Stocks’ Details

WAM Microcap Limited

Robust Growth in Operating Profit: WAM Microcap Limited (ASX: WMI) is a listed investment entity with a market capitalisation of ~$173.06 million as on 3rd July 2020. During the month of May 2020, the company reported an excellent investment portfolio performance of 14.3%, which was contributed by smash repair company AMA Group, fashion retailer City Chic Collective and infant goods retailer Baby Bunting Group. During the month, the company increased its holdings in automotive companies in expectation of a rise in domestic tourism and car usage.

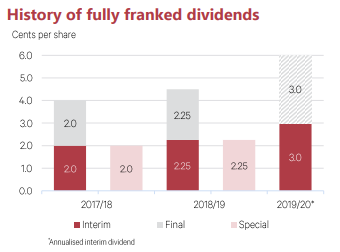

During 1H FY20, the company reported a rise of 311.9% in operating profit before tax to $27.3 million due to strong investment portfolio performance and the growth in assets over the period. Since its inception, the company has paid a dividend of 12.75 cents per share.

Dividend History (Source: Company Reports)

Key Risks: As of now, the company’s risks involve a rise in US-China trade tension, the second wave of coronavirus, the shape of economic recovery and the heightened valuations occurring in the market.

Stock Recommendation: During 1H FY20, the company has provided shareholders with a return of 23.0%. This indicates robust investment portfolio performance as well as the rise in the share price relative to the NTA. The company is focused on the most exciting undervalued growth opportunities in the Australian mid-cap market. The stock of WMI has provided a return of 15.09% during the span of three months. The stock of WMI is trading at a P/E multiple of 4.89x as compared to the industry median (Investment Banking & Investment Services) of 10.3x on TTM basis. Therefore, considering the robust investment portfolio performance in May 2020, rise in operating profit and consistent dividend history, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.230 per share, up by 0.82% on 3rd July 2020.

WAM Leaders Limited

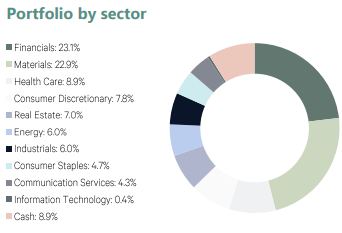

Decent Growth in Portfolio: WAM Leaders Limited (ASX: WLE) is a listed investment entity, managed by Wilson Asset Management Group. The market capitalisation of the company stood at ~$841.8 million as on 3rd July 2020. In the month of May 2020, the investment portfolio performance of the company stood at 9.8%, which was supported by miners, financial institutions, retail travel agency, Flight Centre Travel Group, and airline Qantas Airways. At the end of May 2020, gross assets of the company stood at $922.1 million with listed equities of $839.7 million. During 1H FY20, the investment portfolio witnessed a growth of 6.6%. Moreover, the portfolio outperformed the S&P/ASX 200 Accumulation Index by 3.5%.

Portfolio by Sector (Source: Company Reports)

Key Risks: The company is exposed to various risks pertaining to the second wave of coronavirus, rising trade tension between the US and China as well as the heightened valuation in the market.

Stock Recommendation: During the half-year 2020, the company has provided a return of 13.6%. The company is focused on investing in high-quality Australian companies. Return on equity of the company stood at 4.5% in 1H FY20, reflecting a YoY growth of 9.8%. During the last three months, the stock of WLE has provided a return of 8.63%. Thus, considering the outperformance of portfolio, decent return to shareholders and key risks stated above, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.080 per share, up by 0.935% on 3rd July 2020.

Contango Income Generator Limited

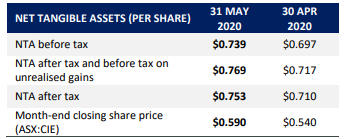

Strong Portfolio Performance: Contango Income Generator Limited (ASX: CIE) invests into companies listed on the Australian Securities Exchange (ASX) that are outside the top 30 companies by market capitalization and are expected to deliver a sustainable tax effective dividend stream at the time of their purchase. The market capitalisation of the company stood at ~$68.79 million as on 3rd July 2020. In the month of May 2020, the investment portfolio of the company has returned 7.42%. Portfolio performance was supported by Breville Group, Charter Hall Group and Appen. Strong performance for the month was derived from a recovery in most of the oversold stocks in the portfolio and new growth stocks. CIE declared a fully franked quarterly dividend amounting to 0.96 cents per share in May. The NTA before tax as on May 2020 was recorded at $0.739 per share, an increase of ~6% in NTA before tax from $0.697 as on April 2020.

