.png)

Stocks’ Details

Contact Energy Limited

Classed as an Essential Business by the Government:Contact Energy Limited (ASX: CEN) is one of New Zealand's largest listed companies which supplies electricity, natural gas and LPG products to its customers. Under the new Covid-19 rules announced by the New Zealand Government, Contact Energy is classed as an essential business, which means that the company will continue to deliver its services in New Zealand even at Alert Level 4 restrictions.

Covid-19 Update:As per the company’s update released on 18 March 2020, Contact Energy is not directly affected by the immediate response efforts in relation to the spread of COVID-19 virus, but the company is maintaining a careful watch on the rapidly developing situation.

Highlights of February Month:In the month of February 2020, the company’s customer business recorded mass market electricity and gas sales of 239 GWh with mass market electricity and gas netback of NZD 93.15/MW. For the month, Contracted Wholesale electricity sales, including that sold to the Customer business, totalled 629 GWh, slightly higher than the figures reported in the previous corresponding period (PCP). Over the month, the company generated 730 GWh of Electricity.

.png)

Wholesale Electricity Pricing (Source: Company Reports)

Valuation Methodology: EV/EBITDA Based Valuation

.png)

EV/EBITDA based Valuation(Source: Thomson Reuters), *1NZD = ~0.98 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The company continues to target a credit rating of BBB (net debt / EBITDAF <2.8x). Contact Energy’s new sustainability linked loan facility which was executed in December 2019 is expected to align its capital structure with strategic ESG ambitions. After noting the above points and considering the fact that the company continues to provide its essential services to its customers amidst covid-19 restrictions, we have valued the stock using EV/EBITDA based relative valuation method and arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like APA Group (ASX: APA), Spark Infrastructure Group (ASX: SKI) and AGL Energy Limited (ASX: AGL). Hence, we give a “BUY” recommendation on the stock at a current market price of A$5.320, up by 6.4% on 27th March 2020.

APA Group

Continuous Growth in Distributions and TSR Returns: APA Group (ASX: APA) is Australia's leading natural gas infrastructure business which operates around $21 billion of energy infrastructure asset. Recently, one of the company’s Directors, Debra Goodin acquired 1,179 securities of the company for a total consideration of $9,986.13 via on market trade. For nearly two decades APA’s distributions have increased every year with compound annual growth rate of 17.2%.

.png)

Distribution History (Source: Company Reports)

H1FY20 Highlights:For the half year ended 31 December 2019, the company reported total revenue of $1,077.8 million, up by 6.4% on pcp. Further, the company reported NPAT $175.0 million, up by 11.2% or $17.6 million on pcp. For the half year period, the company declared an interim distribution of 23.0 cents per security, an increase of 7.0% over pcp.

Guidance: For FY20, the company expects its EBITDA to be in between $1,660 million and $1,690 million and net interest expense is expected to settle at the lower end of the range of $505 million to $515 million.For the year, the company expects total distributions per security to be around 50.0 cents.

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:For H1FY20, APA had a net margin of 13.5%, which is higher than the industry median of 11.7%. For the period, the company maintained an Asset to equity ratio of 4.34x which is higher than the industry median of 3.08x. We have valued the stock using EV/Sales Based relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose we have taken peers like AusNet Services Ltd (ASX: AST), Spark Infrastructure Group (ASX: SKI), and Beach Energy Ltd (ASX: BPT). Considering the continuous growth in distribution, its decent guidance, and expected upside in the share price, we give a “Hold” recommendation to the stock at a market price of $9.730 as on 27 March 2020.

Spark Infrastructure Group

Solid Financial Performance in FY19: Spark Infrastructure Group (ASX: SKI) is a leading owner of a diversified portfolio of quality essential service infrastructure with a market cap of around $3.25 billion as at 27 March 2020. For the year ended 31 December 2019, the company reported adjusted EBITDA of $859.1 million, up 3.7% on FY2018, driven by cost efficiencies and growth in both the regulated and unregulated sectors. For the year, the company reported total distribution of 15.0cps which represents a payout of 67% of look through net operating cash flow.

