Stocks’ Details

Pilbara Minerals Limited

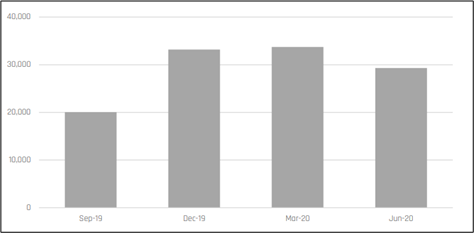

A Look at June 2020 Quarter: Pilbara Minerals Limited (ASX: PLS) is engaged in the exploration of lithium and tantalum. The market capitalisation of the company stood at $856.52 million as on 12th August 2020. Recently, the company released its activities report of June 2020 quarter, wherein, it reported spodumene concentrate production of 34,484 dry metric tonnes (dmt) and shipped 29,312 dmt of spodumene concentrate. Following the introduction of post-COVID-19 stimulus packages as well as incentives by various governments for the electric vehicle (EV) and renewable energy sectors, the company is optimistic about lithium market sentiment. During the quarter, PLS continued to implement control measures to ensure the safety of its people in line with government directives to support the community response to COVID-19.

Quarterly Spodumene Concentrate Shipments (Source: Company Reports)

Future Focus: PLS is focused on expansion and diversification strategy to become one of the biggest and low-cost lithium producers, as well as a fully integrated lithium raw materials and chemicals supplier in the future.

Key Risks: The company’s business activities are exposed to several financial risks, such as credit risk, liquidity risk, market risk and interest risk. To manage these financial risks, PLS ensures enough net cash flows to meet all its financial commitments.

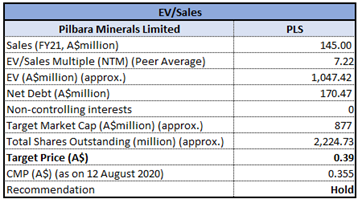

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Approach (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During the June quarter, the company secured new low-cost US$110 million senior debt facility with BNP Paribas and Clean Energy Finance Corporation to replace existing Nordic Bond facility. This debt facility is likely to improve cash-flow, materially reduce funding costs and places the company in a decent position to capitalise on the expected future growth in lithium raw materials demand. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method and have arrived at a target price offering an upside of low double-digit (in percentage terms). For the said purposes, we have considered Galaxy Resources Ltd (ASX: GXY), Mineral Resources Ltd (ASX: MIN) and Orocobre Ltd (ASX: ORE), as peers. Thus, considering the positive sentiment for lithium market, new debt facility and future focus, we give a “Hold” recommendation on the stock at the current market price of $0.355 per share, down by 7.792% on 12th August 2020.

Galaxy Resources Limited

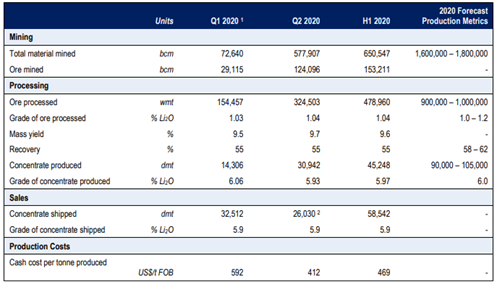

Traka Secures the Mt Cattlin Gold Project: Galaxy Resources Limited (ASX: GXY) is primarily engaged in the production of lithium concentrate. The market capitalisation of the company stood at $505.71 million as on 12th August 2020. Recently, the company noted that Traka Resources Limited has secured rights to the advanced Mt Cattlin Gold Project by agreeing with GXY to exchange its free carried 20% interest in the Mt Cattlin North Tenements for 100% of the gold and other mineral potential. During Q2 FY20, the company reported production volume of 30,942 dry metric tonnes from Mt Cattlin. The company shipped 26,030 dmt of spodumene concentrate, which brought 1H FY20 shipments to 58,542 dmt.