Net Tangible Assets (Source: Company Reports)

Outlook: In the past period, the performance of the company was supported by the broadening of the rally. Going forward, the company would continue to monitor the growth of the COVID-19 around the world and the trend of economic data.

Key Risks: CIE’s business is exposed to numerous financial risks: market risk (including price risk and interest rate risk), credit risk, liquidity risk. Market risk is associated with the fluctuation in fair value or future cash flows of a financial instrument due to changes in market price.

Stock Recommendation: Over the past 12 months to 31st May 2020, the company has paid a dividend yield of 5.18%, or 7.11%, including franking credit. The portfolio of the company is characterised by strong and diverse companies that exhibited good cash flows and business models. During the last one and three months, the stock of CIE has provided returns of 10.08% and 21.30%, respectively. Hence, considering the decent portfolio performance during May 2020, strong & diverse portfolio of companies that exhibit good cash flows & business model, and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.640 per share down by 2.29% on 3rd July 2020.

Pinnacle Investment Management Group Limited

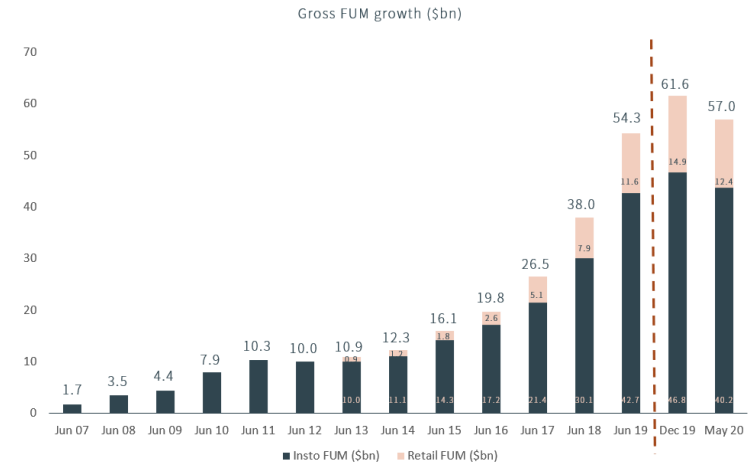

Impact of COVID-19 on FUM: Pinnacle Investment Management Group Limited (ASX: PNI) is engaged in the funds management business. The market capitalisation of the company stood at ~$751.74 Mn as on 3rd July 2020. Recently, the company stated that it has experienced a large impact of the COVID-19 crisis on the market value of FUM. As on 31st May 2020, total affiliate FUM stood at $57.0 billion against $61.6 billion at 31 December 2019 and $54.3 billion at 30 June 2019. During 1H FY20, net profit after tax from continuing operations amounted to $13.8 million, reflecting a rise of 37% from $10.1 million in the prior corresponding period (PCP).

FUM Growth (Source: Company Reports)

Future Growth of PNI: The company is well-positioned to deliver superior business and financial performance in the medium term. PNI’s future focus involves investment in the distribution platform and quickly meet the evolving needs of its clients.

Valuation Methodology: P/BV Multiple Based Relative Valuation (Illustrative)

P/BV Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Key Risks: PNI’s activities are sensitive to equity market conditions and regulatory risk. The company’s business is likely to be impacted by any disruption in the equity market.

Stock Recommendation: The company possesses a strong and flexible balance sheet. PNI had a debt facility of $30 million from CBA, which is fully drawn down in December 2019, to acquire 25% interest in CCI. Current ratio of the company stood at 6.33x in 1H FY20 as compared to the industry median of 1.38x. This reflects that the company is in a decent position to address its short-term obligations against the broader industry. We have valued the stock using Price to Book Value multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers such as Pendal Group Ltd (ASX: PDL), Perpetual Ltd (ASX: PPT) HUB24 Ltd (ASX: HUB), etc. Thus, considering the growth in NPAT, strong and flexible balance sheet and decent liquidity position, we give a “Buy” recommendation on the stock at the current market price of $3.930 per share, down by 2.723% on 3rd July 2020.

Comparative Price Chart(Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...