Stocks’ Details

Hansen Technologies Limited

Performance for 2HFY20 to date in-line with Expectations: Hansen Technologies Limited (ASX: HSN) is involved in the business of providing mission critical software to suppliers of essential services such as energy, water and communications. On 3rd April 2020, the company provided an operating update, wherein, it informed that it has formalised the flexible working arrangements for its staff and is continuing to work on customer projects using long established remote work practices. The recurring revenues the company derives from its customer relationships, provide HSN a solid revenue foundation as it deals with the COVID-19 pandemic. Currently, the company does not expect its recurring revenues to be significantly affected by COVID-19.

Withdrawal of FY20 Earning Guidance: Due to the uncertainty surrounding the potential effects of COVID- 19 on future operations and financial performance, the company has withdrawn its formal earnings guidance for FY20.

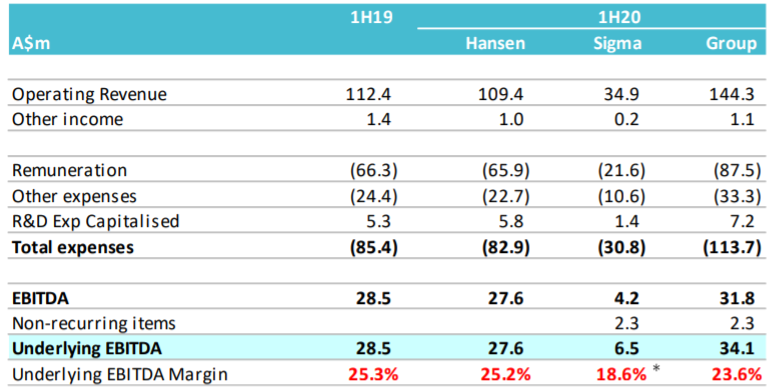

Decent H1FY20 Performance: In the first half of FY20, the company reported a growth of 28% in its revenue to $144.3 million, as compared to pcp. Over the same period, the company’s underlying EBITDA grew by 20% to $34.1 million. For the period, the company declared an interim dividend of 3 cents, partially franked.

Half Year Results Snapshot (Source: Company Reports)

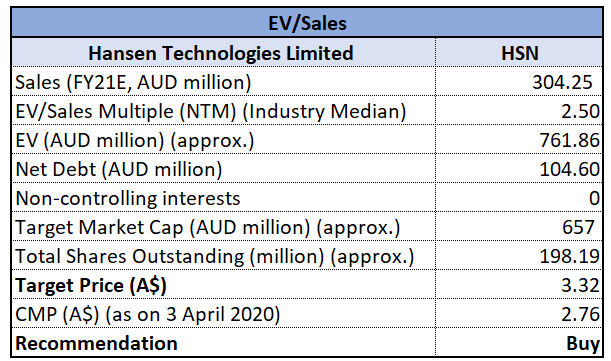

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company continues to have significant funding available to assist with cash flow requirements. HSN stock is currently trading near to its 52 weeks low price of $2.810, offering investors an opportunity for accumulation. We have valued the stock using EV/Sales multiple based relative valuation method and arrived at a target upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like Altium Ltd (ASX: ALU), Bravura Solutions Ltd (ASX: BVS), ELMO Software Ltd (ASX: ELO), etc. Considering the company’s resilient performance during the current challenging climate, decent H1FY20 performance and current trading levels, we are giving a “Buy” recommendation to the stock at a current market price of $2.760, down by 2.817% on 3rd April 2020.

Nanosonics Limited

Underlying growth momentum Continued: Nanosonics Limited (ASX: NAN) is primarily involved in the research, development, and commercialisation of innovative technologies in infection control and decontamination. The company recently provided an update on COVID-19, wherein it informed that its unaudited sales in Q3FY20 have increased significantly, as compared to pcp, reflecting continued underlying growth momentum for the business and a growing awareness and understanding of the importance of ultrasound probe decontamination. The company has assured that it is currently well-positioned to meet customer demand having increased inventory of raw materials and finished goods for capital equipment and consumables.

