.png)

Stocks’ Details

BHP Group Limited

Stable Operating Performance: BHP Group Limited (ASX: BHP) is primarily involved in the exploration, production and processing of minerals. The market capitalisation of the company stood at $86.17 Bn as on 11th March 2020. The stable operating performance of the company can be seen in the underlying attributable profit which amounted to US$5.2 billion for 1H FY20. As a result of operational stability, favourable exchange rate movements and higher iron ore prices, BHP reported profit from operations of US$8.3 billion in 1HFY20.

On the back of decent cash flow, the Board of the company declared an interim dividend amounting to 65 US cents per share. The below picture gives an idea of currency exchange rates applicable for the dividend:

.png)

Currency Exchange Rates (Source: Company Reports)

Positive Outlook for Commodities: BHP is optimistic about the underlying fundamentals of its commodities even with near-term uncertainty. The company is focused on advancing its exploration programs in petroleum and copper, with the third phase of the drilling program at Oak Dam in South Australia in progress. This program is forecasted to be completed in the June 2020 quarter.

Valuation Methodology: P/E Multiple Based Relative Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: For 1HFY20, net operating cash flows stood at US$7.4 billion, demonstrating decent iron ore prices as well as decent operating performance. We have valued the stock using P/E based relative valuation method, and for the purpose, we have taken peers such as Rio Tinto Ltd (ASX: RIO), Fortescue Metals Group Ltd (ASX: FMG), South32 Ltd (ASX: S32), etc., and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering strong cash flows, focus on petroleum exploration and record dividend paid to shareholders, we give a “Buy” recommendation on the stock at the current market price of $28.520 per share, down by 2.496% on 11th March 2020.

Orocobre Limited

Improvement in Operational Performance: Orocobre Limited (ASX: ORE) is in the exploration and production of minerals along with a major focus on the development of potash and lithium resources in Argentina. Despite the softer conditions in the market, the company managed to deliver positive operating margins during 1HFY20. Total production for the period stood at 6,679 tonnes of lithium carbonate, which reflects a rise of 10% on pcp.

The company received positive results from the Olaroz Lithium Facility with the revenue amounting to US$39.4 million from the sale of 6,395 tonnes of lithium carbonate.

.png)

Production and Price (Source: Company Reports)

Production Guidance for FY20: With respect to Olaroz Lithium Facility, the company anticipates production for FY20 to be at least 5% higher as compared to FY19. ORE forecasts the average sales price of around US$5,000 per tonne for the March 2020 quarter.

Stock Recommendation: Current ratio of the company stood at 2.60x in 1HFY20 against the industry median of 1.70x. This reflects that ORE is in a decent position to address its short-term obligation as compared to the peer group. The stock of Orocobre is trading at a price to book multiple of 0.7x against 1.3x of industry median (Basic Materials) on TTM basis. Therefore, in light of decent liquidity position and positive operating margins, we give a “Buy” recommendation on the stock at the current market price of $2.260 per share, down by 8.871% on 11th March 2020.

Pilbara Minerals Limited

Weaker Market Conditions During 1H FY20: Pilbara Minerals Limited (ASX: PLS) is a lithium and tantalum exploration company with a market capitalisation of $511.45 Mn as on 11th March 2020. During 1H FY20, PLS experienced weaker market conditions in China and low customer demand for lithium raw materials. This is currently impacting spodumene exports from Western Australia and prices received throughout the entire lithium raw materials and chemicals product suite and resulted in lower production of spodumene concentrate of 36,033 dmt.

.png)

Financial Overview (Source: Company Reports)

Focus for Upcoming Years: In order to ensure cautious management of its operating cash flows, balance sheet as well as its working capital position, the company would continue to operate under a moderated production strategy during 2HFY20.

Valuation Methodology: P/BV Multiple Based Relative Valuation

.png)

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In order to cement the balance sheet, the company has wrapped up the equity raising of $111.5 million during 1HFY20. The company ended the half year with the cash balance of $105.5 million along with the working capital of $94.8 million. We have valued the stock using P/BV based relative valuation method, and for the purpose, we have taken peers such as Orocobre Ltd (ASX: ORE), Western Areas Ltd (ASX: WSA), South32 Ltd (ASX: S32), etc., and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering the recent fund raising, focus for the years ahead and valuation, we give a “Speculative buy” recommendation on the stock at the current market price of $0.200 per share, down by 13.043% on 11th March 2020.

