Company Overview: Gage Roads Brewing Co Limited is engaged in brewing, packaging, marketing and selling craft brewed beer, cider and other beverages. The Company operates through two segments: proprietary brand brewing and contract brewing. The Company offers a range of ales and lagers, which are crafted in Western Australia. The Company offers dry-hopped and unfiltered beers. The Company's beers include Little Dove, which is a new world-style pale ale; Sleeping Giant, which is an India pale ale; Single Fin, which is a summer ale; Narrow Neck, which is an American-style pale ale; Break Water, which is an Australian-style pale ale; Atomic, which is an American-style pale ale; Small Batch Lager, which is a European lager, and Premium Mid Pils, which is a Czech Pilsener.

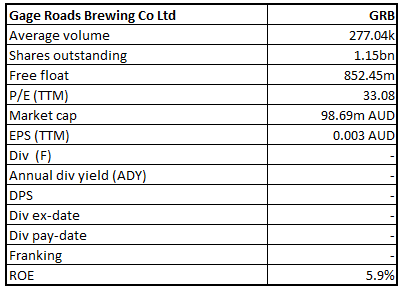

GRB Details

Decent Growth in Topline: Gage Roads Brewing Co Limited (ASX: GRB) is involved in brewing, packaging, marketing and selling of beer, cider and other beverages. The company runs its operations through two segments, i.e., proprietary brand brewing and contract brewing. At the close of 10th January 2020, the market capitalisation of the company stood at ~A$98.69 million. FY19 was another year of strong growth, and there were increased earnings and higher value for its shareholders. During the third year of the 5-Year proprietary brand strategy, the company has continued to deliver on key leading indicators. Between FY15- FY19, the company witnessed CAGR of 12.95% in its revenue with FY15 figure of $24.40 million and FY19 revenue of $39.72 million. This reflects that the company has decent capabilities to generate revenues which could help it in achieving long-term growth. However, the revenues of FY19 experienced a rise of 20% as compared to FY18 due to growth in sales of higher-margin brands. Over the span of four years (i.e. FY15- FY19), the company experienced CAGR of 26.99% in gross profit as FY15 figure was $6.48 million and FY19 gross profit stood at $16.85 million. This reflects that the company is managing its direct costs effectively.

During FY19, total receivables (net) of the company stood at $8.75 million as compared to $4.44 million in FY18. Moreover, it experienced a CAGR of 42.37% in the same metric during the span of FY15-FY19. It can be said that the cash levels of the company might rise in the upcoming periods and it could help the company in experiencing decent levels of growth. Therefore, it might provide the company with the strength to gain strong traction in the industry. The company stated that sales of its “Single Fin Summer Ale” has experienced a rise of 76% in FY19 as compared to the previous year and it has become its highest-selling individual brand. Also, it has proven to be a high performer with the company’s new channels to market. The company also added that the Single Fin continues to be the fastest-growing independent retail brand in the craft market segment.

It was also mentioned that 5-Year proprietary brand strategy is seeking to increase awareness of its proprietary brands as well as to expand those brands into broader national markets, driving incremental sales from the previously up-tapped independent retail and on-premise channels to market. Moreover, greater consumer awareness together with expanded access to the national markets and the new channels(independent retail and on-premise channels) is anticipated to grow annual volumes of the company’s brands, which could help in delivering improvement in margins along with sustained earnings growth through a shift in sales mix to the higher-margin products.

Sales and Earnings of FY19 (Source: Company Reports)

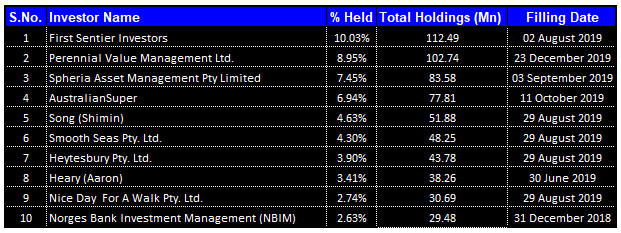

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Gage Roads Brewing Co Limited:

Top 10 Shareholders (Source: Thomson Reuters)

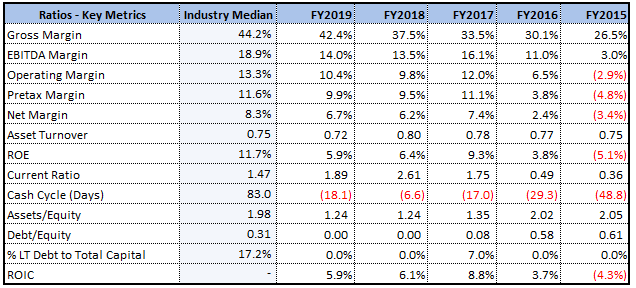

Decent Growth in Key Metrics: Gross margin, EBITDA margin, and operating margin of the company stood at 42.4%, 14.0% and 10.4%, reflecting YoY growth of 4.9%, 0.5% and 0.6%, respectively. Net margin of the company stood at 6.7% in FY19, with YoY growth of 0.5%. This reflects that the company has improved its position to convert its top-line into the bottom-line. Current ratio of the company stood at 1.89x in FY19 in comparison to the industry median of 1.47x. This reflects that the company is in a decent position to address its short-term obligations against the broader industry. The company has no debt, which reflects some sort of stability in the balance sheet. Moreover, a deleveraged balance sheet generally helps the company to focus towards long-term growth objectives.

