With the rising oil price scenario, some ASX listed energy players have taken a front foot and the environment across the globe signifies that the energy sector is becoming defensive in a gradual manner. Whether this picture is going to stay in long term or not is still a question, below are four energy players that have yielded good returns in this year to date.

Woodside Petroleum Limited

.png)

WPL Details

Expects Moderate Rise in production for 2HFY18: Woodside Petroleum Limited’s (ASX: WPL) first quarter result for the period ended 31 March 2018 showcased higher quarter on quarter (Q-o-Q) production of 22.2 MMboe and sales revenue of $1,169 Mn (up by 18% on Q-o-Q basis). The company also highlighted that the Train 1 at Wheatstone LNG achieved steady production and demonstrated production rates above nameplate capacity. According to the management, most of the development projects are on well track and domestic gas production is expected to be commenced in H2 FY18. During the quarter, the company has completed the acquisition of an additional 50% interest in the Scarborough gas field. Moreover, it has also completed A$2.5 Bn entitlement offer during the same period which will support to provide equity funding to deliver Scarborough and SNE-Phase 1 and browse to targeted Final Investment Decision. ROE and ROIC stood at 3.4% and 2.4%, respectively in 1HFY18 and the group expects to improve return ratio in the second half based on ongoing developments.

.png)

Quarterly Production Performance (Source: Company Reports)

On the other hand, the Company has recently appointed Meg O’Neill as a new Chief Operations Officer of the Company who has taken his responsibilities with effect from May 2018. In the past one month, the stock price was up by 9.46 per cent and trading at the higher level. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $ 35.470, considering the moderate rise in production for 2HFY18 at the back of aforesaid facts.

.png)

WPL Daily Chart (Source: Thomson Reuters)

Origin Energy Limited

.png)

ORG Details

Decent Outlook: Last month, Origin Energy Limited (ASX: ORG) presented its business prospects at the Macquarie Australia Conference and highlighted about FY18 activity wherein the group has unchanged its full-year 2018 underlying EBITDA guidance for its energy markets business to be in the range of $1.78 Bn to $1.85 Bn, if market conditions and the regulatory environment do not change materially. Moreover, the Origin’s share of APLNG production is expected to be in the range of 245–265 petajoules (PJ) for the full year. Further, the company disclosed its capital expenditure (Capex) and expects in between $360 Mn and $420 Mn for the full year while adjusted Net debt is expected to be below than $7 Bn. On the balance sheet front, the current ratio and quick ratio stood at 1.05x and 1.01x, respectively in 1HFY18 with debt to equity ratio below 1x, representing decent liquidity position of the company.

.png)

Capital Management (Source: Company Reports)

On the other hand, ORG has changed its registered office, principal place of business with immediate effect. Moreover, the group has recently issued new 104,315 Fully Paid Ordinary Shares as the result of the vesting and exercise of Deferred Share Rights issued pursuant to the rules of the Origin Energy Limited Equity Incentive Plan. We expect that the company has decent outlook ahead as the company focuses on strengthening its balance sheet, following disciplined capital management, and reducing organizational complexity and cost. Meanwhile, the share price was up by 12.53 per cent in the past three months (as at July 04, 2018), with gradual rise of 0.101 per cent on July 05, 2018, and the stock currently trades close to its 52-week high levels. Hence, we maintain our “Hold” recommendation at the current market price of $ 9.890.

.png)

ORG Daily Chart (Source: Thomson Reuters)

BHP Billiton Limited

.png)

