revenue Growth (Source: Company Reports)

Death Volumes in Australia has increased by 0.9% pa between 1990 and 2016; and in New Zealand, it has surged 0.6% between the same period. Since the company is projecting that the volume would grow 1.4% from 2016 to 2025 and 2.2% from 2025 to 2050 in Australia, it would benefit the whole death care industry including Propel. Similarly, in New Zealand the volume growth is pegged at 1.1% p.a. from 2016 to 2025 and 1.8% from 2025 to 2050.

Going forward, the company is expected to draw benefits from acquisitions completed during and since FY18 along with other property transactions. On the valuation front, the company has maintained its Gross Margin at 40.7% in 2018 against 40.3% in FY17. Propel has also maintained sufficient liquidity with current ratio at 1.35x compared to industry average of 1.11X.

The stock has generated negative YTD return of 15.41% and has been in a downward spiral for quite some time now. However, recent consolidation of the prices with positive 14-day Relative Strength Indicator suggests that buying might come at lower levels from the investors who are looking for decent risk-reward ratio. We believe that PFP is set to benefit from the aforementioned factors and therefore recommend ‘Speculative Buy’ in the stock at the current price of $ 2.950 (up 1.4% on September 11, 2018).

Invocare

Disappointing Bottomline numbers: Invocare Ltd.’s (ASX: IVC) shares dipped 1.029% on September 11, 2018, as one of the directors, Richard Hugh Davis lately offloaded 40,000 shares at $12.65. Moreover, Australian Super Pty Ltd also ceased to be the substantial shareholder in Invocare Limited.

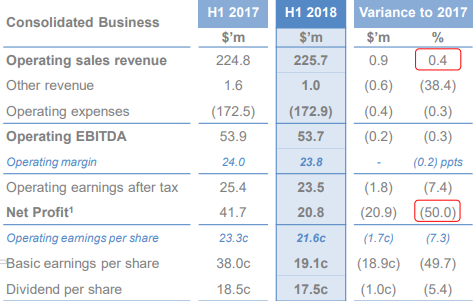

The stock has been reeling low after gap down following the disappointing first half year 2018 result. Revenue of the company witnessed hairline growth of 0.4% at $225.7 Mn compared to the previous corresponding period. Increasing expenses impacted the reporting profit which was down 50% at $20.8 Mn compared to the previous comparable period. The drop-in profit was primarily due to impact of mark to market valuation of prepaid contracts in 2017 which included substantial gain due to prepaid property valuations.

There was no growth in the market share of the company pertaining to factors such as loss of volume through temporary closures, US operations wind up and reduction in the number of deaths. The company has declared 1H FY18 dividend at 17.5 cents per share fully franked which was lower compared to the 18.5 cents in 1H 2017.

Financial Performance Snapshot (Source: Company Reports)

Stock Performance: The stock has generated negative Year to date return of 20.89% and might register further fall owing to its expensive valuation at 18.070 x compared to peers. We believe that muted topline numbers and inability to improve bottomline numbers would affect the stock price going ahead. The company might start deriving value from the slew of acquisitions made this year but as of now it is a long shot and uncertain if the entities would not be able to generate healthy revenue stream for the company. We therefore maintain an ‘Expensive’ recommendation on the stock at current market price of $12.50.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...