.png)

Stocks’ Details

Mayne Pharma Group Limited

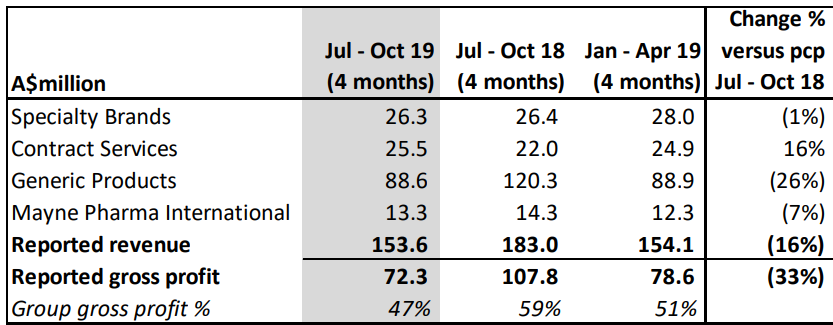

Stable Balance Sheet with Reduction in Net Debt:Mayne Pharma Group Limited (ASX: MYX) is a pharmaceutical company focused on applying its drug delivery expertise to commercialise branded and generic pharmaceuticals. In the recently held Annual General Meeting, the top management of the company addressed its shareholders and stated that group revenue to the end of October stood at $154 million, down by 16% on the prior corresponding period (pcp). Its gross profit of the company went up by 13% on YoY basis to $290 million in FY19 from $256.6 million in FY18. The company has also managed to reduce its net debt by $18.0 million in 2HFY19, resulting in bank leverage ratio of 2x. It can be said that the reduction in the net debt might help the company to focus on strategic growth objectives.

Financial Performance (Source: Company Reports)

What to Expect: The company is actively rebalancing its portfolio to specialty products led by the commercialisation of E4/DRSP oral contraceptive. The company expects that US specialty products to contributing around 60% of revenue by FY24. It was added that Specialty Brands is expected to benefit from the product launches of TOLSURA® and LEXETTE®, and from E4/DRSP in FY 2022.The company expects group operating expenses to be lower in FY20 as compared to FY19 on a constant currency basis.

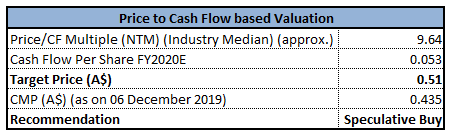

Valuation Methodology: Price to Cash Flow Multiple Approach

Price/Cash Flow Multiple (Source: Thomson Reuters) *NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of MYX gave a negative return of 17.14% in the last one month and is currently trading close to its 52-week low of $0.430.In the time span of 5 years from FY15 to FY19, the company witnessed a CAGR of 38.89% in revenue and a CAGR of 40.92% in gross profit. During the year, EBITDA margin of the company stood at 27.9%, higher than the industry median of 24.1%, indicating stable business earnings. Current ratio of the company was 2.23x as compared to the industry median of 1.91x. Thus, considering the current trading levels, business growth in last 5-years, above industry margin and modest outlook, we have valued the company using a relative valuation, i.e., Price/Cash Flow valuation multiple, and arrived at a target price, offering a lower double-digit return (in percentage terms). Hence, we give a “Speculative Buy” rating on the stock at the current market price of $0.435, down by 1.136% on December 06, 2019.

ICSGLobal Limited

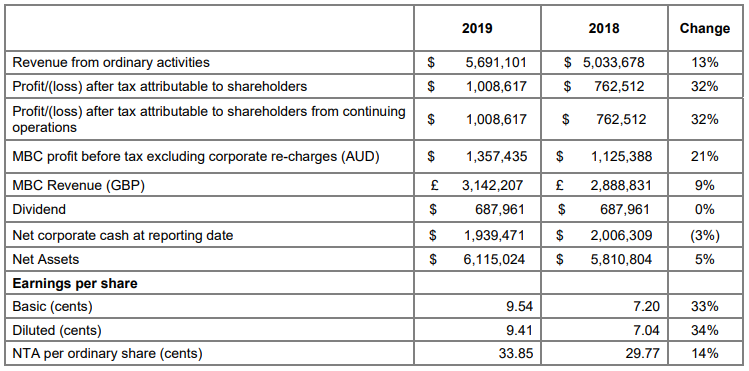

Substantial Rise in Profit: ICSGlobal Limited (ASX: ICS) is a holding and investment company, which operates a medical billing service in the UK. As on 06 December 2019, the market capitalisation of the company stood at $21.22 million. In the recently held Annual General Meeting of the company, the top management addressed its shareholders and stated that revenue of the company has gone up by 13% to $5.69 million in FY19 and net profit after tax stood at $1 million, up by 32% on prior period. The company also reported astrong financial position and has a corporate cash of $1.95 million at the year end, after paying dividends of $687,961. In the time span of 5 years from FY15 to FY19, the company has witnessed a CAGR of 10.26% in revenue and a CAGR of 10.37% in gross profit.