BHP Details

Strong fundamentals and FY18 Guidance Remains Unchanged: BHP Billiton Limited (ASX: BHP) has provided an operational review for the nine months ended 31 March 2018 wherein the group revealed its full-year production guidance and kept the same unchanged for Petroleum, Metallurgical Coal and Energy Coal. According to the release, the full year petroleum volumes are expected to touch the upper end of the guidance range (i.e., 180-190 MMboe). This will primarily be underpinned by increase in well performance in the Onshore US fields. In addition to this,total Copper production guidance was narrowed to between 1,700 and 1,785 kt while Metallurgical coal and Energy coal guidance was unchanged for the full year and is expected to be in the range of 41-43 MMboe and 29-30 MMboe, respectively. On the financial front, thecompany recorded revenue at $21,779 Mn in 1HFY18 against $18,796 Mn in 1HFY17, marking a growth of 15.9 per cent on a year on year (YoY) basis at the back of product mix growth and pick up in commodity prices. The net margin of the company stood at 20.2% in 1HFY18 which is above the industry median (14.1%). RoE and RoIC substantially increased from 4.7% and 2.7% to 6.7% and 4.5%, respectively in 1HFY18 over the six months period. As a result, the company recorded Current ratio and Quick ratio at 1.75x and 1.40x, respectively in 1HFY18 while debt to equity came down to 0.49x from 0.53x during the same period. Going forward, the company has a bright outlook at the back of several development activities such as Onshore US development activity, Los Colorados Extension project at Escondida and higher utilization rates at Pampa Norte, etc. and oil price scenario.

.png)

Operational Performance and Guidance for FY18 (Source: Company Reports)

On the other hand, the company has recently approved to spend US$ 2.9 Bn on the South Flank Iron Mine Project in the central Pilbara to replace its existing mines rather than adding new supply and increase the quality of its iron ore at a time when the high-grade material is selling at a premium. We expect that this decision will help BHP to compete with its rivals in term of high ore grade as they are in high demand across the market which will support topline growth of the company in future. Meanwhile, the stock price climbed up 15.12 per cent in the past three months as at July 04, 2018 and currently trades near its 52-week high. We maintain our “Hold” recommendation on the stock at the current market price of $ 32.870, given the full-year production guidance along with other on-going developments and commodity prices.

.png)

BHP Daily Chart (Source: Thomson Reuters)

Oil Search Limited

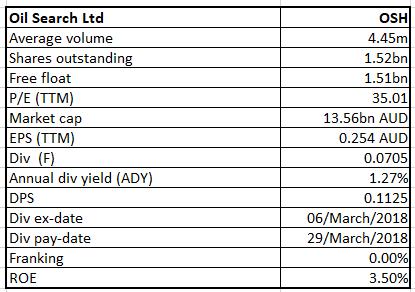

OSH Details

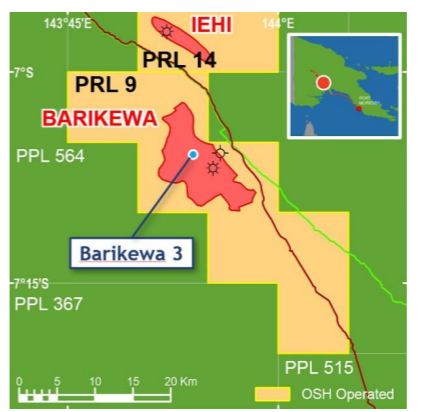

Update on Barikewa 3 Appraisal Drilling Well: Oil Search Limited (ASX: OSH) has recently released an update on Exploration and Appraisal Drilling report for June month. According to the release, the drilling at the Barikewa 3 Appraisal Well in Petroleum Retention License (PRL) 9 in the Western province sits at a total depth of 821 metres as of 25 June 2018. The objective of Barikewa 3was to test the potential resource upside in the field and assist in selecting the optimal commercialization pathway for the resource. The Barikewa 3 appraisal well follows the successful Kimu 2 appraisal well, which reached total depth in late May 2018 and proved up an extension of the Kimu gas reservoir.

Barikewa 3 Appraisal Well Site (Source: Company Reports)

At the end of March 2018, the company held cash of $697.3 Mn with gross debt of 3,625.5 Mn, all of which relates to the PNG LNG facilities. However, the company has downgraded its 2018 production estimate and expects it to be in the range of 23 - 26 million barrel of oil equivalent (MMboe) from the previous guidance of 28.5 – 30.5 MMboe due to the issues erupted owing to natural calamity. We expect that the company has potential to grow further at the back of ongoing developments, resulting into topline growth of the company in years to come. On the other hand, The Capital Group Companies Ltd, a substantial holder of the Group increased their holding from 7.1778 per cent of the voting power to 8.1985 per cent of the voting power. Meanwhile, the share price has risen 23.61 per cent in the last three months as on July 04, 2018 and is trading towards 52 weeks’ high level. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $ 8.910.

.png)

OSH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...