NRW Holdings Limited

Acquisition of BGC Contracting: NRW Holdings Limited (ASX: NWH) is engaged in the provisioning of services, which primarily include civil contracting, mining services, etc. The market capitalisation of the company stood at $840.57 Mn as on 11th March 2020. The first half of the financial year 2020 has been proved another period of growth in terms of revenue and earnings throughout all parts of the business and reported revenue amounting to $808.7 million with a rise of 55% over pcp. During December 2019, NRW completed the acquisition of BGC contracting for the total consideration of $270.1 million. NWH declared a fully franked interim dividend of 2.5 cents per share in order to please the shareholders.

.png)

Earnings (Source: Company Reports)

Expected Contribution in 2H FY20: NRW Holdings Limited is expecting a significant contribution from the acquisition of BGC contracting in the second half of FY20. The company is positioned to capitalise on the positive market conditions in public infrastructure delivery in WA.

Valuation Methodology: P/E Multiple Based Relative Valuation

.png)

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: During 1H FY20, it has procured new Civil contracts with the worth of $70 million for BHP Mitsubishi Alliance at Blackwater and Goonyella. It possesses current order book amounting to $3.8 billion. We have valued the stock using P/E-based relative valuation approach, and for the purpose, we have taken peers such as Perenti Global Ltd (ASX: PRN), Emeco Holdings Ltd (ASX: EHL), Macmahon Holdings Ltd (ASX: MAH), etc., and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Hence, considering the current order book and the recent acquisition of BGC contracting, we give a “Buy” recommendation on the stock at the current market price of $1.740 per share, down by 11.675% on 11th March 2020.

Regis Resources Limited

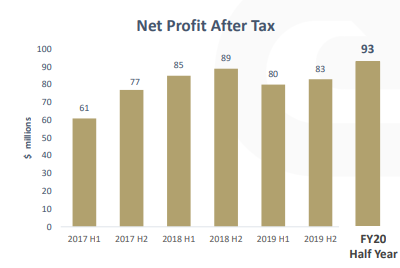

Robust Net Profit Margin: Regis Resources Limited (ASX: RRL) is in the exploration of gold and minerals with a market capitalisation of $2.06 Bn as on 11th March 2020. Recently, it has appointed Russell Barwick for the role of independent Non-Executive Director. For the 1H FY20, the company reported net profit after tax amounting to $93.4 million and net profit margin of 25%, representing the reliability and quality of the operations at Duketon. The robust net profit margin has helped the company to undertake significant capital investment towards the development of the Rosemont underground as well as new satellite deposits at Dogbolter-Coopers, Baneygo and Petra.

Net Profit after Tax (Source: Company Reports)

Production Guidance for Duketon: The company expects annual production in the range of 340,000 ounces -370,000 ounces with all-in sustaining costs expected to be at the upper end of annual cost guidance of $1,125-$1,195 per ounce for Duketon operations.

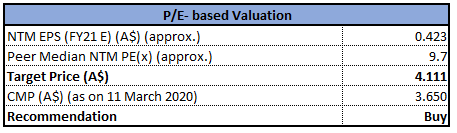

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Net margin of the company stood at 25.1% in 1HFY20 as compared to the industry median of 14.3%. This reflects that RRL is in a decent position to convert its top-line into the bottom-line against the peer group. We have valued the stock using P/E-based relative valuation method, and for the purpose, we have taken peers such as IGO Ltd (ASX: IGO), Western Areas Ltd (ASX: WSA), St Barbara Ltd (ASX: S32), etc., and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Therefore, considering strong net margins, performance at Duketon operations and guidance for FY20, we give a “Buy” recommendation on the stock at the current market price of $3.650 per share, down by 9.877% on 11th March 2020.

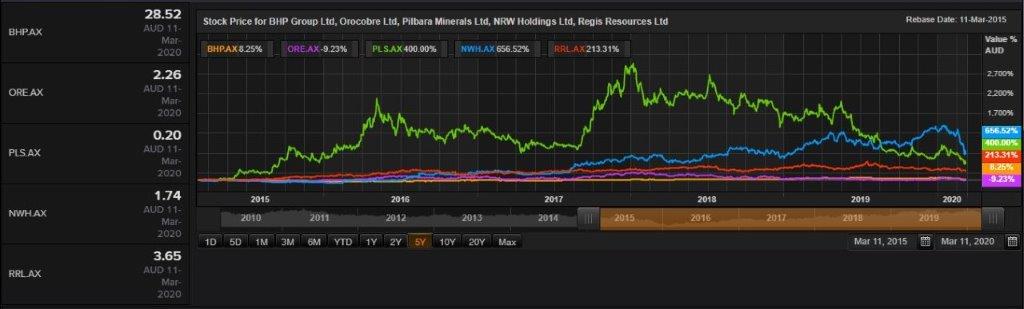

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...