Key Metrics (Source: Thomson Reuters)

Issue of Shares to Matso’s Broome Brewing Pty Ltd: On 31st October 2019, the company, through a release, announced that it has issued 14,318,615 shares as a performance-based milestone payment with respect to the acquisition of Matso’s Broome Brewing Pty Ltd. Moving to the background, on 20th September 2018, the company has acquired 100% of the shares of Matso’s Broome Brewing Pty Ltd from Peirson-Jones family for the cash consideration of $13.25 million. Since on-boarding the brands, the company also improved the growth in sales rates of Matso’s flagship product such as “Matso’s Ginger Beer” and has reversed the decline of “Matso’s Mango Beer”. The company added that the acquisition of the brands of Matso has provided a step-change for the 5-year proprietary brand strategy and represented a major expansion of its brand portfolio and proved as a catalyst for the re-branding of its sales and marketing team to Good Drinks and the Good Drinks strategy.

A Look at Contract- Brewing Division: During FY19, sales of its contract-brewing division, Australian Quality Beverages (AQB), experienced a fall of 2.5m litres and reached to 5.2m litres as compared to FY18. Out of 2.5m Litres, 1.6m Litres were of Matso’s sales which werepreviously captured under AQB brands are now included as Good Drinks proprietary brands. The company added that AQB volumes are being reduced and are anticipated to reflect around 4 Mn Litres over the upcoming few years.

The combined proprietary sales and AQB volumes have resulted in a total throughput of 13.2m litres and delivered an unaudited EBITDA amounting to $5.5 million for FY19, reflecting a rise of 25% against FY18.

Brands Creation - Support Topline Growth: The company has introduced several new and exciting brands in order to complement its existing brand portfolio. The first product was The Atomic Beer Project and it was stated that it would champion the exploration of hops and reflects an innovation-led portfolio which includes the development of numerous limited releases as well as core products. It was also mentioned that the Gage Roads range has been evolved to take benefit of the growth in craft can format. When it comes to Matso’s range, there has been the addition of Matso’s Hard Lemon to this flamboyant as well as fun flavoured brand family, and there was a continuation to explore the growing consumer trend in order to seek out the brands in new categories.

The company also stated that the first microbrewery and taproom venue in Redfern, which happens to be the home of the Atomic Beer Project, is progressing well. The company is making an investment of around $3 million for the installation of a brewhouse and taproom fit-out of the premises, which would be financed through the current operating cash flows and credit facilities.

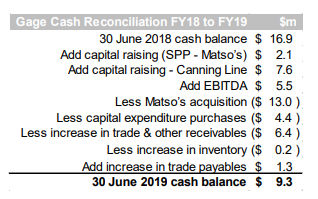

Strong Cash Balance with Zero Debt: Gage Roads Brewing Co Limited witnessed the end of FY19 with a strong cash balance of $9.3 million and in a debt-free position. The business had one-off non-recurring working capital movements resulting from a change of trading terms with Endeavour Drinks and the natural increase of debtors, which was resulted from the onboarding of Matso’s sales and revenues. GRB tackled the working capital movements by utilising the current cash flows and debt facilities. However, these movements were absorbed by year-end, and GRB is implementing a tailored debtor financing facility from the Commonwealth Bank in order to finance any future intra-year movements in working capital for supporting the continued strong growth of its brands.

Cash Balance (Source: Company Reports)

What to Expect: The company added that Good Drinks brands growth and 5-year strategy happens to be on track in order to deliver margin growth along with earnings targets for FY 2020 and beyond. The Redfern venue is anticipated to open in early 2020 and next sites have been identified. The company added that the new can filler, bottle filler and plant improvements provide it with the production efficiencies and reduced waste. GRB is aiming additional earnings in the range of $1.5 million to $2.5 million by FY22 with the help of new machinery.

It added that the program is well underway and is on schedule and on budget. With respect to Good Drinks, the company is planning investment in tier 1 marketing professionals and the outlook also revolves around potential acquisitions.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

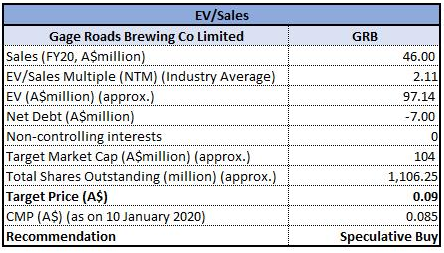

EV/Sales Based Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of GRB has delivered a return of 1.18% in the span of the previous one month. With respect to the Good Drinks strategy, the company is targeting larger east coast markets with expanded Good Drinks capabilities. However, the volume target is 20%-25% per annum growth of its own brands. The company mentioned that Good Drinks team continues to focus on building a capable, empowered as well as nationally represented sales team. For FY 2020, GRB is would continue to explore potential acquisition targets and international opportunities. The company is well-positioned to deliver growth in earnings and sustained value for its shareholders on the back of flexible balance sheet, a management team, which is strongly aligned to shareholders, current revenue streams secured and enhanced ability to drive revenue and margin growth. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., EV/Sales multiple, and arrived at a target price of lower double-digit growth (in percentage terms). Hence, we give a “Buy” rating on the stock at the current market price of A$0.085 per share (down 1.163% on 10 January 2020).

.png)

GRB Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...