Key Metrics (Source: Company Reports)

Update on Sal de Vida Project: GXY stated that Front-end engineering design of the wellfield and ponds is ongoing, and the process plant package is out for tender. The company stands in a strong position to execute its growth strategy countercyclically and to address the expected rise in lithium demand.

Guidance: For Q3 FY20, the company is likely to report lithium concentrate production in the range of 26,000 - 31,000 dmt.

Key Risks: GXY’s business is sensitive to risks related to additional funding requirements, metal prices, exploration, development and operating risks, competition, production risks, regulatory restrictions, including environmental regulation and liability and potential title disputes.

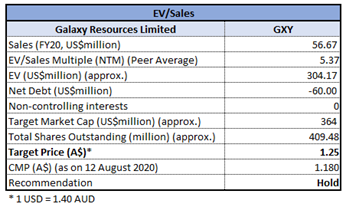

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Current ratio of the company stood at 3.40x in FY19 as compared to the industry median of 1.75x. This reflects that GXY is in a decent position to address its short-term obligations against the peer group. We have valued the stock using the EV/Sales multiple based illustrative relative valuation method and have arrived at a target price offering an upside of high single-digit (in percentage terms). For the said purposes, we have considered Altura Mining Ltd (ASX: AJM), Mineral Resources Ltd (ASX: MIN) and Orocobre Ltd (ASX: ORE), as peers. Thus, in light of the decent liquidity position, performance in Q2 FY20 and the anticipated rise in lithium demand, we give a “Hold” recommendation on the stock at the current market price of $1.180 per share, down by 4.453% on 12th August 2020.

Lithium Australia NL

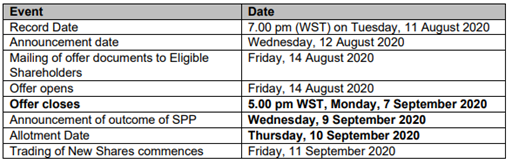

Equity Raising for Future Growth: Lithium Australia NL (ASX: LIT) is engaged in the exploration of lithium and other minerals. The market capitalisation of the company stood at $41.64 million as on 12th August 2020. Recently, the company announced that it has raised $4 million through a placement to institutions and sophisticated and professional investors via the issue of 75,471,698 fully paid ordinary shares at $0.053 per share. In addition, the company has launched a share purchase plan to raise an additional $2 million. The company would use the proceeds to ramp up the growth of its subsidiaries Envirostream Australia Pty Ltd (battery recycling) and Soluna Australia Pty Ltd as well as for working capital purposes.

Key Events (Source: Company Reports)

Future Focus: As of now, the company is currently focused on near-term revenue from Soluna Australia Pty Ltd and Envirostream Australia Pty Ltd. In addition, Envirostream is likely to report revenue growth in FY21, mainly due to strengthening commodity prices since March 2020.

Key Risks: The company’s business activities are exposed to a variety of financial risks, such as credit risk and liquidity risk. LIT continuously monitors forecast cash flows in order to manage the liquidity risk.

Stock Recommendation: Current ratio of the company stood at 2.61x in 1H FY20 as compared to the industry median of 1.85x. This reflects that LIT is well-positioned to address its short-term obligations against the broader industry. Debt to equity of the company stood at 0.01x in 1H FY20 against the industry median of 0.16x. On TTM basis, the stock of LIT is trading at a price to book value multiple of 1.6x, which is lower than the industry median (Metals & Mining) of 2.3x. Hence, considering the recent capital raising, decent liquidity position, deleveraged balance sheet and key risks associated with the business, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.059 per share, down by 13.235% on 12th August 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Note: Lithium Australia Ltd (Company) is a client of Kalkine Media Pty Ltd (Kalkine Media), an affiliate of Kalkine. However, under no circumstances have Kalkine or its related entities been, directly or indirectly influenced in making any related insights concerning Company as contained in this report, and no form of compensation is or will be received by Kalkine, Kalkine Media or Kalkine’s other related entities for the publication of this report.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...