Softness in First Half Result: Santos Ltd (ASX: STO) recently announced a 2016 first half net loss of US$1,104 million, impacted by the previously announced impairment charge for GLNG of US$1,050 million after tax and lower oil prices. The underlying net loss was of the order of US$5 million after tax (excluding impairments and other one-off items). However, STO at the same time reported for a record production (up 10% over 1H15) and significant cost reductions achieved in the first half with unit upstream production costs slipping by 15% to US$8.80/boe and capital expenditure down by 58% to US$283 million. The stock fell about 6.8% on August 22, 2016 while the company decided for no interim dividend payment.

1H FY2016 Performance (Source: Company Reports)

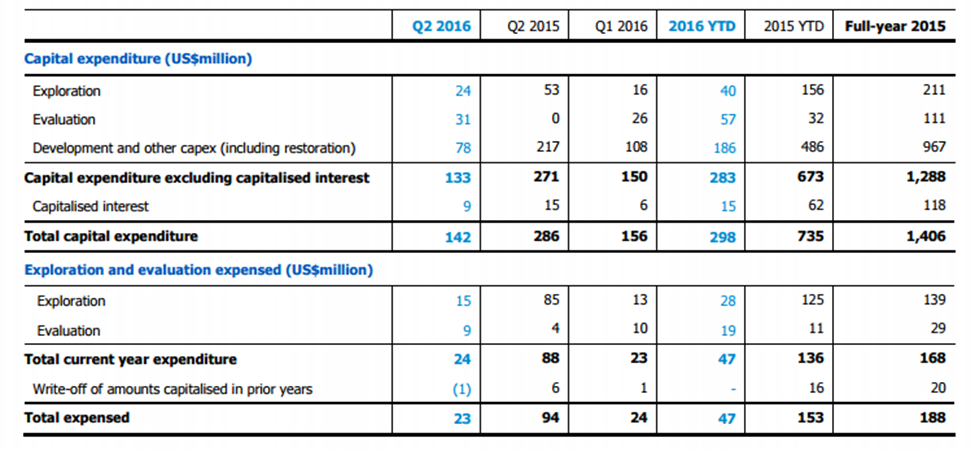

Heavy impairment costs against GLNG: STO had already reported that they would incur a heavy impairment charge from the carrying value for GLNG of over US$1,050 million after tax (about US$1,500 million before tax) for its 2016 half-year performance. But the group reported that this would be a non-cash charge and would not impact their debt facilities. On the other hand, the group is controlling its capital expenditure wherein its first half capital expenditure reached US$283 million, which is 58% less as compared to the same period of last year.

Santos control in its capital expenditure (Source: Company Reports)

Cash flow scenario: One of the key factors that investors needed to note was whether the group would be able to meet its cash flow estimates despite facing impairment charge for GLNG coupled with ongoing tough market conditions they are facing given the volatile oil price environment. The group targeted for a positive cash flow for this year in November 2015. On the other hand, the oil prices have fallen a bit since last year while US dollar strengthened further against Australian dollar. Given these conditions, the group’s target of positive cash flow this year was seen to be challenging. However, the company said that it has made a good progress in the first half and is forecasting a free cash flow breakeven oil price of US$43.50 per barrel for 2016, down from US$47 per barrel. The new operating model is said to lift productivity and drive long-term value for shareholders in a low oil price environment.

Update on ramp up in production of GLNG: Management had reported that they would continue to face pressure given the ongoing tough market conditions in LNG market. The group is increasing its production of GLNG equity gas cautiously while the third party gas price has increased. Accordingly, Santos is adjusting their assumptions regarding upstream gas supply and third party gas pricing. But the group assured that this would not impact their GLNG’s ability to meet its LNG off-take commitments. Santos is constantly striving to cut costs while pursuing opportunities to optimize their asset portfolio. Moreover, the group is focusing on a long term basis for its GLNG project and we believe that the group is well positioned to face these hurdles. Management is forecasting a better LNG market in the long term, and accordingly, Santos is positioning to be a key supplier of LNG and targeting growing demand from the Asian market.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...