Financial Performance (Source: Company Reports)

What to Expect: The company has recently updated the guidance for profit after income tax and expects it to be in the range of $1.4 million to $1.7 million due to the continued success in gaining new clients and operational leverage. It also expects to start a major project at the beginning of 2020 and is currently exploring further channels to increase the growth rate.

Stock Recommendation: As per ASX, the stock of ICS gave a return of 113.13% in the past one year and a return of 108.91% in the past 6 months. The stock is currently trading close to its 52-week high of $2.120. The company’s Return on Equity (ROE) stood at 16.9% as compared to the industry median of 11.7%. In terms of valuation, the stock is trading at a P/E multiple of 22.120x, higher than the industry median (Consumer non cyclicals) of 11.5x on TTM basis. EV/EBITDA of the company stood at 15.3x as compared to the industry median of 9.5x on TTM basis. Thus, taking into account the current trading levels and stretched valuations, we recommend a “Sell” rating on the stock at the current market price of $2.110, up by 6.03% on December 06, 2019.

Simavita Limited

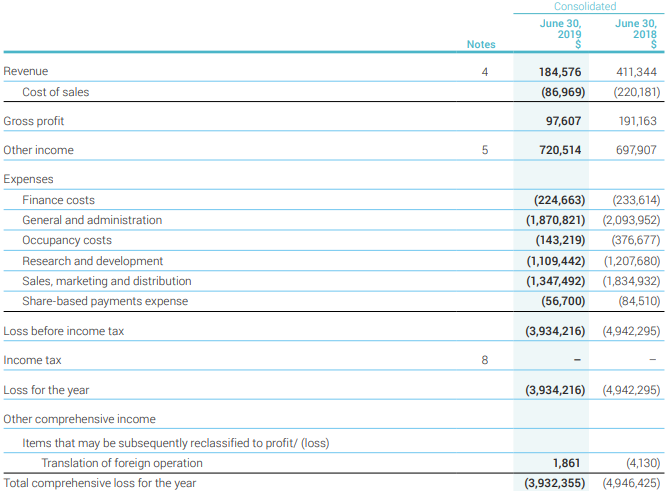

Simavita Limited (ASX: SVA) develops and markets advanced systems associated with smart, wearable and disposable sensors for the health care industry. The company has recently confirmed the receipt of $683,621 under the Australian Government’s Research and Development Tax Incentive Scheme and has announced that it has received CE Mark approval for Smartz™, designed for extensive use in both adult and infant markets. During the year, the group reported a loss after tax of $3.93 million, down by 20% on the prior period due to a decline in total operating expenses.

Financial Performance (Source: Company Reports)

What to Expect: With respect to The Smartz™ opportunity, the company added that this happens to be a true industry disruptive technology. It has a low recurring cost model and is addressing market needs for a better environmental solution. In the annual report, the company stated that there is expectation that medtech companies would continue to play a significant role in reducing the medical costs, optimizing provider performance, as well as improving patient outcomes.

Stock Recommendation: As per ASX, the stock gave a return of 144.44% in the past 3 months and a return of 175% in the last one month. The stock has witnessed high volatility in the last five trading sessions and has corrected 24.14%. In terms of valuations, the stock is trading at an EV/Sales multiple of 62.2x, higher than the industry median (Healthcare) of 8.7x on TTM basis. Thus, considering the substantial gain in the last one and three months, recent volatility in stock price and stretched valuation, we recommend a “Sell” rating on the stock at the current market price of $0.022, down by 26.667% on December 06, 2019.

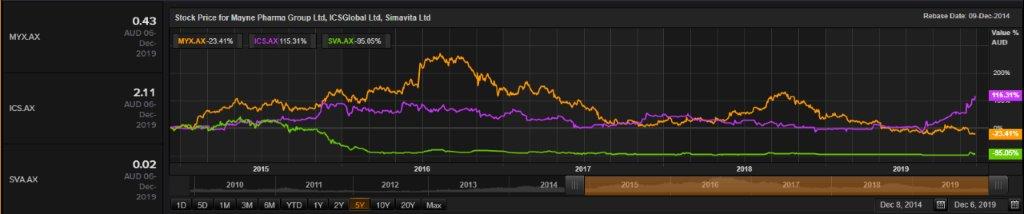

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...