Woodside Petroleum Limited

Woodside’s improved performance with the bottoming of scrip price: Woodside Petroleum Limited (ASX: WPL) is based out in Perth, Australia with offices all over the world. WPL is engaged in the exploration and production of oil and gas. It is one of the largest independent oil and gas company in Australia.

Today, the company has announced that it has entered into a contract with Bechtel Pty Ltd, global engineering, construction, and project management company, to undertake front-end engineering design (FEED) for the Pluto Train 2 Project.

The Pluto Train 2 Project will form the basis of Woodside’s preferred concept for the development of the 7.3 Tcf (2C, 100%) Scarborough gas resource (Woodside 75%). The project will include a second LNG train at the Pluto site with a targeted capacity of 5 Mtpa and installation of domestic gas infrastructure. Woodside is targeting final investment decision (FID) for the Pluto Train 2 Project in 2020 and ready for start-up in 2024.

The company will be declaring its fourth-quarter results on 17 January 2019 with its full-year FY18 performance on 14 February 2018.

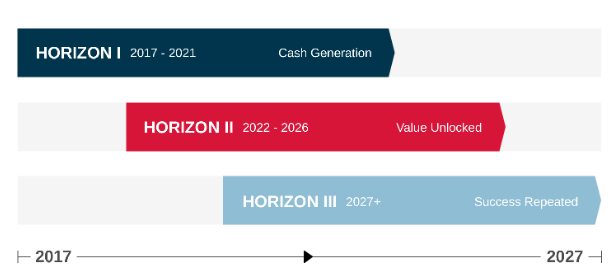

WPL’s Roadmap (Source: Company Reports)

Financial highlights: As per the financial updated of 3Q FY18 reported by the company on 18 October 2018, it achieved sales revenue of $1.157 billion which was 25.4% higher than 3Q FY17 revenue on account of increased production volumes along with higher prices realized. The LNG production increased by 13.8% on a q-o-q basis to 23.1 MMboe which was driven by Wheatstone. The company paid an interim dividend of US 53 cents per share on 20 September 2018, which was 20% higher than 1H 2017. WPL delivered the 5,000th North West Shelf Project LNG cargo and achieved 99% reliability at the Nganhurra FPSO (Enfield oil). It increased its 2018 production guidance from 85-90 MMboe to 87-91 MMboe and Pluto LNG capacity to 4.9 Mtpa and is expected to achieve a total sales revenue of around $5 billion.

The company reported a dividend yield of 4.54% with a P/E ratio of 18.83x which shows that investors are expecting higher earnings growth in the future.

The company has around 936.15 million shares outstanding with the market cap of $27.92 billion and a beta of 0.91x (5-year Monthly basis).

Meanwhile, the stock price has fallen 19.54% in the past three months as on December 24, 2018 and is trading close to lower level. On 24 December 2018, the scrip price was lying on the lower band of the Bollinger band with an oversold position reflected by the Relative Strength Index. But following today’s news, the price surged by 4.16% moving to $31.06 with today’s high price of $31.19. Based on the growth in earnings and the updated earnings guidance for FY18 along with the bottoming of scrip price and a bullish sign indicated by the charts, we maintain our “Buy” recommendation on the stock at the current market price of $31.06.

Origin Energy Limited

Improving Financials: Origin Energy Limited (ASX: ORG) is an Australian based oil and gas company which is into the exploration, production, generation and the sale of energy to households and businesses across Australia. It provides a range of renewable energy options like wind and solar to its clients and also generates electricity through coal, natural gas, wind, and sun. The company is further looking for natural gas reserves to develop as a future energy source.

Financial performance: In Fy18, the company generated 15.9 TWH output up by 14% at Eraring. APLNG production was reported at 676 PJ up by 11%. ORG reported total revenue of $14,604 million in FY18 with a growth of 7% on a y-o-y basis with a net profit of $218 million (against loss of $2,226 million in FY17) and underlying profit from continuing operations of 838 million which was up by 110% versus FY17. The underlying ROCE from continuing operations was reported at 8.4% which was up by 3% versus FY17. The adjusted net debt improved and went down to $1.6 billion in FY18 from 6.5 billion in FY17. Net cash flow from operating and investing activities also grew by 92% moving up to $2.645 billion. Net proceeds from assets sale were reported at $1.5 billion, and energy market natural gas sale was 13% up moving to 281 PJ.

The company reported its EBITDA margin (8.9%), Operating margin (3.8%), and Net margin (1.9%) below the industry median of 31.9%, 22.1%, and 13.2% respectively. Although, the company was able to generate better revenue from its assets as compared to the industry which can be seen from the asset turnover ratio of 0.59x for the company as compared to 0.43x of the industry.

Financial Metric (Source: Company Reports)

During 2018 (YTD), the scrip price has fallen by 35.06% from $9.44 at the beginning of the year to $6.13 as on December 24, 2018. Although the price is in downtrend from the past 6 months, the scrip price has soared by 4.4% today. The price was lying on the lower band of the Bollinger band until 24 December 2018 with the RSI indicating an oversold condition. This reflected a bullish sign due to which the price went up by 4.4%. The scrip is making new lows on a regular basis. Although it can be seen that the financials of the company are improving, the bottoming of prices and new lows were made on a regular basis. Hence, we maintain our “hold” recommendation on the stock at the current price level of $6.4 until a new support level is visible by the chart.

Oil Search Limited

Oil Search making a new support level: Oil Search Limited (ASX: OSH), an oil and gas company headquartered in Papua New Guinea with other offices located in Sydney, Anchorage, and Abu Dhabi, holds 29% interest in the PNG LNG Project. Being an outperformer since 2014, the company achieved an average production rate of 8.3 million tonnes per annum (MTPA) last year which was above its capacity of 6.9 MTPA.

On 20 December 2018, the company announced that it has started with the 2018/19 two-well, two-rig appraisal drilling programme on the Pikka Unit in November. The drilling at Pikka B and Pikka C will commence from early January 2019 and mid-late January 2019 respectively.

Financial performance: As per the latest quarterly updates, the total production was reported at 7.53 million barrels of oil equivalent (mmboe) with a 39% increase from the previous quarter. The total sales and revenue were also up by 60% and 81% respectively. During the third quarter of FY18, the company achieved an annualized production rate of 8.9 MTPA, and 9.0 MTPA for the September month. These were the highest rates reported till date. The total revenue reported at US$474.9 million is the highest since the fourth quarter of 2014. The growth was led by an increase in LNG and gas sales by 68% and liquids sales by 31%. Also, the company realized higher LNG and gas prices by 18% and oil and condensate prices by 5%. The company also reported higher liquidity of US$1.44 billion (up by US$180 million).

After the recovery from the earthquake, the excellent performance from PNG LNG project, the company estimates the full year 2018 guidance of total production to lie in the range of 25-26 mmboe sq. as per the previous guidance of 24-26 mmboe sq. The company also estimates its production cost to lie between US$ 11.5-12.5 per boe and the capital cost to go down US$ 425-475 million which was earlier expected to be around US$ 435-530 million. The company is also expected to spud two wells in January and March 2019.

2018 Candlestick Chart (Source: ASX)

Meanwhile, the stock has generated a negative YTD return of 11.67% and trading at the lower level. On the technical analysis front, the stock price has breached its support level of around AU$7.00, and the Relative Strength Index also seems to be in a neutral state with the price reaching towards the middle of the Bollinger band. With the bottoming of the prices and better performance for the previous quarter and better earnings guidance, we maintain our “Buy” recommendation on the stock at the current market price of $7.100.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...