Stocks’ Details

Bega Cheese Limited

A Rise in Normalised Revenue:Bega Cheese Limited (ASX: BGA) is engaged in the processing, manufacturing, cutting and packaging traditional cheese products. The company is also involved in the manufacturing of high-value dairy products. The market capitalisation of the company stood at A$874.12 Mn as on 20th December 2019. The company recently announced that Macquarie Group Limited currently holds a relevant interest (including shares held in nominee companies) of 5.10% in the company’s shares as at 17th December 2019. During FY19, the company reported a rise of 5% to $115.4 million in normalised earnings before interest, depreciation and tax as compared to the previous year.

.png)

Key Financials (Source: Company Reports)

The Expectation for EBITDA:For FY20, the company is expecting normalised EBITDA in the ambit of $95 - $105 million against $115 million in FY2019. The company is well advanced in its plans to restructure its manufacturing capacity for meeting the changing supply environment, which includes the development of toll and third-party manufacture relationships to ensure its efficient use of capital within the dairy industry.

Valuation Methodology: Price to Cash flow Multiple Approach

.png)

Price to Cash flow Multiple (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation:The company has been reviewing its supply chain and overhead cost to remain competitive and will continue to manage its supply chain for domestic and international trade to mitigate further downside risk. We have valued the stock using price to cash flow-based relative valuation method and arrived at a target price of lower double-digit upside (in percentage terms). Thus, considering the company’s decent balance sheet with total assets of $1.489 billion, total liabilities of $663 million and increased export sales, we give a “Buy” recommendation on the stock at the current market price of A$4.110 per share, up 0.735% on 20th December 2019.

Redbubble Limited

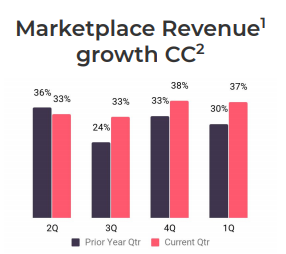

Trading Update for Q2 FY20:Redbubble Limited (ASX: RBL) is a global online marketplace company and has a market capitalization amounting to A$254.91 Mn as on 20th December 2019. Perennial Value Management Limited has become an initial substantial holder in the company, with a 5.17% voting power. Redbubble group recently notified the trading update for Q2 FY20. Marketplace Revenue growth for the second quarter to date (from October 1, 2019 to December 9, 2019) was estimated at 20% YoY on a floating basis. The TeePublic branded marketplace showed a good performance, where QTD Marketplace Revenue growth stood at 59% on the YoY basis. However, in Q1 FY20, the marketplace revenue amounted to $70 million, reflecting a yoy growth of 37% on a constant currency basis.

Marketplace Revenue (Source: Company Reports)

Expectation of Positive FCF: RB Group has been generating growth in revenue by focusing on accelerating near-term work, which includes marketing optimisation, product merchandising and line extensions as well as growing member revenue.The Group anticipates to grow operating EBITDA on YoY basis and expects to achieve positive free cash flows (FCF) in FY20.

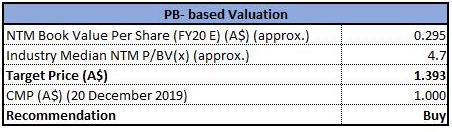

Valuation Methodology: Price to Book Value Based Valuation

P/B Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:RB Group is progressing well in the areas of strategic investment, which are critical for long-term marketplace growth as well as profitability. In addition, RB Group is focused on executing throughout its four strategic initiatives as well as delivering on opportunities to propel the flywheel. We have valued the stock using one relative valuation method, i.e., Price to Book Value method and arrived at the target price of a double-digit upside (in percentage terms). Thus, in the light of decent performance in the recent past, and valuation, we give a “Buy” recommendation on the stock at the current market price of A$1.000 per share, up 1.523% on 20th December 2019.

Cash Converters International

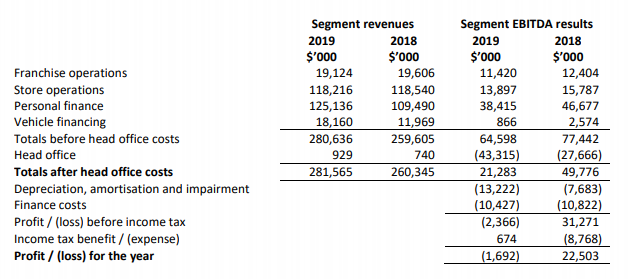

A Look on FY19 Performance:Cash Converters International (ASX: CCV) is a franchisor of second-hand goods and financial services stores and is a provider of secured and unsecured loans. The market capitalisation of the company stood at A$135.62 Mn as on 20th December 2019. The company recently announced that Mitsubishi UFJ Financial Group, Inc. has made a change to substantial holdings in the company and the current voting power stands at 7.91% as compared to the previous voting power of 6.84%. During FY19, the company recorded a statutory net loss after tax amounting to $1.692 Mn against a profit of $22.503 Mn in the previous year.

Financial Summary (Source: Company Reports)

Well-Positioned for Growth:CCV is placed well for future growth and profitability with the continued investment in its proprietary technology and store network. The company stands in a good position when it comes to second-hand goods retailing, pawnbroking and short-term unsecured lending in Australia. The company would further leverage that scale with both its physical store presence as well as online capabilities.

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Valuation Multiple (Source: Thomson Reuters), NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation:Gross margin and EBITDA margin of the company stood at 55.6% and 13.8% in FY19 as compared to the industry median of 24.2% and 6.9%, respectively. Current ratio of the company stood at 2.24x in FY19 against the industry median of 1.26x. This implies that the company is in a decent position to address its short-term obligations as compared to the broader industry. We have valued the stock using one relative valuation method, i.e., EV to Sales Multiple approach and arrived at a target price of double-digit upside (in % terms). Thus, in light of decent margins and liquidity management, valuation and market position, and trading levels, we give a “Hold” recommendation on the stock at the current market price of A$0.230 per share, up 4.545% on 20th December 2019.

.JPG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...