Stocks’ Details

amaysim Australia Limited

Completion of OVO Subscribers Acquisition: amaysim Australia Limited (ASX: AYS) is an asset-light subscription utility provider that delivers clear and transparent mobile and energy plans. As on 5 June 2020, the market capitalization of the company stood at ~$156.41 million. The company has recently announced that it has completed the acquisition of ~77,000 mobile subscribers from My Mobile Data Pty Ltd as OVO Mobile, for a consideration of $15.8 million.

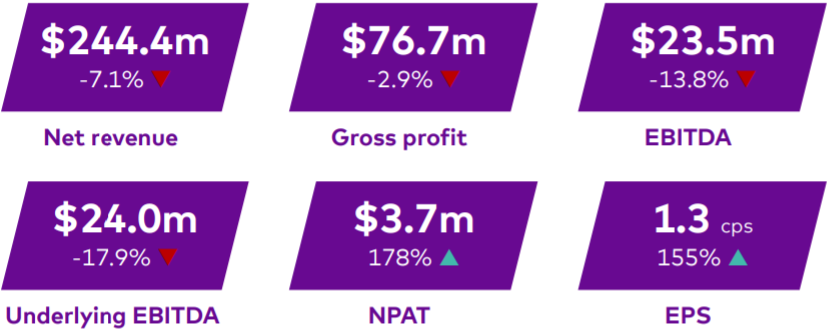

Half-Year Results: During 1H20, recurring mobile subscribers went up by 11.8% to ~706k, and net revenue of the company stood at $244.4 million. In the same time span, gross profit of the company was $76.7 million, and EBITDA of the company stood at $23.5 million. During the half-year, NPAT of the company witnessed a significant increase of 178% to $3.7 million, resulting in a growth of 155% in EPS to 1.3 cps.

1H20 Financial Highlights (Source: Company Reports)

What to Expect: The acquisition of OVO will accelerate the company’s strategic initiatives to grow its recurring subscriber base. The acquisition is expected to be earnings accretive in FY2021, with a higher earnings contribution in FY2022 and beyond. AYS has provided guidance for FY20 and expects EBITDA to be in the range of $33 million – $39 million.

Stock Recommendation: Despite the current challenges in the economy, AYS gave a pleasing performance. As per ASX, the stock of AYS gave a return of 32.5% on the YTD basis and a return of 65.63% in the last one month. The stock is also trading on the average level of its 52-weeks’ band of $0.24 to $0.87. On TTM basis, the stock is trading at an EV/Sales multiple of 0.3x, lower than the industry median (Telecommunications Services) of 2.1x. Considering the attractive returns, current trading levels, decent financial performance, and positive outlook, we recommend a ‘Hold’ rating on the stock at the current market price of $0.525, down by 0.943% on 5 June 2020.

FBR Limited

Hadrian X® Achieves Commercial Lay Speed: FBR Limited (ASX: FBR) is an Australian robotics company, engaged in developing and commercializing digital construction solutions. As on 5 June 2020, the market capitalization of the company stood at ~$111.47 million. The company has recently stated that its flagship technology, the Hadrian X® construction robot, has recorded a new peak laying rate of over 200 blocks per hour. This makes it commercially competitive and compelling when measured against traditional manual bricklaying in most markets around the world.

