St Barbara Limited

St Barbara Provides Update on Joint Venture with Alice Queen: St Barbara Limited (ASX: SBM) is a gold producer and is engaged in mining and the trade of gold, mineral exploration and development. It operates in three countries, with tenements in Western Australia, Papua New Guinea, and Nova Scotia, Canada.

Managerial Changes: On 6th December 2019, the company stated that Craig Jetson will succeed Bob Vassie as the Chief Executive Officer (CEO) and Managing Director of the company in 2020, after the latter retires.

Joint Venture Update: On 28 November 2019, Alice Queen Limited (ASX: AQX) announced favourable results related to the soil and rock chip geochemical sampling program at the Horn Island project under a newly formed joint venture with St Barbara Limited. In addition, it was stated that a Ground Dipole-Dipole Induced Polarisation survey is likely to be finalized by the end of December 2019.

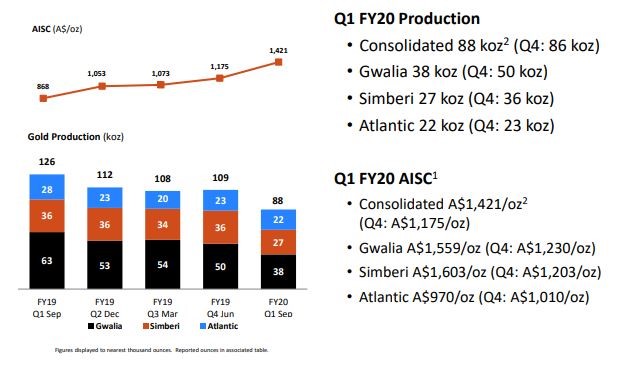

Quarterly Results for the Period Ended 30 September 2019:During the quarter, the company reported total production of 88 koz at an All-in Sustaining cost of $1,421/oz. Operational cash flow for the period stood at $43 million, down from $58 million in the prior quarter. The company had $76 million of cash at bank and A$112 million of debt at the end of the quarter.

Financial Highlights (Source: Company Reports)

Outlook for FY20:Gwalia gold production is now expected to be in the range of 175 to 190 koz. Total production from Simberi operations is expected to be in the range of 110 to 125 koz. Atlantic Goldproduction is expected to be in the range of 95 to 105 koz.AISC for Gwalia operation is anticipated to range between $1,390/oz and $1,450/oz and that for the Simberi operations is predicted to be between $1,285/oz and $1,450/oz. Atlantic operation AISC is expected to be in the range of $900/oz - $955/oz.

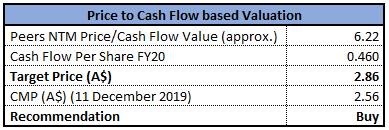

Valuation Methodology: Price/Cash Flow Multiple Approach

Price to Cash Flow Multiple Valuation (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the company’s stock is trading below the average of its 52-week trading range of $2.430 - $5.152. As on 11 December 2019, the company’s market capitalisation stands at ~$1.73 billion. The business has attracted further growth opportunities after the company took major steps to enhance its growth prospects through planned reserve expansion and regional drilling programs. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., price to cash flow multiple based approach and arrived at a target price with lower double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $2.560, up 3.226% as on 11 December 2019.

Saracen Mineral Holdings Limited

Saracen Mineral Acquires 50% Interest in KCGM:Saracen Mineral Holdings Limited (ASX: SAR) is engaged in gold mining, sales and mineral exploration and processing. On 11 December 2019, the company announced the completion of the Retail Entitlement Offer, under which Saracen Mineral hasobtained entitlements applications for around $37.37 million from shareholders of the company. The company has underwritten the shortfall of A$57.34 million, subject to the terms of the Underwriting Agreement. On 29th November 2019, the company stated that it has finalized the purchase of 50% interest in the Kalgoorlie Consolidated Gold Mines (or KCGM) for a consideration of US$750 million.

Entitlement timeline (Source: Company Reports)

Shareholding Update: On 5th December 2019, the company issued an announcement stating that Van Eck Associates Corporation, which is a substantial holder of the company, has reduced its voting power from 15.39% to 12.01%.

