Stocks’ Details

Viva Energy Group Limited

Strong Commercial Sales: Viva Energy Group Limited (ASX: VEA) is involved in the manufacturing, distribution, and supply of petroleum products to retail and commercial customers. The market capitalisation of the company stood at $2.96 billion as on 16th June 2020. The company recently stated that in the month of May 2020, its weekly sales in the retail Alliance channel stood at 45.1 million litres per week, reflecting a rise of 16.4% over April 2020. Commercial sales ex-aviation were strong and are so far largely unaffected by the COVID-19 related restrictions. VEA is planning to proceed with the major maintenance of the Residual Catalytic Cracking Unit during 2020 at a reduced cost and over an extended timeframe with total capital expenditure of the event anticipated to be between $85 million - 100 million.

May 2020 Performance (Source: Company Reports)

Guidance: For 1H FY20, the company expects the total sales volume to be in the range of 6,100 to 6,200 million litres. In the retail business, the company expects its underlying EBITDA (RC) to be between $325.0 million – $335.0 million.

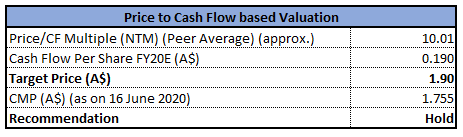

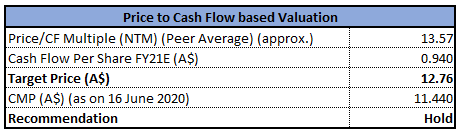

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: Due to measures taken around the world to manage the spread of COVID-19, global refining margins have been impacted by lower demands for oil products, especially jet and gasoline fuels. This position is likely to persist in the remainder of 2020 and possibly into 2021. VEA is exposed to operational and supply chain risks. Disruption to any part of Viva Energy’s supply chain might impact its operations and Total Shareholder Returns.

Stock Recommendation: VEA would continue to develop its refining business improvement program, and work closely with the Government on a strategic review of the sector in order to identify actions that will be necessary to enhance the long-term viability of the refining business. In FY19, the company’s gross margin and EBITDA margin stood at 9.0% and 3.9% in FY19, respectively. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of high single-digit (in percentage terms). For the purpose, we have taken peers like Ampol Ltd (ASX: ALD), Origin Energy Ltd (ASX: ORG), Washington H Soul Pattinson and Company Ltd (ASX: SOL). Therefore, considering the improvement in key margins, strong commercial sales, and rise in weekly sales, we give a “Hold” recommendation on the stock at the current market price of $1.755 per share, up by 15.461% on 16th June 2020.

Infratil Limited

Opening of Share Purchase Plan: Infratil Limited (ASX: IFT) owns and operates businesses in the energy, transport, data infrastructure and social infrastructure sector. The market capitalisation of the company stood at $3.28 billion as on 16th June 2020. The company has recently opened its non-underwritten Share Purchase Plan (SPP) to raise around NZ$50 million. This SPP is a part of equity raising announced on 9 June 2020, whereby the company also completed a fully underwritten NZ$250 million institutional placement. The company would use the proceeds from equity raising to finance growth investments in its existing portfolio companies as well as to take benefit of new opportunities.

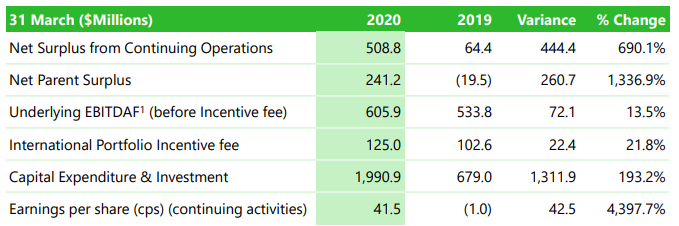

During FY20, the increasing exposure to its preferred sectors of data infrastructure and renewable energy has generated net growth in a year of portfolio changes. Net profit from the continuing operations stood at NZ$508.8 million against NZ$64.4 million in the prior year. The company ended the FY20 with strong capital position and liquidity throughout the group with multiple levers to manage near to medium-term capital commitments.

Key Metrics (Source: Company Reports)

Pipeline of Growth Opportunities: IFT maintains an attractive pipeline of growth opportunities throughout its portfolio and is continuing to evaluate additional opportunities in key growth sectors and new geographies. The company would continue to apply a disciplined approach to allocating capital when assessing potential investments.

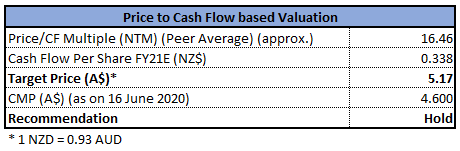

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: Due to its business activities and financial policies, IFT is exposed to credit risk, liquidity risk market risk. Apart from these risks, the business is sensitive to projected generation & electricity price.

Stock Recommendation: The company has a long track record of delivering strong returns to shareholders and maintains a 10-year total shareholders’ return target of 11-15% per annum. Net margin of the company stood at 37.2% in FY20 as compared to the industry median of 17.9%. This reflects that the company has decent capabilities to convert its top-line into the bottom-line against the broader industry. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like Contact Energy Ltd (ASX: CEN), Mercury NZ Ltd (ASX: MCY), Meridian Energy Ltd (ASX: MEZ), etc. Hence, in light of the track record of delivering excellent returns to shareholders, decent capital position and liquidity comfort, we give a “Hold” recommendation on the stock at the current market price of A$4.600 on 16th June 2020.