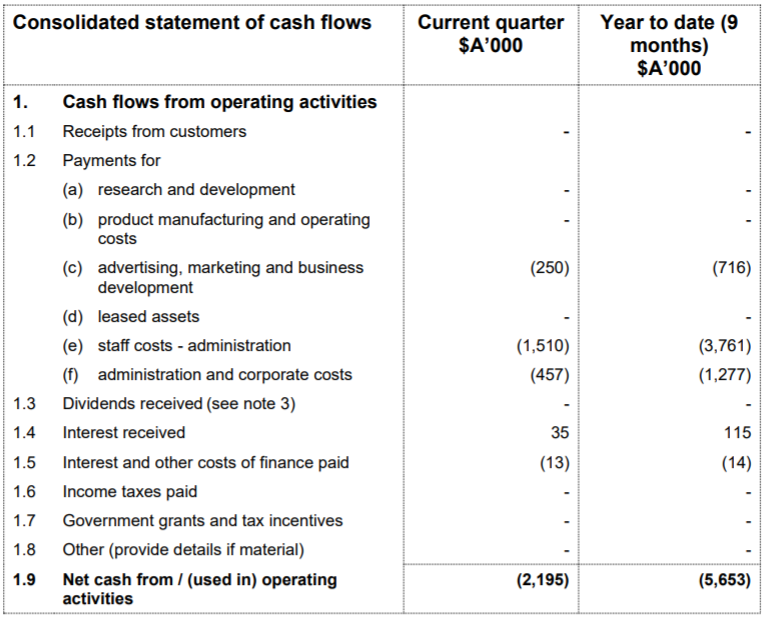

Quarterly Highlights for the Period Ended 31 March 2020: During the three months ended 31 March 2020, FBR took several initiatives to rationalize its costs. The company has decided to postpone the first display home build for the next few months because of the increased focus on the economic, social, and political outcomes of the COVID-19 crisis. During the quarter, the company used total cash of $2.19 million in operating activities.

Quarterly Statement of Cash Flows (Source: Company Reports)

Stock Recommendation:The company remains well-positioned to deploy to a residential site and present its technology to the world. As per ASX, the stock gave a return of 40.91% in the past six months and a return of 72.22% in the last three months. The stock is trading slightly above the average of its 52-week band of $0.010 to $0.105. On TTM basis, the stock is trading at a price to book value multiple of 1.9x, higher than the industry median (Machinery, Tools, Heavy Vehicles, Trains & Ships) of 1.7x and thus seems a little overvalued. Considering the current trading levels, returns in the last six months, softer market conditions due to the outbreak of COVID-19 and higher P/BV multiple as compared to industry, we suggest our investors to wait for the price correction and hence, we have a watch stance on the stock at the current market price of $0.063, up by 1.613% on 5 June 2020.

Integrated Payment Technologies Limited

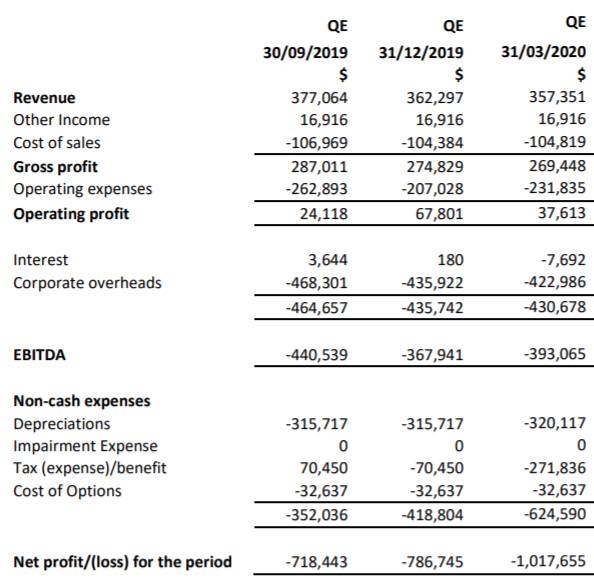

Quarterly Highlights: Integrated Payment Technologies Limited (ASX: IP1) is acting as a clearing house for the payment of superannuation contributions, payroll deductions, salaries and ATO related payments. As on 5 June 2020, the market capitalization of the company stood at ~$7.41 million. During the three months ended 31 March 2020, revenue of the company witnessed a decline from the previous quarter and stood at $357k, and gross profit of the company stood at $269k. In the same time span, net loss of the company increased from $786k to $1.01 million.

Quarterly Financial Highlights (Source: Company Reports)

What to Expect: Given the current uncertainty created by COVID-19 and associated challenges to providing accurate forecasts, the short-term outlook of the company is uncertain. The payment solution of the company, ClickSuper continues to add new payroll providers and is delivering greater value and functionality for its customers.

Stock Recommendation: As per ASX, the stock of IP1 gave a significant return of 118.18% in the past six months and a return of 200% in the last one month. The volatility in the market due to COVID-19 might pose some challenges for the company in the near term. During 1H20, EBITDA margin of the company witnessed a decline over the previous half. In the same time span, current ratio of the company stood at 0.86x, lower than the industry median of 2.56x. Considering the softer market conditions due to the COVID-19 crisis, lower EBITDA margin and decline in results, we suggest our investors to keep an eye on the stock and give a watch stance at the current market price of $0.020, down by 16.667% on 5 June 2020.

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...