Other Recent Updates: On 3rd December 2019, the company announced the appointment of Ben Wessely as the General Manager KCGM, with immediate effect. Additionally, Newmont Goldcorp has predicted CY20 production of Kalgoorlie Super Pit to be 285,000 ounces at an all-in sustaining cost of US$1,035/oz.

Production Details (Source: Company Report)

Quarterly Highlights and FY20 Outlook: During the quarter ended 30 September 2019, the company recorded zero lost time injuries (LTIs) with 0.4 Lost Time Injury Frequency Rate (LTIFR). Gold production for the quarter stood at 96,324 oz at an AISC of $964/oz. Cash and equivalents stood at $196.1 million at the end of the quarter. For FY20, the company expects Gold production to be in the range of 350 – 370 koz at an AISC of $1,025 – 1,075/oz.

Valuation Methodology: PE-Based Multiple Approach

.png)

Price to Earnings Based Multiple Valuation (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the company’s stock is trading below the average of its 52-week trading range of $2.423 - $4.659. As on 11 December 2019, the company’s market capitalisation stands at $3.12 billion.Considering the acquisition of interest Kalgoorlie Gold Mines, financial performance in the September quarter and FY20 guidance, we have valued the stock using one relative valuation method, i.e., price to earnings multiple based approach and arrived at a target price with lower double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $2.930, up 0.687% on 11 December 2019.

Gold Road Resources Limited

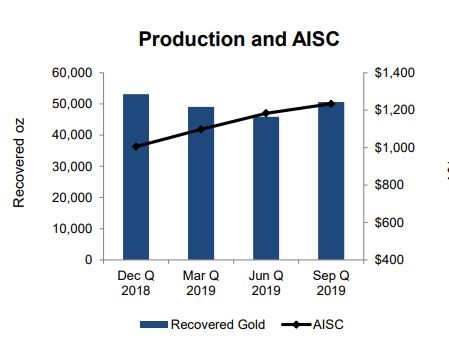

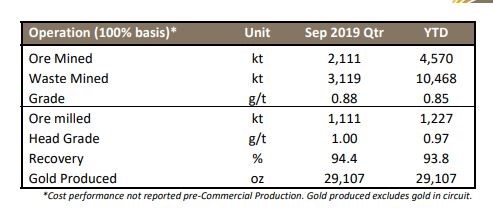

FY19 Production Approaching Upper End of Guidance:Gold Road Resources Limited (ASX: GOR) is involved gold and mineral exploration along with the development of the Gruyere Project in Western Australia (WA). As per a recent update provided by the company on 4th December 2019, the tier-1 gold mine of the company has 12 years of mine life with a production rate of 300 koz of gold per annum at AISC of $1,025/ounce. Ore Reserve at the Gruyere gold mine presently stands at 3.92 million ounces. The mine also possesses 6.61 million ounces of mineral resources.

Quarter Highlights for the Period Ended 30 September 2019: Gruyere generated 29,107 ounces of gold during the quarter. Cash balance at the end of the quarter came in at $65.3 million. The company sold 12,461 ounces of gold at an average price of $2,052/ounce.

Operations Highlights (Source: Company Reports)

Outlook: The company expects FY19 gold production to be in the range of 75,000 to 100,000 ounces for gold production. AISC for the coming quarter is expected to be in the range of $1,050 to $1,150 per ounce.

Valuation Methodology: PE-Based Multiple Approach

.png)

Price to Earnings Based Multiple Valuation (Source: Thomson Reuters)

Stock Recommendation: Over a period of one year, the stock has generated a return of 87.90%. As per ASX, the company’s stock is trading above the average of its 52-week trading range of $0.590 - $1.645. As on 11 December 2019, the company’s market capitalisation stands at $1.02 billion. The development of Gruyere along with enhanced project pipeline, portends good growth opportunities for the business. Gold production for CY19 is expected to be at the upper end of the guidance range. Given the backdrop of the above factors, we have valued the stock using one relative valuation method, i.e., price to earnings multiple based approach and arrived at a target price with lower double-digit upside (in % terms). However, given the decent returns in a period of one year, we have a watch stance on the stock at the current market price of $1.195, up 2.575% on 11 December 2019 and suggest investors to wait for better entry levels.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...