The shares of Bendigo and Adelaide Bank Ltd (ASX: BEN) have been under pressure since its first half of 2015 results, falling over 9.5% till date, (from 16

th Feb to July 22

nd). However, we believe that the bank delivered a modest performance during the first half of 2015.

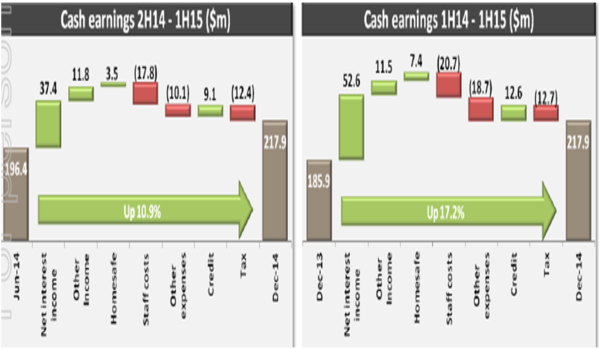

The cash earnings rose 17.2% yoy to $217.9 million in the first half of 2015, driven by the net interest income and homesafe portfolio. The statutory net profit after tax surged 25.8% yoy to $227.3 million, as the group derived benefit from tax issue finalization and Cuscal investment. Cash earnings per share improved to 48.1 cents, against 45 cents in the first half of 2014. The group declared a fully franked interim dividend of 33 cents during the period, as compared to 31 cents in first half of 2014. Meanwhile, the bank maintained its dividend payout ratio at 69%, as compared to 1H14.

Cash earnings performance (Source: Company Reports)

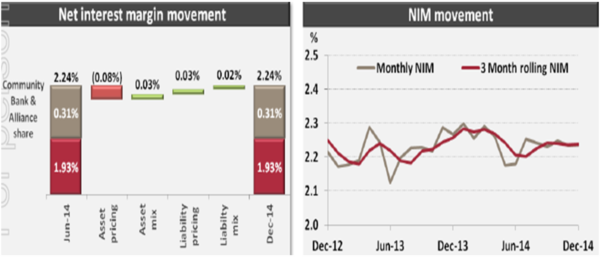

Meanwhile, the bank’s net interest margin remained flat at 2.24%, partly affected by 8 bps on the back of mounting lending competition. On the other hand, over 3 bps positive contribution came from the asset mix, driven by RFC acquisition. The second half of 2015 is expected to include costs of committed liquidity facility and rising HQLA holdings for Basel III.

Net interest margins performance (Source: Company Reports)

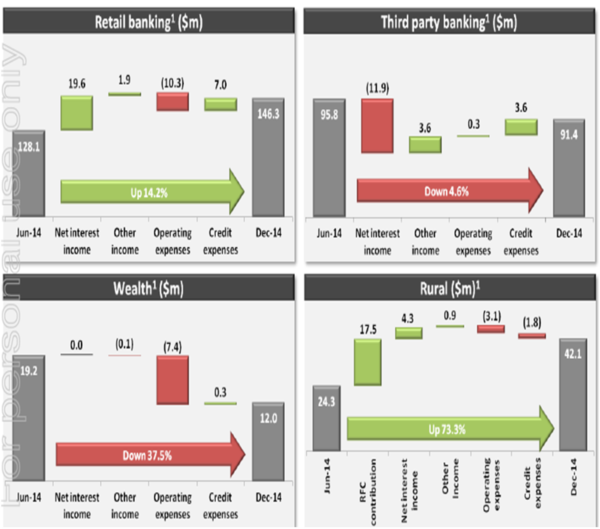

As per the segment highlights, the retail banking improved 14.2% to $146.3 million in the first half of 2015, despite highly competitive lending market, driven by increase over $19.6 million of net interest income (NII). The increase in NII was mainly due to growth of at-call funds and pricing of term deposits. The bank has achieved decent consumer and business satisfaction ratings, while intends to continue its focus on customer strategy. BEN launched EasySaver deposit on October 2014. On the other hand, the third party banking business declined 4.6% yoy to 91.4 million, impacted by the net interest income decrease of $11.9 million. Meanwhile, the bank’s investments in upgrading the third party lending systems is showing benefits while the funding facilities approved for 17 credit unions. The wealth segment plunged 37.5% yoy to $12 million, due to decrease of $7.4 million of operating expenses. But the margin lending portfolio has stabilized and the smart start super showed solid increase of 36% during the first half. The rural business surged 73.3% yoy to $42.1 million driven by RFC contribution of $17.5 million, in line with expectations. Meanwhile, the efforts of the rural non-performing loans decrease have been ongoing and the business is well positioned to deliver growth.

Segment performance (Source: Company Reports)

The bank delivered a return on average tangible equity of 13.39%, as compared to 13.38% in the period ended on June 2014, and 13.3% in the first half of 2014. Meanwhile, the return on average ordinary equity improved 9.16%, against 8.83% in the corresponding period of last year. The bank reported improved Basel III CET1 ratio which rose by 12 basis points to 8.14%. The total capital surged by 80bps to 12.19%, with $292 million of additional tier 1 capital issued in October. Over $600 million RMBS has offered capital and funding benefit. Meanwhile, the great southern settlement agreement was approved by the supreme court of Victoria. Post approval in December, over 300 customers chose to repay in excess of $20 million overdue loans. The bank reported arrears of $311.4 million, while the specific and collective provisions were $9.8 million and $11.8 million respectively.

Current loan size distribution and obligor exposure (Source: Company Reports)

The amortization of back book affected net growth, witnessing a 20% yoy increase in excess repayments during the period. The bank’s residential mortgages have performed well during the first half, while the loan growth declined to $502 million in 1H15 from 1,095 due to seasonality impact. The residential loan approvals improved to $5,239 million during the first half of 2015, as compared to $5,098 million in last year’s corresponding period, but reduced as compared to $5,424 million during the period ended on June-14.

Bendigo and Adelaide Bank raised over $282 million capital by offering Convertible preference shares 3 (CPS3) to further build its balance sheet. Over 2.82 million of CPS3 was issued at an issue price of $100 per CPS3.

Outlook

Bendigo and Adelaide Bank shares have hit a five year high of $14.45 during February, but could not sustain these levels. Moreover, the challenging banking sector coupled with uncertainty of proposed changes from RBA or APRA can further impact the stock. With the bank’s results due next month, we recommend investors to be cautious on the stock as we believe that the Bendigo and Adelaide Bank is “Expensive” at its current levels of $13.02, and would review the stock later.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...