.png)

Adjusted EBITDA Over Last four Years (Source: Company Reports)

Outlook and Guidance:The company’s Bomen Solar Farm is mechanically complete and is expected to commence its commercial operations in Q2 2020. For FY20, the company has provided a distribution guidance of at least 13.5cps comprising 7.0cps attributable to the first half of 2020 and at least 6.5cps attributable to the second half.

Valuation Methodology: Price to Book Value Multiple based Relative Valuation

.png)

Price to Book Value Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation:SKI’s stock is trading near its 52-weeks low price of $1.685, offering investors an opportunity for accumulation. In the second half of FY19, the company had a net margin of 20.9% which is higher than the industry median of 15.2%. For the same period, the company reported ROE of 1.6%. Considering the company’s solid FY19 performance, decent outlook, and guidance, we have valued the stock using price to book based relative valuation method and arrived at a target price of lower double-digit upside (in % terms). For the purpose we have taken peers like AusNet Services Ltd (ASX: APT), AGL Energy (ASX: AGL) and APA group (ASX: APA). Hence, we give a “Buy” recommendation to the stock at the current market price of $1.860, down by 1.587% on 27 March 2020.

AGL Energy Limited

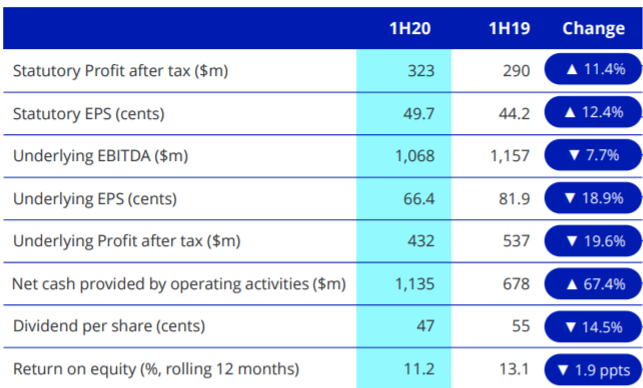

Decent H1FY20 Performance:AGL Energy Limited (ASX: AGL) operates Australia's largest electricity generation portfolio. In the first half of FY20, the company reported Statutory Profit after tax of $323 million, up by 11.4% on pcp, driven by lower negative fair value movement due to lower short-term forward electricity prices. During the period, the company witnessed a decline of 7.7% in its Underlying EBITDA which stood at 1,068 million, due to Loy Yang A Unit 2 outage, higher depreciation and market headwinds as expected. Overall, FY20 is tracking ahead of expectation due to resilient generation performance and broad-based customer growth.

H1FY20 Results Snapshot (Source: Company Reports)

Decent Guidance:For FY20, the company’s underlying profit after tax is expected to be in the upper half of the guidance range of $780 million to $860 million. Cash conversion of the company continues to be strong, underpinning a robust and flexible financial position. The company’s current share buy-back is expected to be accretive to earnings and dividends per share. As per the latest share buy-back notice which was published on 25 March 2020, the company has bought back around 25,713,609 shares for a total consideration of ~$500.44 million.

Covid-19 Update:In the current challenging climate, AGL Energy has continued to provide essential services to millions of Australian homes and businesses. In order to help its customers, the company has extended their payment due dates. Further, the company has placed plans to protect the health and safety of its employees and their families.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuaion

.png)

Price to Earnings Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock is trading close to its 52 weeks low level of $15.150, offering a decent opportunity for accumulation. Considering the decent financial performance in 1HFY20 and FY20 guidance, we have valued the stock using Price to Earnings based relative valuation method and have arrived at a target price of lower double-digit growth (in percentage terms). For the purpose, we have taken peers like Origin Energy Ltd (ASX: ORG), APA Group (ASX: APA), AusNet Services Ltd (ASX: AST) etc. Hence, we give a “Buy” recommendation on the stock at the current market price of $15.930, down by 0.871% on 27 March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...