APA Group

Pricing of Senior Unsecured Notes: APA Group (ASX: APA) operates a leading natural gas infrastructure business in Australia. The market capitalisation of the company stood at $13.2 billion as on 16th June 2020. Recently, the company announced that it has appointed Rhoda Phillippo as an Independent Non-Executive Director, effective from 1st June 2020. Following the shutdown work program, APA has resumed the commissioning of Orbost Gas Processing Plant. Moreover, the supply of Sole gas into the Eastern Gas Pipeline has recommenced.

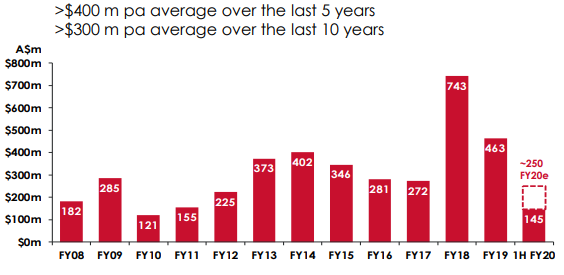

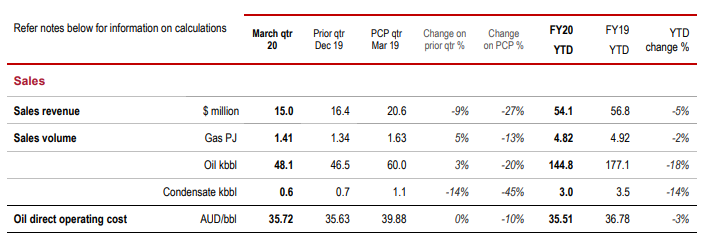

In another update, the company stated that it has priced senior unsecured notes totaling to EUR 600 million in the European debt capital markets with respect to Regulation S under the US Securities Act. The proceeds raised from the notes issue would be utilised for the repayment of the debt, which is maturing in July 2020. APA would also use proceeds for general corporate purposes. The company maintains a track record of growth in capex investment.

Capex Investment (Source: Company Reports)

Distribution Guidance: For 1H FY20, the company expects EBITDA to be in the range of $1,635 million - $1,655 million. APA forecasts to pay a distribution per security of 50.0 cents.

Valuation Methodology:Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Strategic Risk: The company is exposed to risks arising from the industry and geographical environments within which APA operates. This includes markets, customers, brand and reputation, and regulatory policy.

Stock Recommendation: APA maintains strong liquidity with $1.2 billion in cash and committed undrawn facilities as at 31st March 2020. This would support the company in the ongoing funding of the business. We have valued the stock using a P/CF multiple based illustrative relative valuation methodand arrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers like AGL Energy Ltd (ASX: AGL), Mercury NZ Ltd (ASX: MCY), Meridian Energy Ltd (ASX: MEZ), etc. Thus, considering the strong liquidity, recommencement of supply of sole gas and track record of growth in capex investment, we maintain a “Hold” recommendation on the stock at the current market price of $11.440 per share, up by 2.234% on 16th June 2020.

Cooper Energy Limited

Decent Growth in Gas Revenue:Cooper Energy Limited (ASX: COE) is an upstream oil and gas exploration and production company with a market capitalisation of $601.86 million as on 16th June 2020. Recently, the company announced that Pendal Group Limited has ceased to become a substantial holder in the company on 9th June 2020.During the quarter ended 31st March 2020, the company reported quarterly production of 0.28 million boe, reflecting a rise of 0.27 million boe over pcp while the revenue for the quarter went down by 9% to $15.0 million. In the same time span, gas revenue of the company went up by 19% to $13.3 million. COE added that the growth in its gas sales has largely offset the impact of the cut to its oil revenue in the March quarter brought by lower oil prices.

Key Sales Metrics (Source: Company Reports)

Guidance:With respect to the gas market, the company is expecting soft spot prices and demand. For FY20, the company anticipates its capital expenditure to be in the middle of $86 million to $93 million.

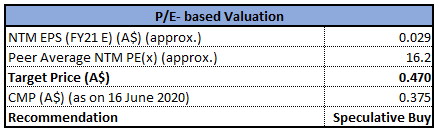

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Key Risk: The expected weakness in demand and spot prices in gas might create a headwind for the business going forward.

Stock Recommendation: As at 31st May 2020, the cash and net debt balance of the company stood at $142.5 million and $84.4 million, respectively. The current ratio of the company stood at 2.70x in 1H FY20 as compared to the industry median of 1.06x. This implies that the company is in a decent position to address its short-term obligations against the peer group. We have valued the stock using the P/E multiple based illustrative relative valuation method andarrived at a target price with an upside of low double-digit (in percentage terms). For the purpose, we have taken peers such as Senex Energy Ltd (ASX: SXY), New Hope Corporation Ltd (ASX: NHC), and Viva Energy Group Ltd (ASX: VEA). Therefore, considering the decent liquidity position, growth in gas sales, and expected weakness in demand and spot prices, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.375 per share, up by 1.351% on 16th June 2020.

.jpg)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...