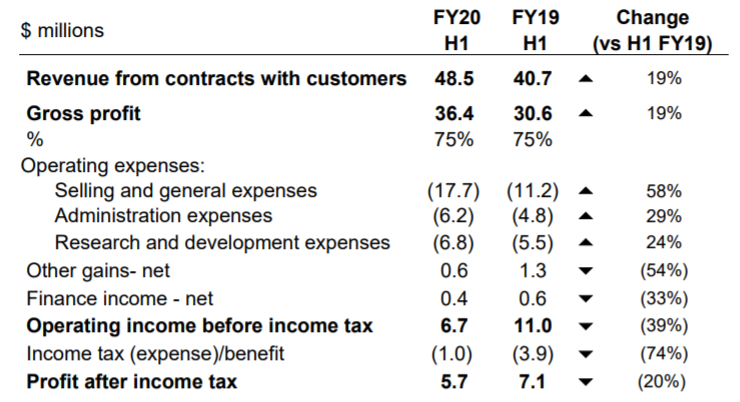

Record sales in H1FY20: In the first half of FY20, the company reported record sales of $48.5 million, up 19% on the prior corresponding period (pcp). For the period, the company reported record operating profit before tax of $6.7 million and free cash flow of $10.0 million.

H1 FY20 Snapshot (Source: Company Reports)

What to expect: The company is taking prudent measures on operating expenses with a likely decrease in Q4 FY20 expenditure. Although the company is currently benefiting from a relatively stronger US dollar, at the current stage, the net impact on revenue and profit for Q4 / FY20 is uncertain.

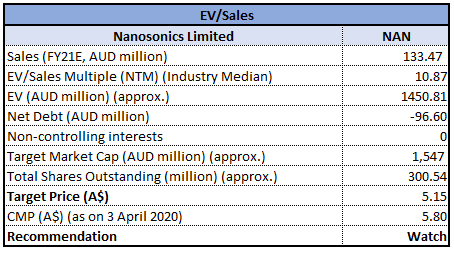

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company is continuing to invest in its stated strategy as fundamentals for business are sound. As at 31 December 2019, the company had a strong balance sheet with cash reserves of $82.0 million and negligible debt. We have valued the stock using the EV/Sales valuation approach and have arrived at a target upside of lower double-digit upside (in percentage terms). For the purpose, we have taken peers like Polynovo Ltd (ASX: PNV), Integral Diagnostics Ltd (ASX: IDX), Mayne Pharma Group Ltd (ASX: MYX), etc. Considering the aforesaid facts and uncertainty surrounding the potential effects of COVID- 19 on future operations, we have a watch stance on the stock at the current market price of $5.80, down by 5.997% on 3rd April 2020.

Wagners Holding Company Limited

Minimal interruption to Australian Operations Due to Covid-19: Wagners Holding Company Limited (ASX: WGN) is an innovative Australian construction materials and services provider which is also an innovative producer of new generation building materials through its composite fibre technologies and earth-friendly concrete businesses. On 3rd April 2020, the company provided an update on Covid-19 and assured that it is taking proactive steps to provide uninterrupted services to all of its clients. The company has experienced minimal interruption to operations in Australia and all of its projects and sites are operating in line with expectations, with some additional costs associated with complying with government and client directions around COVID-19 preventative measures.

International Operations Impacted by Covid-19: The company has informed that its international operations have been impacted due to the travel restrictions and shut-downs throughout USA, UK, Europe and New Zealand. Due to the uncertainty around the COVID-19 impacts and the company’s inability to forecast earnings with any degree of certainty, the company has withdrawn its FY20 earnings guidance.

H1FY20 Results Highlights: In the first half of FY20, the company reported revenue from continuing operations of $122.32 million, down by 1.2% on pcp, due to reduced cement volumes, and no major project work during the period. For the same period, the company reported a net loss of from continuing operations of $1.62 million, down by 112% on pcp, due to dispute with a major customer, delays in higher margin project services based work and the Groups revenue composition shifting, which now includes a greater proportion of lower margin revenue streams such as the Groups contract haulage services.

.png)

Half-year Result Summary (Source: Company Reports)

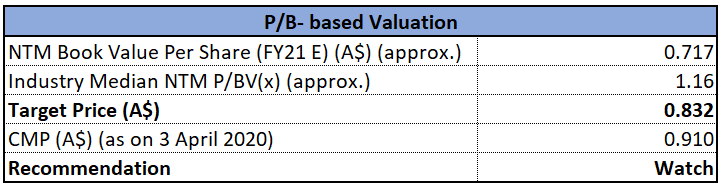

Valuation Methodology: Price to Book Value Multiple based Relative Valuation

Price to Book Value based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: In the past six months, the stock has corrected by 64.34% on ASX. We have valued the stock using a Price to book based relative valuation method and arrived at a target price with a correction of lower-single digit upside (in % terms). For the purpose, we have taken peers like CSR Ltd (ASX: CSR), GWA Group Ltd (ASX: GWA), James Hardie Industries PLC (ASX: JHX), etc., and arrived at a target price which suggests a correction. Considering the aforesaid facts, recent withdrawal of FY20 earnings guidance and uncertainty surrounding Covid-19, we have a watch stance on the stock at the current market price of 0.910, down by 6.186% on 3rd April 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...